What is Asset Class?

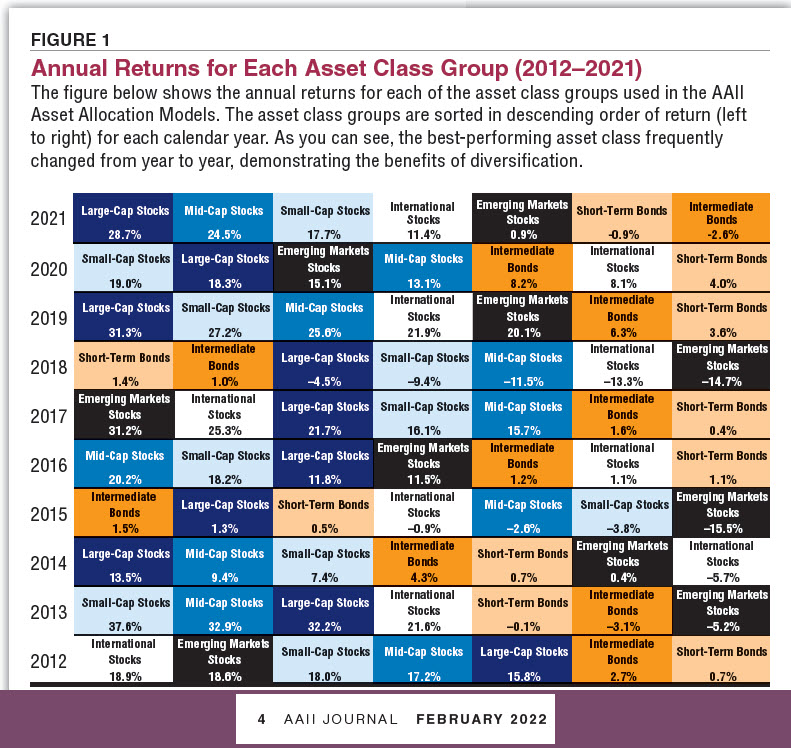

As I was reviewing my February 2022 AAII Journal, I was curious about one figure on page 4 of the issue. The table’s heading was “Annual Returns for Each Asset Class Group (2012-2021). The figure shows seven asset groups for the ten years considered. I believe the contents of the table are instructive. I’d like to take a break from my annuity series to talk about what I think we can learn from the table.

What are the Asset Classes?

The seven are Large-Cap Stocks, Mid-Cap Stocks, Small-Cap Stocks, International Stocks, Emerging Markets Stocks, Short-Term Bonds, and Intermediate Bonds. For the sake of simplicity, I prefer to break the classes into Large, Medium, Small, International, and Bonds. International includes “international” and “emerging markets.” Bonds includes short and intermediate term bonds.

Large Cap Stock Returns

Although large cap stocks (the really big companies in the S&P 500 index) aren’t always in first place for the ten years being considered, there are three things that pop out for me. First, there is only one year (2018) where large caps had a negative return of -4.5%. Secondly, this class is consistently on the left side of the table. For half of the years, large cap stocks hit the top two positions in five years. Finally, Large-Caps were the champs three of the ten years. If you want consistent growth, think large cap as a large portion of your total retirement plan.

Mid-Cap Stock Returns

Mid-cap stocks had a bit more uncertainty in the ten-year history. Only once did they hit the number one position. Having said that, Mid-Caps never dropped to the sixth or seventh place. I like selecting mid-cap stocks, rather than buying a mid-cap ETF or mutual fund. Of course, that means I need to spend more time picking stocks. Another approach is to buy a dividend growth ETF like VYM. VYM and DGRO “invest in growth and value stocks of companies across diversified market capitalization.” Stocks in the mid-cap region include FNF, HPQ, LYB, and MPW. These four are dividend-paying positions in the financials, information technology, materials, and health care real estate. Don’t forget that dividends are a helpful way to get more cash to buy more investments.

Small-Cap Stock Returns

I have a much larger allocation to small caps than most investors should consider. For example, 27% of our total investment capital is in small cap. For most investors, 5-15% is probably a less risky approach. In the table we can see that Small-Cap stocks appear four times in the top two positions, and twice in the top position. In fact, Small-Cap is the only other asset class that achieved that position more than one time. Again, ETFs like VYM, DGRO, and similar dividend growth ETFs will give you exposure to small cap companies. Many of my small-cap investments are REITs or BDCs. For example, the big ones for me are NEWT, MAIN, FLGT, ABR, and CSWC. Most of these are value stocks (except FLGT), not growth investments. In other words, I am looking for healthy dividends I can use to buy more of other investments.

International and Emerging Markets

Most advisors and brokers will encourage an investor to have international exposure. I have a hard time recommending any mutual funds or ETFs for this class of investment. Nevertheless, there is one year when both took a turn in the top seven. However, if you look at the far right, you will see that this category managed eight entries out of twenty boxes. If you want international investments, let me encourage you to consider stocks in specific companies in Canada or the United Kingdom. Canada’s banks (CM and TD) are a good starting point as is Seagate in Ireland (STX). For mining companies, RIO is a good pick. RIO (Rio Tinto Group) engages in exploring, mining, and processing mineral resources worldwide and is headquartered in London UK.

Bonds of All Flavors

Do you want to play it safe and not expose yourself to stock market risk? Be my guest, but I cannot recommend that strategy. Inflation will kill your real returns. Please notice that in one year the Short-Term bonds won first place, the real return was 1.4%. Intermediate bonds grabbed a first place slot with a 1.5% return. My suggestion: keep a light allocation of bonds for a steady flow of income. Pay attention to the returns of bonds in the two right-most columns. Bonds are a good way to lose buying power over the years. Ninety-five percent of our assets are in stocks and only 2% in bonds.

Time to Ask, “What Should I Do?”

For the average hands-off investor, especially if you are 65 years old or younger, let me encourage you to avoid bonds. Focus most of your investing dollars in large cap value and growth stocks. Then, to gain exposure to the small-cap and mid-cap stocks, buy a good dividend growth ETF like DGRO, SCHD, or VYM. Finally, consider a REIT and a BDC for some of your investment dollars. Two of the key pillars in this area are the ones with “O” and “MAIN” for the ticker symbols. O is a REIT and MAIN is a BDC. Both pay a monthly dividend.

Full Disclosure

Cindie and I large positions in VYM, MAIN, O, SCHD, RIO, CM, TD, FNF, HPQ, LYB, MPW, NEWT, MAIN, FLGT, ABR, and CSWC.

Hi Wayne

Just read this article and again as always I am blown away with your knowledge and expertise in investing. Such great information for us lay folks and for free. Wish i had found you long ago. But better late than never.

LikeLiked by 1 person