A Balanced View

This is the second in a four-part series. It is easy for someone like me to determine that an investment or class of investments is “wrong” because of my built-in bias towards dividend growth and investment growth. My prejudices and preferences can cause me to reject some investments, like bonds, as “just a bad idea.” That is an unfair and one-sided view of just about everything in life. I say “just about” because there are times when truth is truth and truth is the only reality that matters. Having said that, it is only fair to say that there are good reasons some might want to consider some types of annuities.

Your Age Matters in the Decision Process

Annuities are more appropriate for a retiree when they are retired or plan to retire soon. Therefore, the advantages of an annuity are very age-driven. If you are not retired, or don’t plan to soon be retired, it is likely that an annuity is a poor substitute for other investment choices. So, the advantages of an annuity product are for those who have a fairly good idea of their actual living expenses and income potential in retirement. If for, example, you need $4,000 per month in retirement to pay for living expenses and only have $2,000 coming in from Social Security, you have a shortfall. This becomes a serious problem if you have not saved much for retirement. However, if you do have some retirement assets, you might want to take some of your savings and buy an annuity.

How does an Annuity Work?

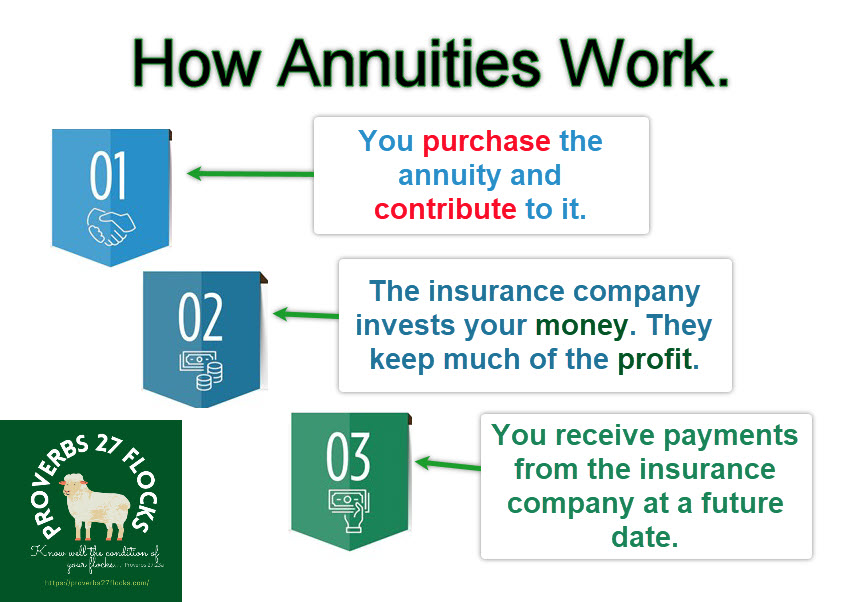

There are three main pieces to the mechanics of an annuity. You don’t want to get the first step wrong. It will greatly impact the second two pieces of the process.

The first piece is the BUYING AND CONTRIBUTING piece.

You must evaluate the annuity, understand the costs, understand the benefits, and understand how your decision today might impact your future. As part of the first piece, you can purchase the annuity when you sign the contract. This is a contract between you and the insurance company. Sometimes your payment is a lump sum, but you can also contribute to an annuity.

A single premium immediate annuity (SPIA) is a lump sum payment contract between you and the insurance company. It is designed to give you, the retiree, income “for life.” You make a single lump-sum payment and then immediately or with in the year start to receive income. So, if your Social Security covers half of your living expenses, an SPIA might be able to help you cover the other half.

Immediate annuities can provide an income stream within a month of purchase without an accumulation period. The immediate annuity rates depend on your single premium payment amount, the annuity contract terms, your age and your gender.

The Second Piece is the Insurance Company Work

What does the insurance company do with your money? They invest it. They want to make more than they give you for your money. They want a substantial profit from their investing efforts. In general, it is not unreasonable for the insurance company to expect average annual returns of at least 10%. So, if you give them a lump sum of $100,000, then after twelve months, they might have $10,000 more for their work. You won’t receive the extra $10,000. In fact, they now are investing $110,000 and hope to make another 10% in year two. So, year two gives them another $11,000.

What will you receive? It depends on the contract you signed. If they are promising you 5% payments on $100,000, then they are saying they will give you $5,000 per year as income. In general, that means you are getting about $415 per month in income. Therefore, if you need an additional $2,000 per month, you might have to give the insurance company $400,000.

Please understand this is far more complicated than how I have described it. You might receive more than $5,000 per year if your withdrawals are less than the growth of your account. But you should not expect to receive $10,000 in increased value in year one or $11,000 in year two. Rather, you might see growth of 1-2% because the insurance company is earning income from your account. How do I know this? Because I have seen it in actual annuity statements from friend’s annuity accounts.

The Third Piece is the Income You Receive

If you have a contract that promises to give you income, the final piece is receiving the income. This can happen relatively soon, or it can be delayed for some future date. One IMPORTANT piece of this puzzle in retirement is inflation. You can get an inflation-protection annuity but remember that if the insurance company is providing inflation protection, there will be a cost associated with this protection. Because inflation can easily average 3-5% or more, an inflation-adjusted annuity sounds appealing. Again, you will pay for this feature. The cost will be the difference between the “regular annuity” payment and a lower amount you’ll probably receive with inflation protection.

Types of Annuities

While there are many different annuity types, they can be broken into three main groups. The three are: fixed, indexed, and variable. They are what they sound like. You can buy a CD and get a fixed rate of return. You can buy an index mutual fund or ETF and expect returns similar to the index. You can buy a variable annuity that will behave like the performance of the investments you select.

So, you can pick the SPIA I mentioned earlier, longevity annuities, index annuities, fixed annuities, and variable annuities. I do not claim to understand all of them in depth. One of my blog readers told me about his Multi-Year Guaranteed Annuity (MYGA). A MYGA is a type of fixed annuity. A MYGA offers a guaranteed fixed interest rate for a certain period, usually from three to 10 years. LINK for MYGA

This Baird link will take you to a PDF that is a helpful overview of the different types of annuities. This also talks about some of the benefits of an annuity. BAIRD LINK

The Advantages of Annuities

Why did my mom have annuities? Primarily for simplicity of the income it provided and the ability to pass on some wealth to her children. She accomplished both. She had sufficient income to cover her living expenses and to give to her favorite charities and her church. She then left portions of her annuities to her heirs.

An annuity can provide retirement income for life. If you think your life might be longer than the income you can receive from your investments, then an annuity is a nice way to provide some safety. However, an annuity will not help your wealth grow as an investment in stocks or bonds might. Different types of annuities offer different levels of safety. This is the primary reason that some will want to purchase an annuity. You are buying something like a pension.

Annuities provide guaranteed returns. A fixed annuity can provide a guarantee earning a specific interest rate on the investment. Keep in mind that the rates offered with this option tend to be lower than what other options provide. However, it provides more predictability for future income planning.

There is market volatility protection. All investments have risk. Some annuities can help to protect you from dramatic bear markets. If the market declines after you purchase an annuity, the annuity’s value won’t get clobbered by the market. But be wise and remember that volatility by itself is not risk. Annuities don’t really protect you from all risks, including inflation and tax risks. So, an annuity that is 2% fixed, will still give a return even if the market decides to fall 25% in value for the year.

You can reduce risk by gradually annuitizing. Annuitization is the process of converting an annuity into periodic income payments. Once you lock in an annuity rate, you do face the risk that interest rates can rise. That means you miss out on some returns by choosing safety early on. The time to buy an annuity is when you’re ready to go to a lower risk solution, and it is best to do this slowly.

Like my Mom, if you die, you’re not going to lose your money. If you die earlier than is normal for your family, whatever “normal” is, you can structure an annuity to provide payments to a spouse or designated heirs like your children. Your money can provide guaranteed protections for yourself or the people you care the most about. The advantage here is the guaranteed protection. It isn’t about the overall value you receive at the end of the policy. The insurance company, please remember, is making a nice profit.

With some annuities, you can choose how your money gets invested. For a variable annuity, the process is similar to what it is like when you choose a mutual fund. You can always choose to invest directly instead of using this vehicle. This gives you more flexibility if you want to use a hands-off approach to investing. You can deposit your cash, choose your investment options, and then forget about it until you need to access the payments. Of course, you could just buy mutual funds and save the cost of the annuity.

A variable annuity can offer a death benefit. Variable annuities carry some risk because they have the potential to lose money. They also come with an extra benefit: a death benefit. That means the insurance company will offer payments or continue to pay out on the annuity to a designated beneficiary. So if you have a pension, and your spouse does not, an annuity could continue to provide your spouse with income if you predecease your loved one.

There are many types of annuities for investors to consider. Not all annuities are a good idea. In fact, I believe the list is a rather short one. In the end, choices are good, but they also make picking an annuity more complicated and confusing.

Some annuities may provide you with some inflation protection. But you only get what you pay for. If you want to ensure that your monthly annuity income stays on pace with the current rate of inflation, you can pay for that too. Inflation can have a devastating impact on your finances. It is easy to miss this because it happens little-by-little. However, if inflation is 3% per year, after ten years the buying power of each dollar is much smaller. In other words, the money held in your pocket would be worth 30% less in just a decade. The good news is that some of your costs can go down. If you have paid off all of your debt, you won’t have a car payment or mortgage payments.

Multi-Year Guaranteed Annuity (MYGA) Advantages

There is safety as MYGAs are not subject to market volatility. There is flexibility. Many providers offer provisions that allow partial withdrawals yearly without a penalty. There are tax benefits. You don’t incur any tax until money is taken out. Of course, some of these same benefits can be gained through other types of investments.

Historical Perspective – Military Pensions

The Single Premium Immediate Annuity (SPIA) “is the oldest type, dating back to the ancient Roman Empire. The word annuity actually comes from the Latin, annua, which means annual payments. Roman soldiers received lifetime annuity payments to compensate for their service in the military.” – Source: annuity.org

We do the same thing in the USA for those who devoted most of their working lives to serving in the army, navy, marines, or air force. It is a pension. So, if you have a pension, the advantages of an annuity seem to be less appealing. LINK

In the next post I will talk about the disadvantages of annuities. Then, in a fourth installment, I plan to share how you can select the best annuity for your needs and provide some web sites that can be helpful in the choice of an annuity.

Annuity Tips LINK

Single Premium Annuity LINK

Inflation Protection Annuity LINK

MYGA Annuities LINK