Let the Insurance Company Pay You

Think about insurance. Insurance, by its very nature, is related to bad news. The car is totaled, you have someone slip on your icy driveway, hail damages your roof or a tornado blows your entire house down. You also go to the hospital and the news isn’t good and it is expensive news. We buy insurance for bad news. To make matters worse, most of the time the cost of insurance increases over time. That is why I like buying shares of an insurance company that sends some of the increase our way.

This is the third in the series. My goal is to present arguments in favor of a simplified and uncomplicated way to have income before and in retirement that grows even if we do nothing.

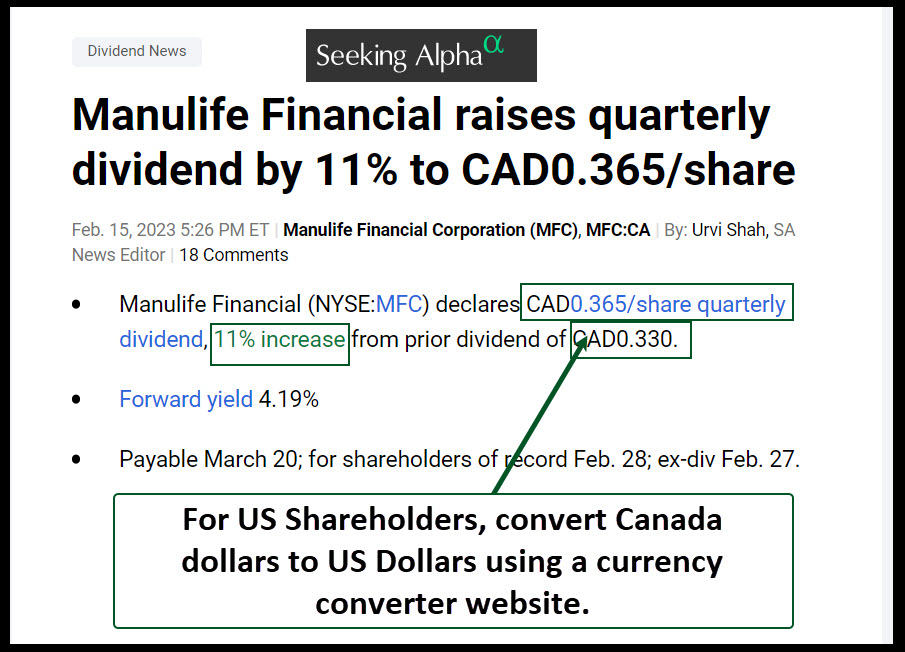

The best way to help you see how easy money works is by example. Today’s example will focus on an insurance company in Canada. Manulife Financial Corporation is one of our financial investments.

In each of these educational posts I discuss: 1) The nature of the investment, 2) The reason it may qualify as easy money, 3) The quality of the investment using outside resources to help gauge quality, and the 4) Factors that determine if and when I buy shares of the investment. In each case I will be talking about an investment that we own.

The Nature of MFC

Cindie and I have homeowner’s insurance, auto insurance, and an umbrella policy. We also have Medicare supplemental coverage. We don’t buy annuities and we don’t need life insurance. However, we do like it when an insurance company pays us. MFC pays us even though we don’t have any insurance with them.

Manulife Financial Corporation, together with its subsidiaries, provides financial products and services in Asia, Canada, the United States, and internationally. The company operates through Wealth and Asset Management Businesses; Insurance and Annuity Products; and Corporate and Other segments. The Wealth and Asset Management Businesses segment offers investment advice and solutions to retirement, retail, and institutional clients through multiple distribution channels, including agents and brokers affiliated with the company, independent securities brokerage firms and financial advisors pension plan consultants, and banks. The Insurance and Annuity Products segment provides deposit and credit products; and individual life insurance, individual and group long-term care insurance, and guaranteed and partially guaranteed annuity products through multiple distribution channels, including insurance agents, brokers, banks, financial planners, and direct marketing. The Corporate and Other segment is involved in property and casualty reinsurance businesses; and run-off reinsurance operations, including variable annuities, and accident and health. The company also manages timberland and agricultural portfolios; and engages in insurance agency, investment counseling and dealer, portfolio and mutual fund management, property and casualty insurance, and mutual fund dealer businesses. Manulife Financial Corporation was incorporated in 1887 and is headquartered in Toronto, Canada. www.manulife.com

Why I Think MFC Qualifies using EIS*

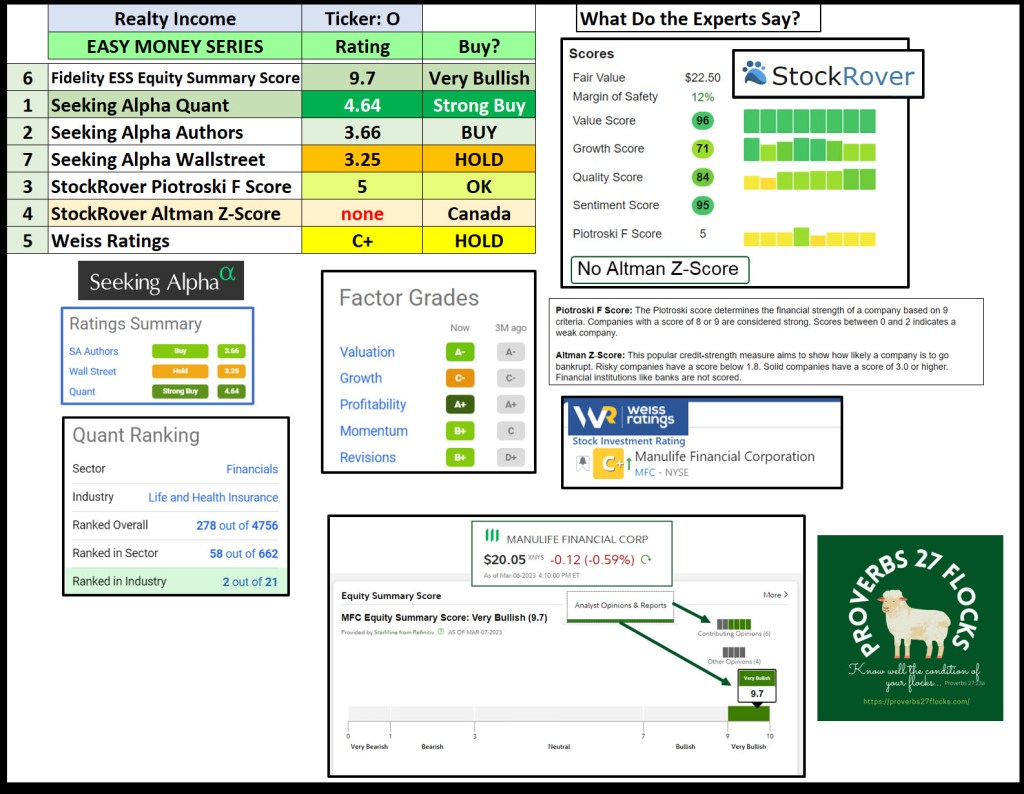

When I look at an investment, it is now like any other task that I have done a hundred times. I don’t even have to remind myself to consider the attributes I need to see before I invest. The following image summarizes most of the things I want to see in an investment. MFC (Manulife Financial Corporation) meets my criteria. However, bear in mind that MFC is not a growth investment. It is just a way to have growing dividends.

The Quality of the Investment

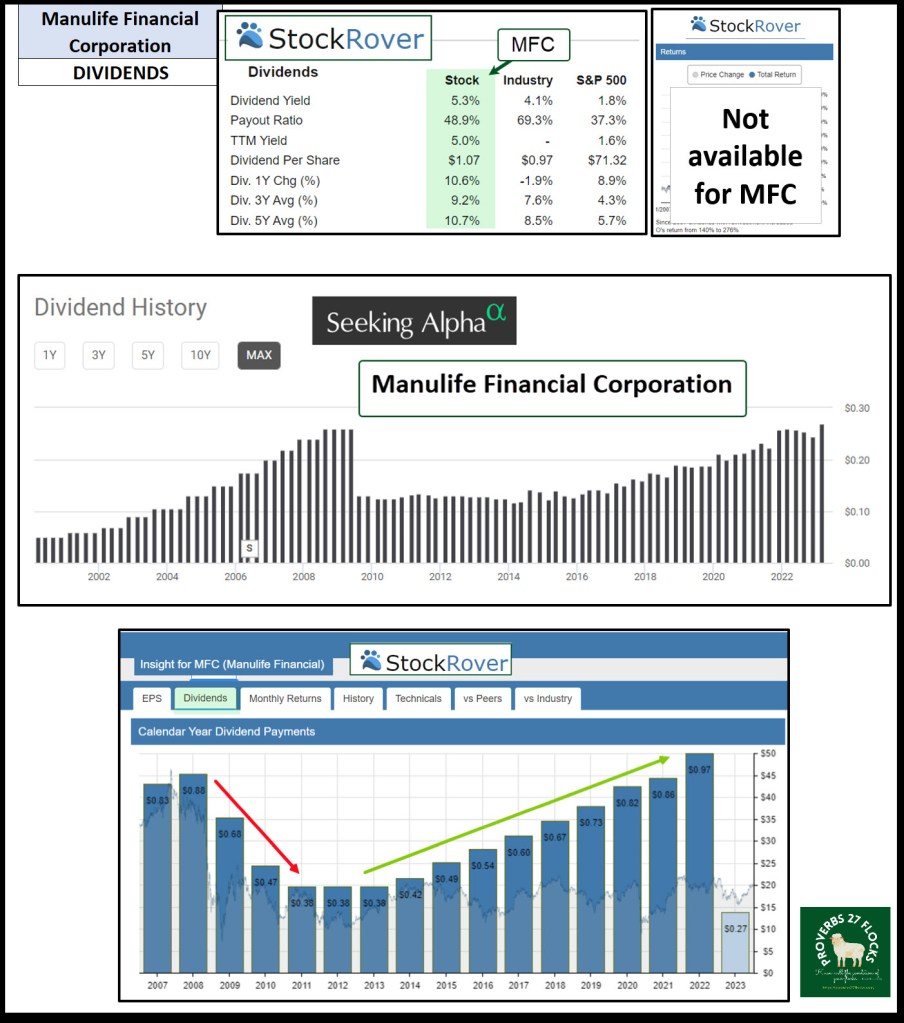

Just like my previous post, where I talked about REIT “Realty Income”, I look at the same resources. This includes the ESS at Fidelity, the QUANT rankings from Seeking Alpha, some scores and information from StockRover, and the Weiss Rating. Read my previous post to see how I view each of these ratings.

One of the reasons we don’t own more of MFC than we do, is that it is a slower growth investment. However, the yield is worth having this as a piece of our total diversification and it adds some international North America to the mix.

Factors I Consider Before Buying

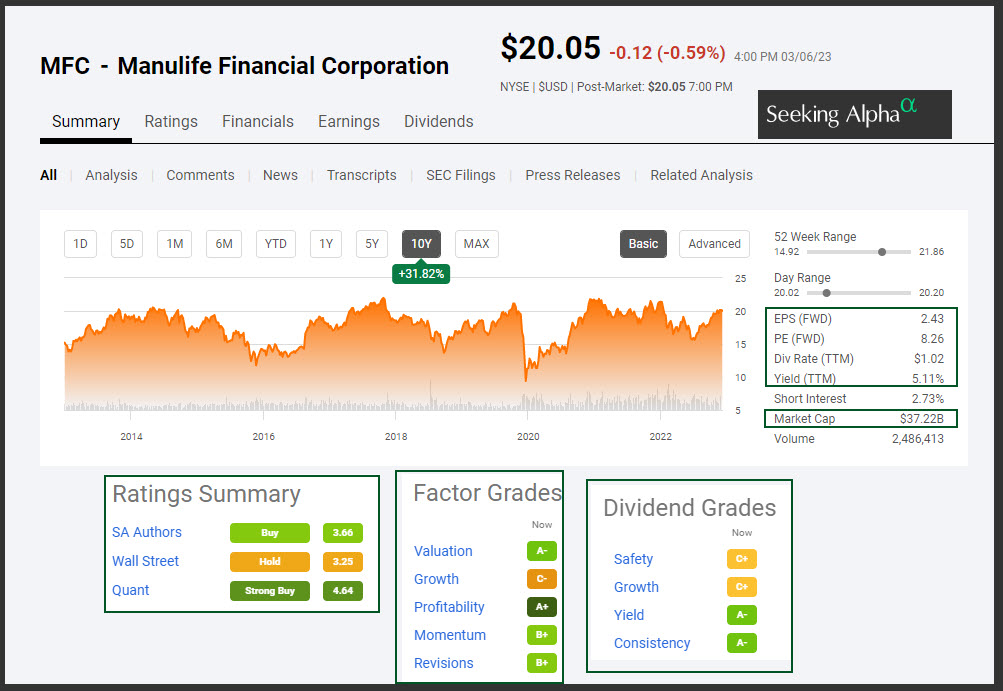

There are three factors that are preeminent or prominent in my mind. The first is that the business must not only be sustainable, but it must also have growing revenue and earnings. Growth is a sign of a business with wise leadership and future opportunity. The second is that the board of directors sees value in sharing a good portion of the profits with the shareholders. This portion should grow over time. This means the dividend payout ratio is not less than 20% for most of our EIS investments. The third is the ranking of the investment using Seeking Alpha’s QUANT score.

In the case of Manulife, the insurance company compares favorably in the sector. It is currently two out of 21 in the life and health insurance industry. In other words, it is in the top 10% of all other similar investments. It is also number 58 out of 662 in the sector called “Financials.” This puts MFC in the top 10% of all of the choices in the SECTOR. The only stock above MFC is CNO (CNO Financial Group, Inc.) We do not own shares in any other insurance company, but we have had some investments in other companies in the past.

Reminder: What is EIS?

EIS is my abbreviation for “Easy Income Strategy.” Each value needs to be at least a “3” or I will pause and not rush to buy. If most of the values are “4” or “5”, I will either buy, or continue to hold or add more shares. Therefore, “5” is a strong reason to buy, “4” is a good reason to buy, and anything lower than a “3” is a cause for potential concern.

Conclusion

It pays to have insurance. It is good protection, but it can also be a source of income in retirement.

Full Disclosure

Cindie and I own a combined total of 1,500 shares of MFC. Those shares are worth approximately $30,000. Therefore, MFC is NOT one of our top ten investments. Always bear in mind that our ownership is not a recommendation to buy the investment. Always align your investment purchases with your written investment goal, strategy, and rules for each investment you make. Suffice it to say, if we invest in something, it is certainly the result of focusing on our goal and strategy.

The Easy Income Strategy – What is Easy Income?

We need to define “easy.” When I say easy, I don’t mean there is no work involved. Rather, the term is meant to convey simplified, unhurried, user-friendly, and uncomplicated. Therefore, it isn’t about trying to sell something, and it certainly isn’t about trading options. It also isn’t about trying to time the market with a buy low and sell high strategy. It is about a process that results in income, and the primary goal is to minimize the time spent while maximizing income that grows over time.

Easy Money is Easy

Easy money is money you can easily acquire. It is income obtained with a minimum of effort. It sounds too good to be true. In fact, most of the time when someone pitches something that is too good to be true, it isn’t true. I think there are some exceptions.