What is Easy Income?

We need to define “easy.” When I say easy, I don’t mean there is no work involved. Rather, the term is meant to convey simplified, unhurried, user-friendly, and uncomplicated. Therefore, it isn’t about trying to sell something, and it certainly isn’t about trading options. It also isn’t about trying to time the market with a buy low and sell high strategy. It is about a process that results in income, and the primary goal is to minimize the time spent while maximizing income that grows over time.

Easy Money is Easy

Easy money is money you can easily acquire. It is income obtained with a minimum of effort. It sounds too good to be true. In fact, most of the time when someone pitches something that is too good to be true, it isn’t true. I think there are some exceptions.

A New Series

The best way to help you see how easy money works is by example. Therefore, this is the first in a series of blog posts to discuss the easy money investments we own. This will include CDs, stocks, and ETF investments. In each post I will talk about the nature of the investment, the reason it may qualify as easy money, the quality of the investment using outside resources to help gauge quality, and the factors that determine if and when I buy shares of the investment.

Does Easy Money Work?

Well, if it doesn’t work then there is nothing easy about it. An annuity might be easy to buy, but it doesn’t work for me. Social Security is easy, but the best it can do is adjust for inflation, and it doesn’t do that very well.

To help illustrate the power of the dividend growth model, consider the following four images from Fidelity Investments. The first one shows the last 20 years of dividend income on a monthly basis. $4,336 is the average monthly income during the last 20 years. That would work out to about $52,000 per year.

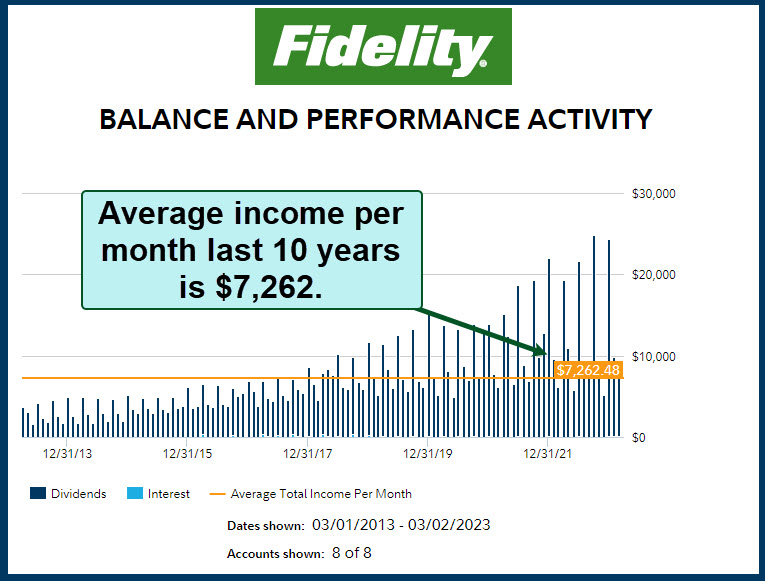

Last Ten Years

The dividend growth model was not something I understood or used twenty years ago. However, I did understand the model ten years ago, so if we look at the ten-year average income it grows to $7,262 per month. That is about $87,000 per year on average. When we add our Social Security to that amount, we hit six figures in real income. There is no time clock or commitment to be in an office or a need to flip burgers at McDonald’s.

Last Five Years

The last five years have been anything but rosy. Covid, wars, rumors of wars, and inflation have all thrashed our economy and the world economies. However, if we look at our five-year average income it grows to $10,199 per month. That is about $122,000 per year on average. So perhaps this easy money engine is still working. Of course, what happens if we look at the last three years?

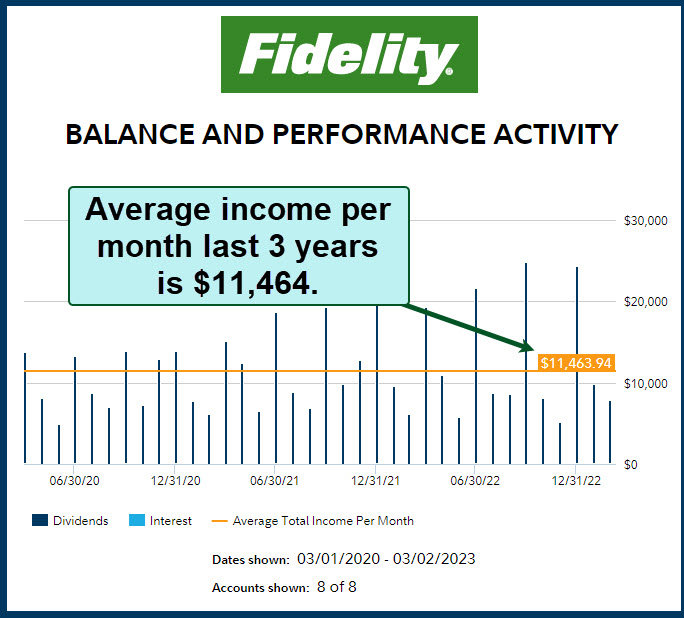

Last Three Years

The last three years have been awful for most investors. The three-year average income grew in spite of the market’s temper tantrums. In the last three years our average monthly income was $11,464. That is about $137,000 per year on average. Last year, total dividend income exceeded $150,000.

Conclusion

When inflation is nipping at your heels, think about how you must manage your investments. Don’t take the hard path. Consider reading the rest of the posts in this series and then set a strategy for easy money. Of course, if you have a better solution, use your solution instead.