A Balanced View Requires Asking Good Questions

This is the third in a four-part series. In the first installment I explained that an annuity is a life insurance product that can pay you while you are living and even provide an inheritance for your heirs. In the second I gave the advantages some might see in buying an annuity contract. In this edition, I believe you need to know there are disadvantages. Most retirees who have planned for retirement should avoid buying an annuity unless there are good reasons to do so.

Who Wants You to Buy the Annuity?

It would not be unusual for your bank, your stockbroker, or your financial advisor, whether fiduciary or not, to suggest that you move money from your savings account, from your bond funds, or even to sell an investment to raise cash to buy an annuity. I saw one investor say that their Fidelity representative suggested they buy either CD’s paying about 1% for twelve months, or even a fixed annuity for three years. The fixed annuity was paying 2.4%. If you are earning 0.10% on your cash, receiving 2.4% might be a compelling offer. But is it really in your best interest?

While it is true that bonds will likely decline in value as interest rates rise, you need to understand that the one selling you the annuity is not going to tell you why 2.4% is not in your best interest. Be aware that you can buy three-year US Treasury bonds on Fidelity’s web site that are currently paying 2.57%. Furthermore, you could choose a two-year treasury bond and receive 2.42%. You don’t pay a commission and won’t pay a 12% surrender fee on a treasury bond.

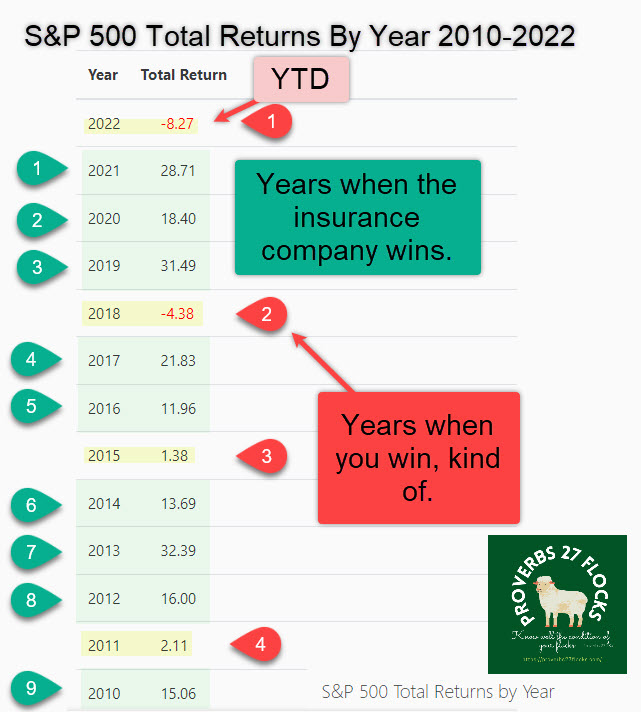

Annuity as Insurance

When you give money to a car dealer for an extended warranty, or buy term life insurance, or pay for renter’s or homeowner’s insurance, the insurance company doesn’t set the money aside to pay you if you have a claim. They put the money to work. They invest the money.

The same is true with the dollars you give when you buy an annuity contract. Rest assured, if the insurance company is offering you a 2.4% return, they are reasonably certain they can earn at least ten percent on your dollars. If you give them $100,000, they might give you $2,400 per year. They also plan to make far more than that on your $100,000. Of course, if the investments they buy are a bust, they won’t make money. But the general trend of the stock market is usually on their side. They have done the math.

Some Disadvantages to Remember when Asking Questions

Sometimes when we talk about disadvantages, the goal isn’t to completely discourage an idea. Rather, the goal is to know what questions to ask and how to interpret the responses. Knowing the disadvantages makes you a better buyer so that you can select the best product for your needs.

For example, many think that the best vehicle to purchase in 2022 is one powered by electricity. It might be a good solution for some, but there are disadvantages with this type of transportation. For example, do you have the charging station you will need at your apartment, your home, or your place of work? How much will it cost to install the charging station? What happens when the batteries need to be replaced? What is the driving range of a single charge on the car you are considering? Is the mining of lithium good for the environment? Will supply and demand cause the costs of batteries to skyrocket? Thoughtful questions can help you know if the disadvantages outweigh the advantages.

The Potential Disadvantages of Annuities

Life is full of situations where you might have advantages and disadvantages associated with a choice you need to make. When we flew to Hawaii with our granddaughter, we rented cars on all three islands. We declined the rental car company insurance coverage. That lowered our costs, but there were potential additional costs if there was an accident that might not be covered entirely by our own auto insurance policy.

Knowing that there are risks and choices, what questions would I encourage you to ask? Here are some of the most important potential disadvantages of annuity contracts:

The costs are bigger than you think or can imagine. Be careful about the fees. Annuities can have many different layers of fees. Ask for an itemized list of the fees and look at the total. If your annuity earns 7-9% and you pay 3-4% in fees, you may be better off with a different product. In a recent discussion, while helping a friend, I asked her advisor what the fees were for this work on her behalf. He started by talking about one fee that was 0.45%, and then another that was 0.35%, and then yet another that was 1.50% on the first $250,000. In other words, the fees for his services and associated broker and management fees were 2.3%. If we put that in dollars per year, she was paying at least $5,700 per year for about five hours of work. This work did not include her annuity.

The Exit Costs (Surrender Penalty) are Daunting. It is not uncommon for an annuity to have a surrender period. The longer you hold the annuity, the lower the costs are. However, do not be surprised if the first several years of surrender charges on a ten-year annuity are 12-14%. If you change your mind about the $100,000 annuity in the second or third year, expect to pay the insurance company $12,000 or more to get out of the contract if you want the cash for other purposes. You might also have costs for specific annuity riders.

There may be tax-related penalties for early withdrawals. Some investors might be subject to a tax penalty of 10% if you withdraw money before the age of 59.5. Sadly, far too many people buy annuities when they are in their 30’s, 40’s, and 50’s. There are many reasons to delay entering an annuity contract until you retire.

You need to think about income taxes. You will pay taxes as ordinary income when you receive payments. While the interest you earn on an annuity before you receive payments will grow in a tax-deferred status, then, when you withdraw these funds, the earnings and your past contributions get will be taxed as ordinary income. This is similar to a distribution from a non-Roth 401(k) or IRA. In other words, you might receive $2,000 in income, but depending on your income taxes, you might not be able to spend the entire $2,000. Furthermore, your $2,000 is going to be worth less due to inflation. Always be thinking “income taxes” and “inflation” when thinking about income.

Commission rates are high for annuities. If your broker sells you an annuity, they are likely receiving a large commission on the sale that you generate. Once again, ask how your advisor is being paid for the work they are doing to sell you the annuity. If they aren’t transparent about this, or suggest that they gain nothing, it is time to be a bit skeptical. Agents sell insurance products to earn a commission. I read one article that said a typical annuity commission is around 6%. That means a $100,000 annuity earns the salesperson up to $6,000. It is little wonder then, that the surrender charge can be $12,000.

Annuity growth will often be much less than stock market growth. What is your participation rate? The stock market typically makes a gain during the year. A good year might see results of 10-20% or more. That means more money for your investments, but it isn’t a guarantee that the value of your annuity will grow. For example, Indexed products in this category will often cap the gains through the participation rate. If your annuity has a 75% participation rate, then you’ll receive that percentage of the amount that the index fund grows.

Annuities are generally inflexible. Annuities are not as adaptable as other investments. Once you buy an annuity contract, your money is committed. If you buy stocks, ETFs, mutual funds, or bonds, you can usually sell most of them at a significant profit. You also participate in the dividends, dividend growth, low costs, and the power of dividend reinvestment. If you trade covered call options, you can add even more income. Bear in mind that annuities are long-term contracts. As such, you need to compare your long-term returns with the long-term returns of something like large-cap dividend-paying ETFs.

Without additional costs, annuities don’t help you guard against inflation. Let’s face it. A fixed annuity is a “safe” and “conservative” investment. You will not incur a riskier investment’s potential gains (and losses), such as the stock market. But don’t forget inflation. If the annuity is paying you 3% and inflation is 5%, you are losing purchasing power. If you think you might live twenty years after you purchase an annuity, you are giving up the potential for a lot of future wealth.

Sales presentations often play on our fears with questionable date ranges. It isn’t uncommon for someone to use the last 50-100 years of stock market returns to point out the bad years. This can make their product seem like a wonderful benefit to keep you from poverty. It is better to look at full market cycles.

Are there bear markets and recessions? There are! But there are also roaring bull markets and inflationary cycles. These can last for a year or several years. This isn’t to say that you should not have a bucket of assets that are more risk-off. But be careful to then be more aggressive with your other investments. If every asset is low risk, you are courting long-term insolvency caused by inflation and higher living expenses.

Summary

I think annuities are costly and complicated solutions. They are hard for the average person to understand, and they are sold using graphs that make them appear to be a wonderful solution. If nothing else, enter the world of annuities with a dose of skepticism and a lot of questions. Expect answers in plain English. Just like with other investments, if you don’t understand it, don’t buy it.

The Last Installment is Coming

Next time I want to share how you can select the best annuity for your needs and will provide some web sites that can be helpful in the choice of an annuity.