Do You Think and Shop Wisely?

There are multiple ways to look at the costs of investing. Many just ignore costs because they may be inevitable in one way or another. However, the cost of each investment should be a consideration when buying any investment and when choosing the account to hold the investment. Costs can include the drain on a portfolio at the account level (advisory and management fees), the costs of individual investments (mutual funds and ETFs), and the costs associated with trading. There are also “hidden” costs like the ultimate taxation of the investment. Two costs that are sometimes overlooked or misunderstood are: 1) Foreign income tax on some international investments and 2) The income tax to be paid for REIT ownership in a taxable account.

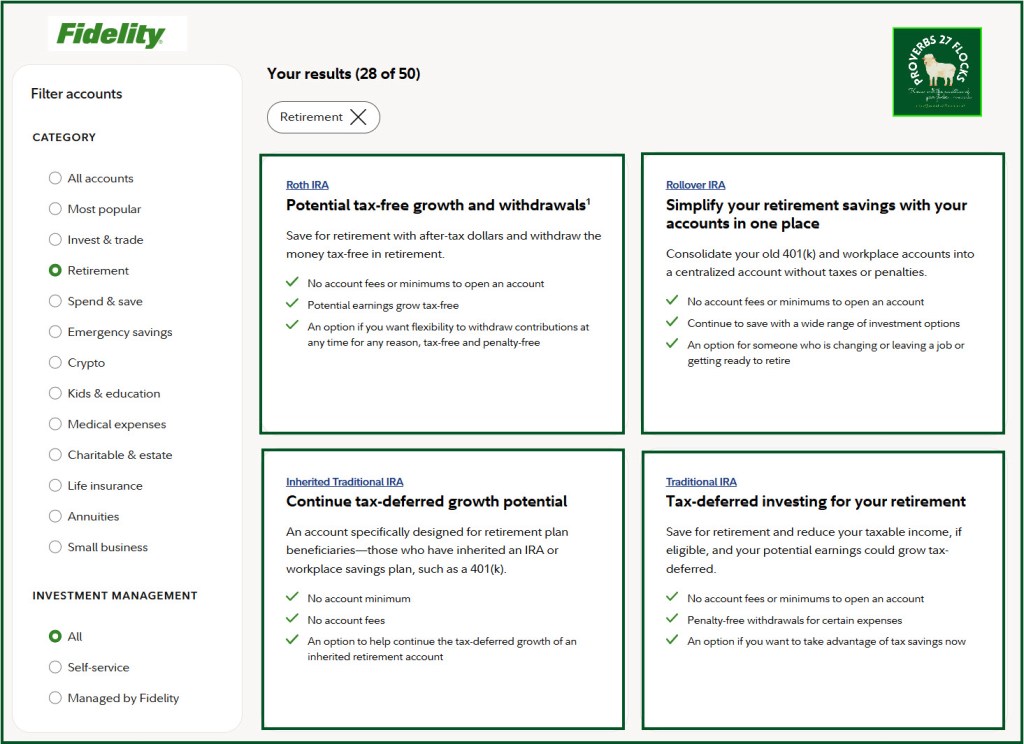

Don’t neglect counting the cost of the type of account you use for investing for retirement.

The True Cost of the Traditional IRA

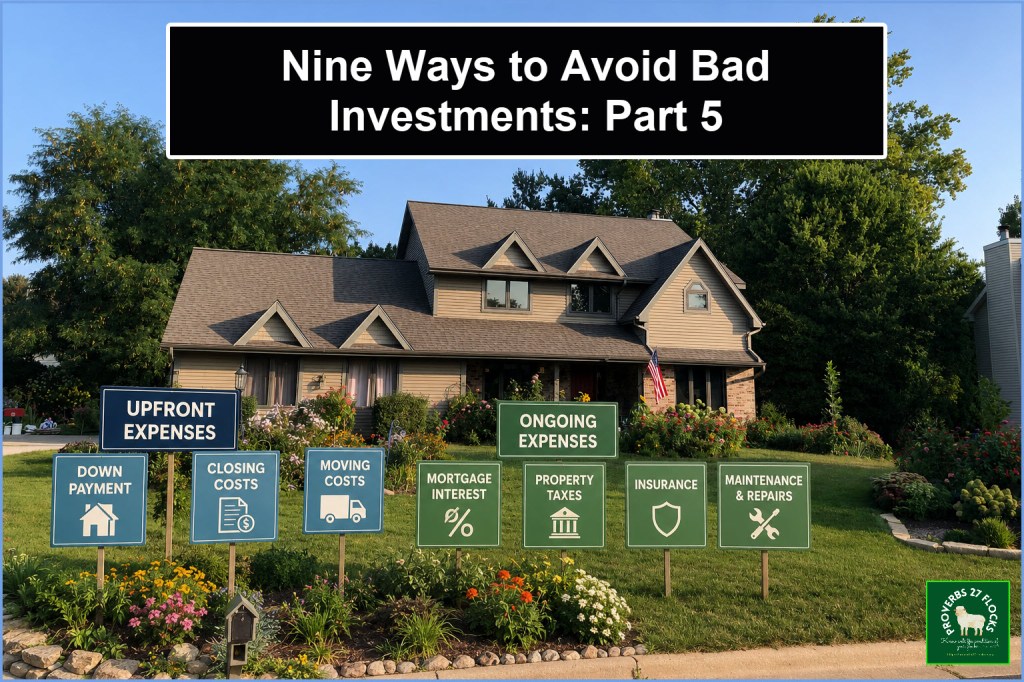

Let’s start with an example that is often misunderstood: the “profit” from the sale of your primary residence. Many people think their primary residence is an investment. It certainly can be an asset, but for most people it is not a very good investment (if you are looking for a good ROI.) The costs of real estate includes upfront expenses like the down payment, closing costs, and moving costs, as well as ongoing expenses such as mortgage interest, property taxes, insurance, and maintenance. It’s important to consider all these factors to understand the total cost of buying and owning a home.

You might buy the home for $250K and you might be able to sell it for $500K. Therefore, you may be tempted to think you made a “profit” of $250K. Perhaps, but probably and realistically not. This might only work if you paid cash up-front and sold the house one year after you bought it without paying for any of the costs associated with home ownership. If you owned the home for 20 years, consider the buying power of your $250K “profit.” You have less buying power. Of course, that is true of every dollar, but it is easy to think about the buying power in today’s dollars, not the buying power 20 years from now.

When you buy the investments in your IRA, and they appreciate, you won’t really get to spend every dollar of the increased value of your assets. Most investors don’t pay attention to the day of reckoning. You must start taking required minimum distributions (RMDs) from your retirement accounts once you reach age 73. Your first RMD is due by April 1 of the year following the year you turn 73, with subsequent RMDs required by December 31 each year. The traditional IRA was a good resource for building a retirement nest egg, but it is a costly investment vehicle. It is full of hidden costs, not the least of which are the income taxes on the withdrawals. Required Minimum Distributions (RMDs) are generally taxed as ordinary income in the year they are taken.

Number Five: Count the Costs and Seek to Avoid Them

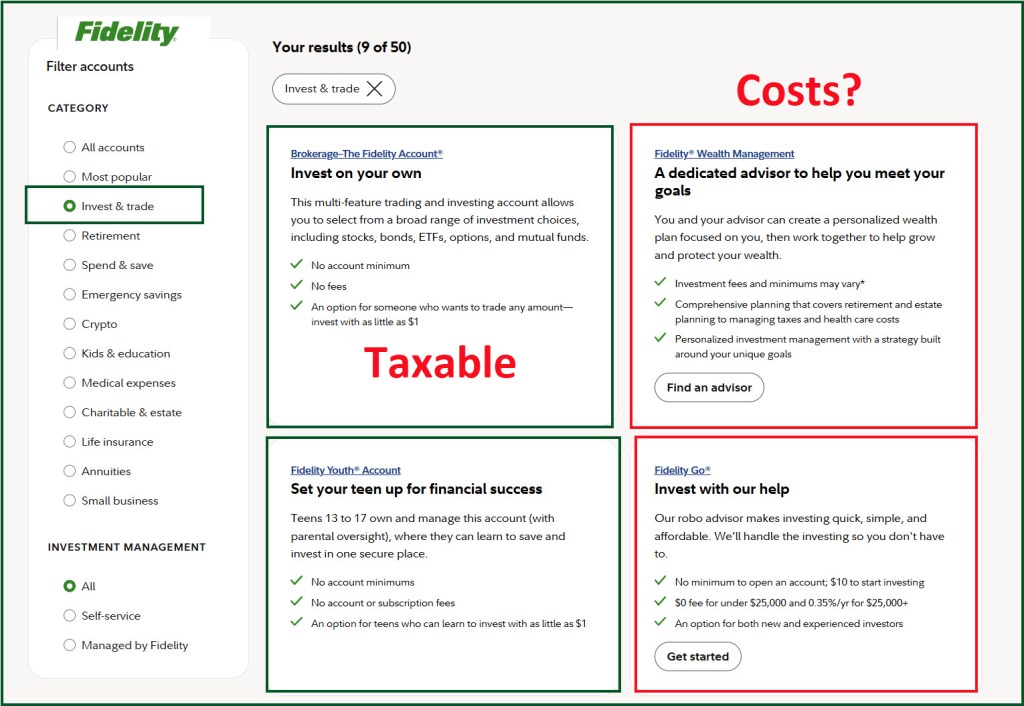

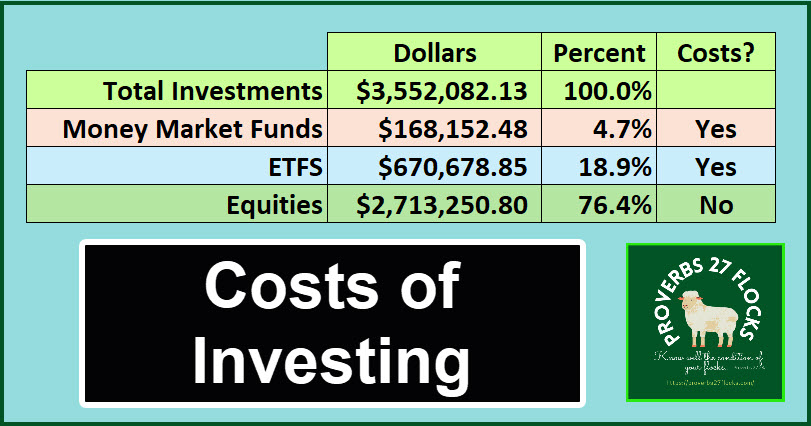

If you were to examine our investment assets you would find that I don’t buy mutual funds other than money market funds like SPAXX, FZDXX and FDRXX. I do own ETFs, and there are costs associated with owning all of those funds. But a large portion of our investments are individual equities like ABBV, MSFT, AVGO, BMY, CRDO, MAIN, CSWC, NNN, and NVDA. There is zero cost of ownership when you buy individual stocks. Yes, it takes more work than buying some mutual funds or ETFs, but when your portfolio is $250K or more it pays to consider individual equities. Bear in mind that some funds are heavily skewed by their top ten investments anyway, so some investors might do better by buying shares of the top ten investments in the S&P 500 index.

Foreign Taxes are a Cost

Some countries have some really nasty taxes that get applied to the company’s dividends. I’ve learned to be skeptical of those investments. Some examples include SNY (Sanofi is based in France), ASX (ASE Technology Holding Co in Taiwan), and ZIM (ZIM Integrated Shipping Services in Israel.) I’ve seen at least $2,486 disappear from my income due to foreign taxes.

For ZIM I tried to get a waiver, but it failed – so I sold my shares. The standard Israeli withholding tax rate for dividends is 30%, but certain shareholders may qualify for a reduced rate under specific conditions. Having dividends taxed at 30% makes ZIM an unsatisfactory investment unless you are willing to accept the reduction in the true income and yield.

REITs generally fall into three categories: equity REITs, mortgage REITs, and hybrid REITs. REITs usually don’t pay corporate income taxes. The government rarely gives you something for “free.” The dividend payments you receive from your REIT investments can constitute ordinary income, capital gains, or a return on capital. This means you probably will pay for this benefit in higher taxes unless you hold the REIT investments in a non-taxed account like a traditional IRA or ROTH.

“Tax efficiency is a cornerstone to any well-balanced portfolio. To ensure you don’t pay more taxes than you have to, it’s important to consider moving some of your investments out of taxable accounts. This is especially true for real estate investment trusts (REITs).” – www.dividend.com

“One of the core principles of income investing is minimizing taxes. For this reason, allocating high-dividend REITs to tax-advantaged accounts is a prudent step in ensuring you don’t pay more than you have to.” – www.dividend.com

The Contents of Our Portfolio

ETFs are a significant portion of our total investment portfolio. Almost 19% of the total is in ETFs. Individual equity investments, however, make up a much larger total and are 76.4% of our total dollars invested. There is no ongoing cost for these investments. Furthermore, they tend to offer more opportunities for options trading.

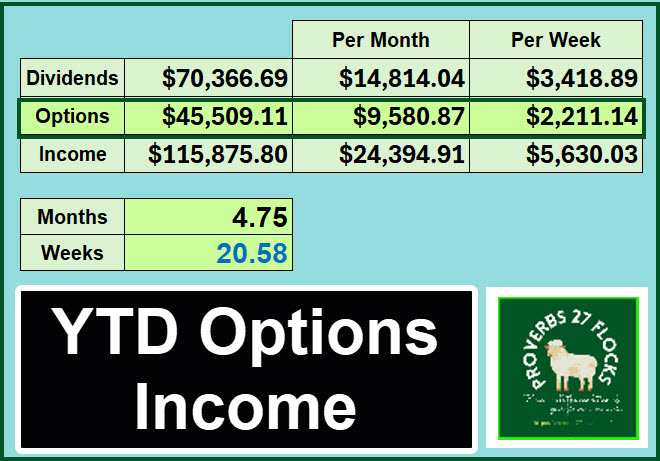

Options income can be meaningful low-cost income. 2026’s YTD options income is now $45.5K, or an average of $2,200 per week. However, some of this income is in traditional IRA accounts, so it will be taxed as ordinary income. The options income in the ROTH IRA’s, however, will not be taxed, so there is zero cost assigned to that income.

Summary

Just as home ownership has some sneaky long-term costs that erode the value of the home as an investment, there are many ways your investments and account types can become quite costly. Don’t ignore the costs. Fidelity provides a good summary of “Six Habits of Successful Investors.” Numbers five and six are worth noting: 5. Consider low-fee investment products that offer good value – Savvy investors know they can’t control the market, but they can control costs. Also 6. Don’t forget about taxes – Another habit that may help investors succeed is keeping an eye on taxes and account types.

Proverbs 27:23-24 “Know well the condition of your flocks, and give attention to your herds, for riches do not last forever…”

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com

All scripture passages are from the English Standard Version except as otherwise noted.