Is Growth the Only Choice Before Retirement?

There are multiple advisors and investment firms that are willing to help you transition from receiving income from working to using your investments to generate income to cover living expenses. That reality exposes a hard truth that many financial advisors are focused on growth without meaningful income.

The theory is that you have to sacrifice income to achieve meaningful growth. Then, you need someone to help you move from the growth model to the income model. There may be something wrong with this approach. This approach means you are unwilling to believe that a bird in the hand is worth two in the bush. Stock prices can go up, but they also go down. Dividends are cash that you can now deploy as you see fit.

One way to see that cash does have value is by the default approach of “Target Date” retirement funds or Fidelity’s “Freedom Funds.” There are two reasons many might like these funds. One of the reasons these funds exist is to get you to think you are gradually getting a total portfolio that is less risky because of the increasing allocation to bonds. What are bonds good at? They are good at providing income. However, that income comes at a huge cost: price appreciation or growth.

If you tell an investor who is 65 years old that they have less risk and more income, you will get their attention. I’ve already written many times about the increased risk of bonds and the absolutely poor long-term returns of that type of investment. That topic doesn’t warrant more time in this post. Rather, it would be wise to think about the benefits of having an investment portfolio that offers both income and growth regardless of your age or retirement status. That likely means bonds and target date funds are not the best way to get growth or growth in income.

Number Six: Income Plus Growth

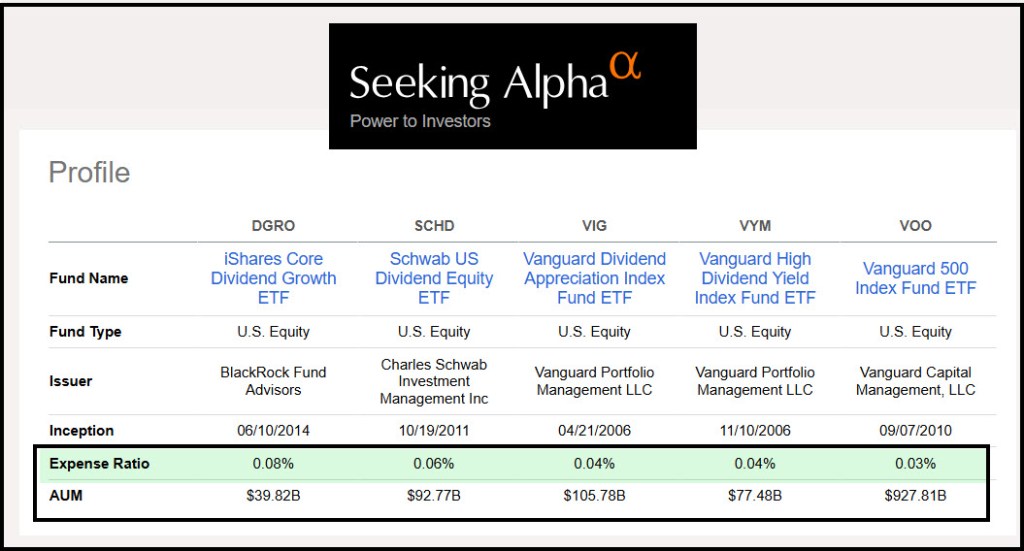

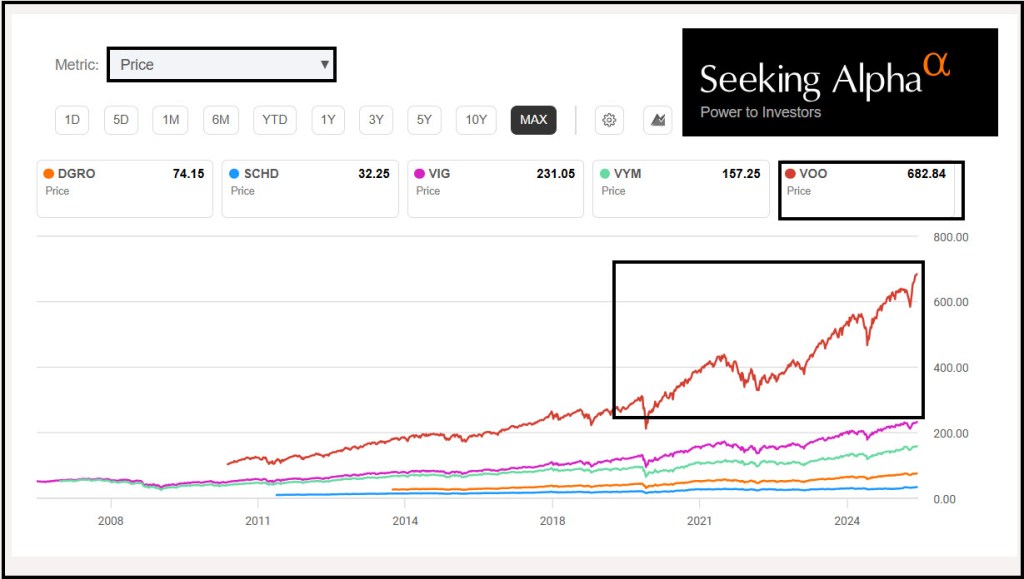

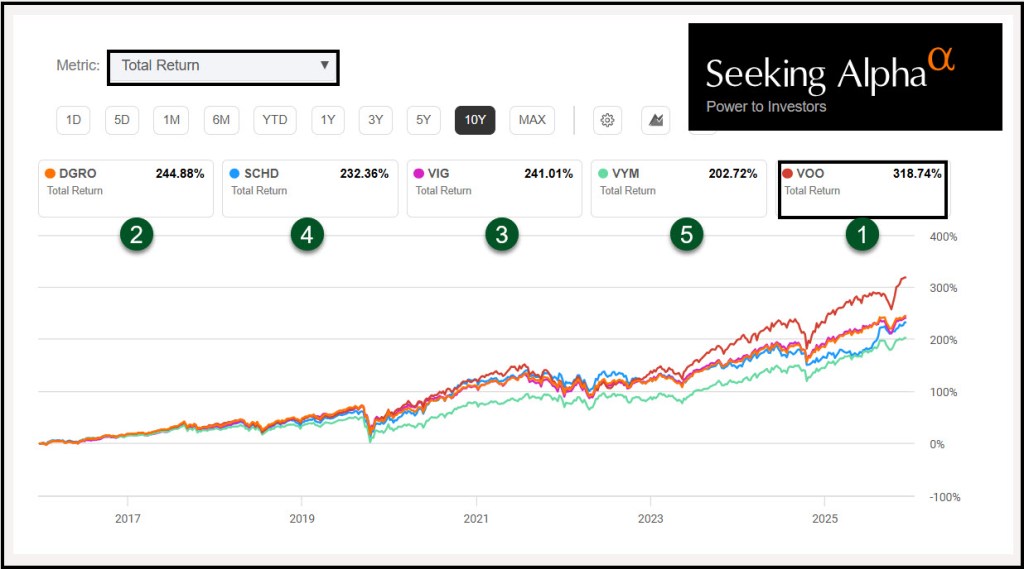

For the investor who doesn’t want to own individual equities, there are some good ETFs that offer the income plus growth model. For the sake of illustration, I will compare five ETFs: DGRO, SCHD, VIG, VYM and VOO. These ETFs are managed by iShares, Schwab, and Vanguard. Each of them provides dividend income and capital appreciation.

DGRO iShares Core Dividend Growth ETF

SCHD Schwab US Dividend Equity ETF

VIG Vanguard Dividend Appreciation Index Fund ETF

VYM Vanguard High Dividend Yield Index Fund ETF

VOO Vanguard 500 Index Fund ETF

When I look at the performance of our investments I am interested in three elements: 1) The overall growth (capital appreciation) of each account and of the total of our eight accounts. 2) The income that is defined by both dividend yield of our total portfolio and the dollars that can be reasonably expected to arrive every month. 3) Income that is growing to counter the impact of inflation. This model means that no changes are needed to fuel income before or after retirement.

A Key Benefit of This Model

One of the downsides of the “growth” at the expense of income model is that your financial advisor is likely selling investments and buying other investments to “rebalance” your holdings. That is an expensive way to invest. While it isn’t a bad idea to trim your holdings of the winners and to look for other investments, there is a different path worthy of consideration.

If you have dividends that are flowing into your accounts pre-retirement, you have a great opportunity to either automatically reinvest those dividends or to expand your portfolio into new ETFs or equities. If most of your investments are not paying a dividend or pay a meager dividend because they are so focused on “growth” you have fewer opportunities to add to your flocks and herds. Yes, you can sell an investment to raise capital, but that would be just another task that may not be in your best interest. It certainly doesn’t set you up for retirement income. One of the great fears of retirees is that the market will drop significantly after they retire.

In fact, the reality is that many investors panic in a down market. They sell at the bottom of the cycle out of sheer panic and then they buy when things turn the corner, but usually too late. As a result, their investment portfolio suffers irretrievable and often permanent harm.

Why do they have this fear? It is because they look at their account balance as their future income instead of looking at the income the investments are producing, even when the market is in a correction or bear territory. I think it is better to remember the income component regardless of the market’s current behaviors.

What is Possible?

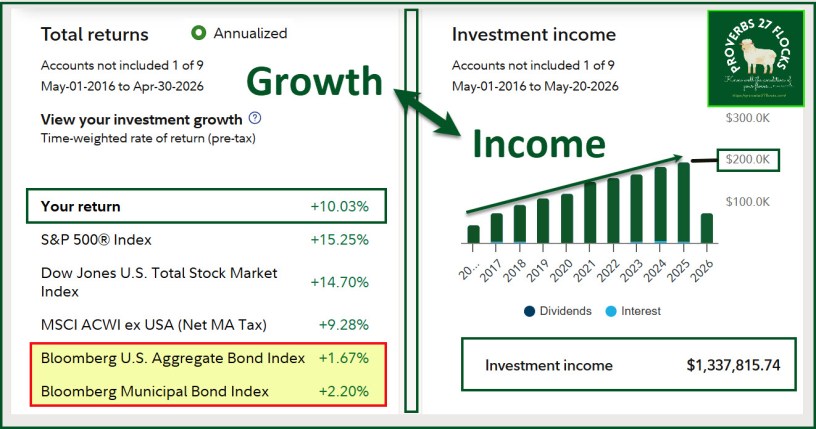

The current value of my traditional IRA and my ROTH IRA is just over three million dollars. The total estimated annual income (EAI) from the investments in those two accounts is at least $181,000. That means my current yield is six percent. This does not include the interest or dividends I receive from cash or money market accounts, nor does it include options income.

If all I was seeing was the income portion, I would neglect considering the growth component. For our investment mix, over the last ten years, the goal has been average annual growth of 9-10%. That is easy to achieve.

Using the Rule of 72, that means my IRA accounts could double to $6M by 2034, or eight years from today. That, by the way, is accomplished while at the same time receiving income each year well over $200K for all of our accounts. Growth plus income is a good model.

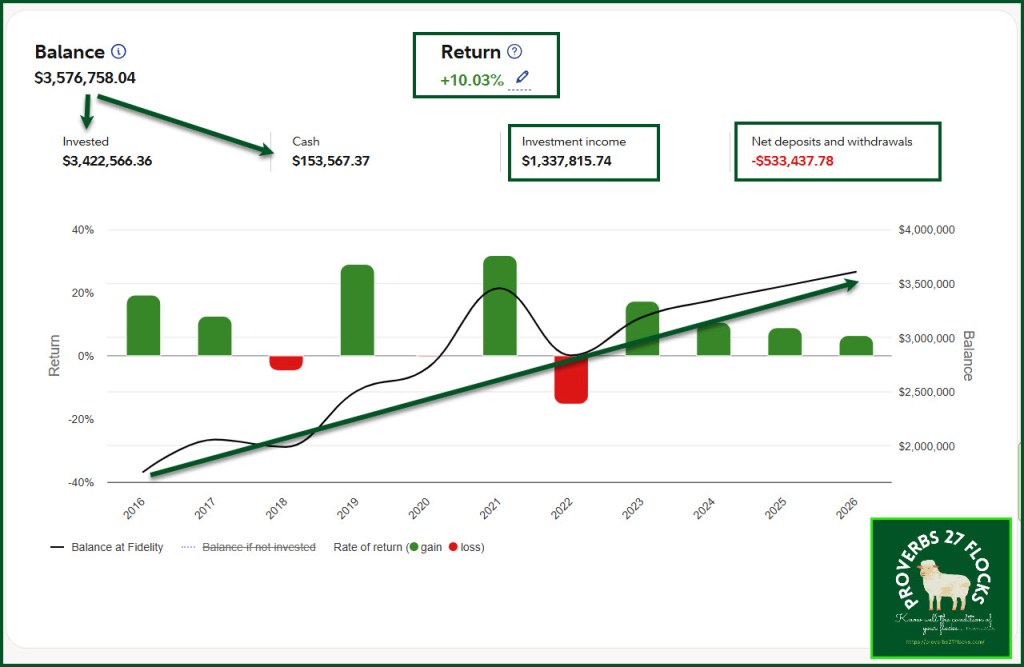

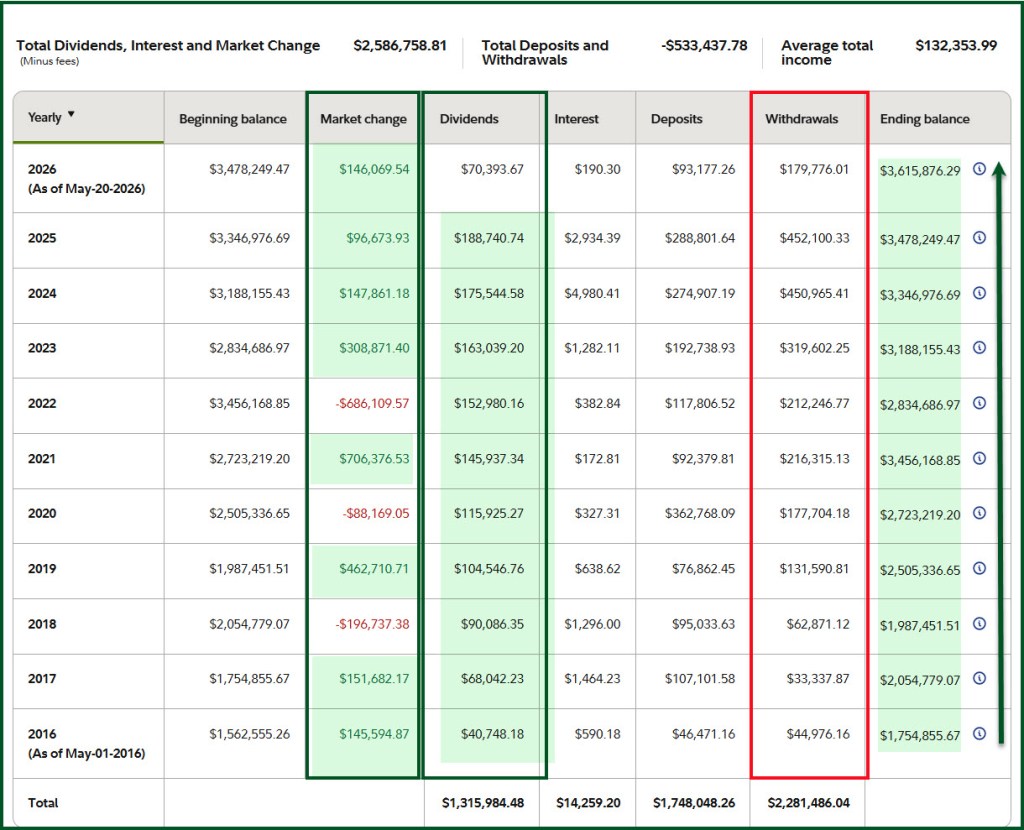

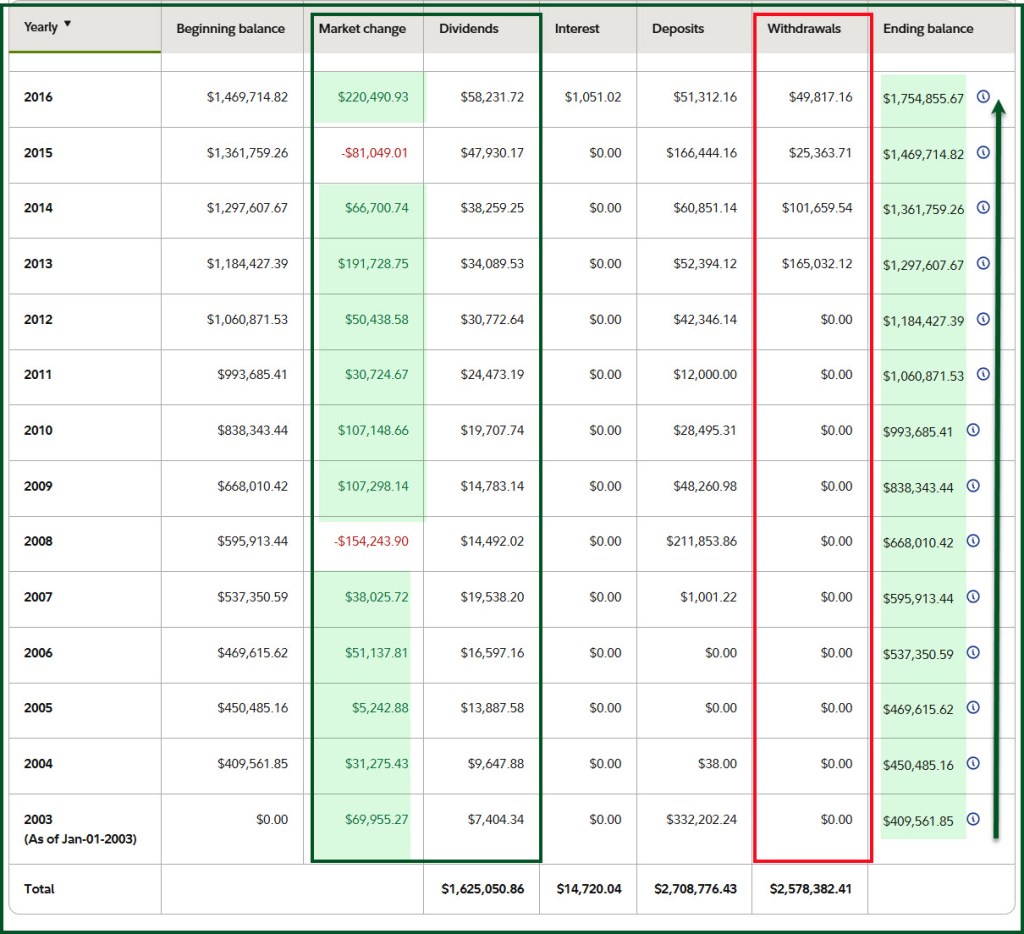

When you look at our results from 2016-2026 YTD, you should notice some trends. First of all, notice the ending balance. You should see growth. That is the result of “Market Change” or the ups and downs of the value of the investment portfolio in the “market’s” view. That can go up and it can go down. Then look at the dividend column. That is going up, regardless of the market’s temper tantrums.

The same observations can be made for 2003-2016. We started with $332K. During the time period 2003-2026 we have received $1.6M in dividends. Those are birds in the hand. They are not in the bush and cannot fly away.

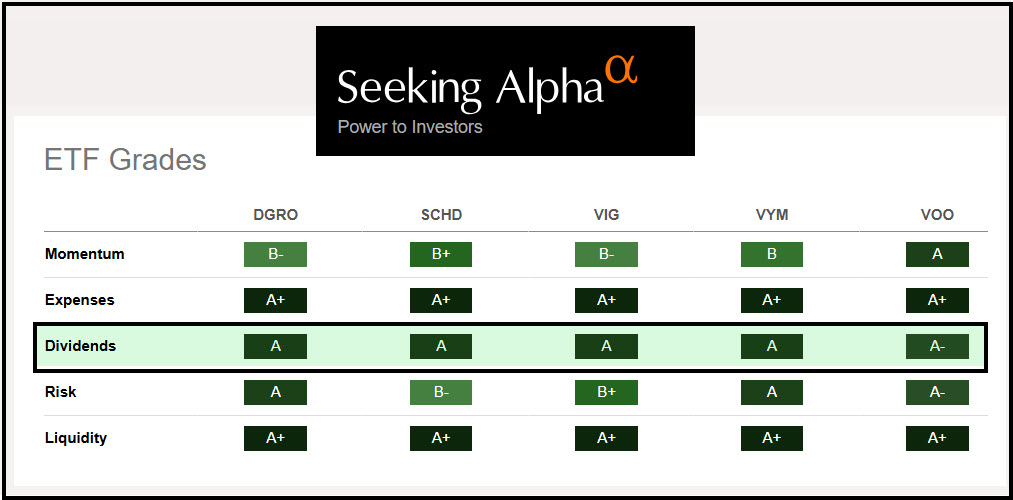

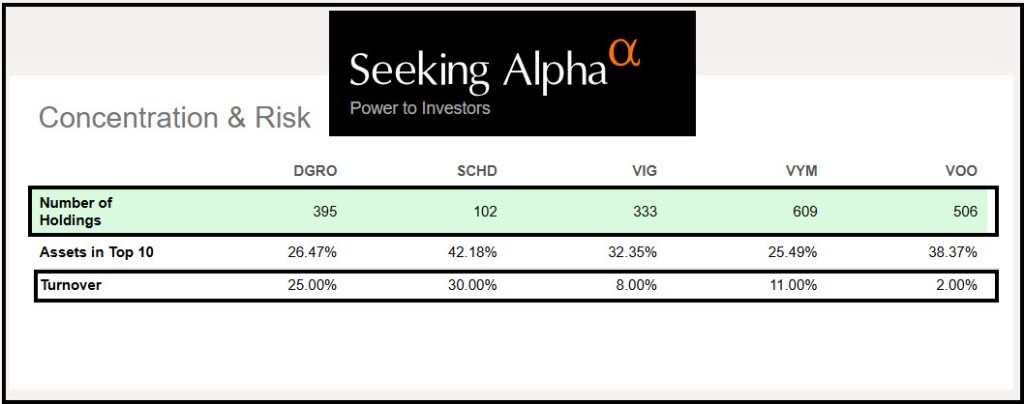

Comparing DGRO, SCHD, VIG, VYM and VOO

It is prudent to compare investments before buying one or two for your investment portfolio. To that end, here are some key images from Seeking Alpha for the five ETFs worthy of consideration. They display expenses, total returns, price returns, ETF Seeking Alpha grades, dividend characteristics, price performance, and concentration (is it diversified or not?)

Summary

Don’t believe, at least don’t believe without some thought, that growth investments must sacrifice on the altar of no or little real income. If nothing else, income might cause you to press the pause button before selling your investments in a market downturn. Don’t kill the cow that is producing milk or the chicken that is laying eggs. The cow or the chicken might be worth less at various points due to market conditions, but the milk and eggs are still food for the present.

Proverbs 27:23-24 “Know well the condition of your flocks, and give attention to your herds, for riches do not last forever…”

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com

All scripture passages are from the English Standard Version except as otherwise noted.