Why Statements Bring Perspective

There are two emotions that investors often have. Both of them are counterproductive and destructive. They are greed and fear. Another underlying problem is one of pride. Short-term success can cause prideful thinking that says, “I am smarter and better than the mass of investors on the planet.”

It still amazes me that one of my most popular posts in terms of number of readers was about the importance of reading your investment statement. There are many good reasons for a monthly review of your statement(s). They include an income review, a performance review, asset allocation reminders, and just a gentle reminder that you must have growth and income growth to cover growing inflation. (“How AND Why I Read My Monthly 80-Page Fidelity Statement – Only Four Pages Capture My Attention”). LINK

What Statements Don’t Reveal About You

They don’t say why you are investing. They don’t reveal your purposes. They don’t reveal your generosity or lack thereof. It is generally wise to ask the “why” question. Why are you doing what you are doing? What is your purpose for living? What do you hope to accomplish that is bigger than you? What will last? What does your investing and your use of your investments say about you?

What Statements Say About You

Oftentimes when I review a friend’s statement I notice several things. One thing is fearfulness. Some investments are chosen because they are “safe.” By “safe” I mean that the total dollars won’t drop because they are “invested” in cash, money market funds and bonds or bond funds.

Statements also reveal a lack of knowledge about investing in general and a potentially misplaced trust in an advisor. The statement can show a maze of hard to decipher investments, some questionable overlaps, far too much complexity, and an utter disregard for some basic principles like the “Rule of 72.”

What are Some Warning Flags in Statements?

Because I have seen so many statements, I have grown accustomed to seeing things that declare a lack of transparency on the part of the provider. For example, if the ticker symbols are missing and the investment (usually some type of mutual fund) doesn’t include a ticker symbol (like CMNIX) then I grow concerned. Mutual fund ticker symbols are five letters and always end in ‘X’.

Another warning flag is having more than 5-6 mutual funds in the portfolio. More is rarely a good thing. In fact, more funds in the portfolio is generally another warning that the advisor wants to appear to be an “expert” by increasing the complexity of the portfolio. They are hoping you just take them at their word.

Yet another concern is the lack of transparency about the total costs. Not only do the mutual funds have an expense ratio, but the investment advisor or broker may be doing things that are not in your best interest. If, for example, there is a lot of buying and selling of investments, generating trading income for the brokerage firm, you should be asking some questions.

Finally, there are the fees charged by the advisor for his or her work. Sadly, the dollars being spent are far in excess of the value received. When you add up the total costs (expense ratios (use Seeking Alpha!), trading costs, and advisory fees), which may take some time and effort, you may find yourself asking, “Why is this so expensive?” This becomes even more apparent when the stock market goes down, as it will at some point. Costs that are based on your total assets are an iceberg that will destroy your investment returns.

What I Look At Every Month

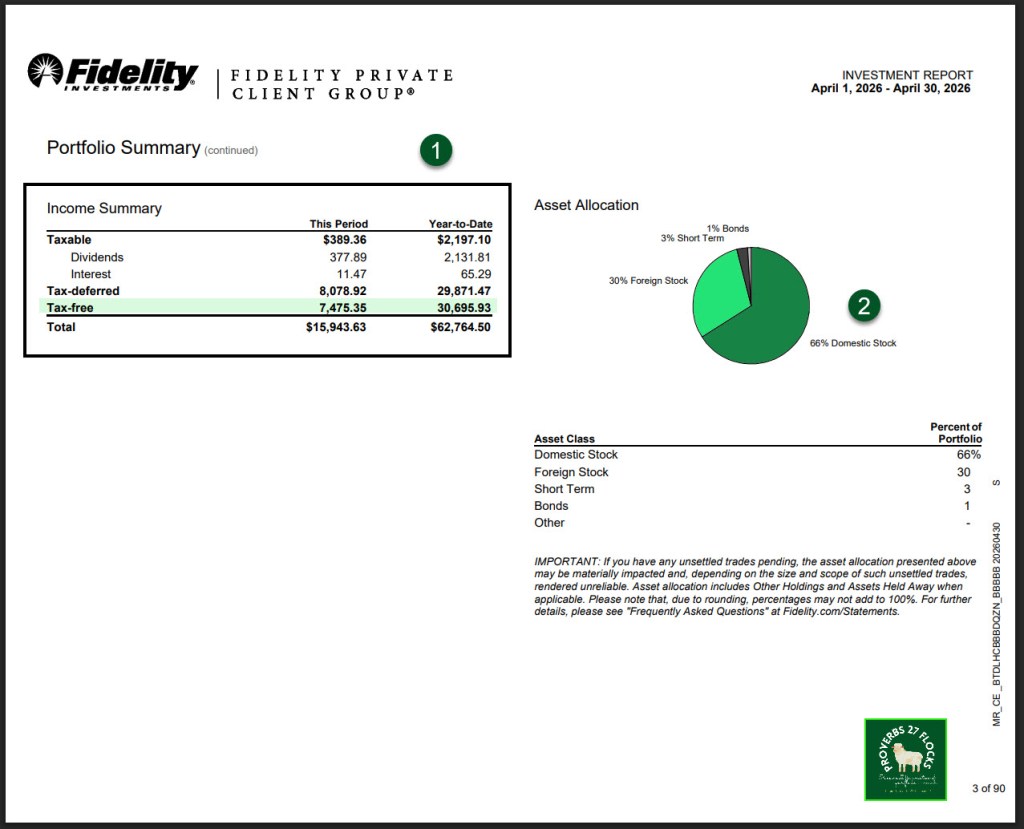

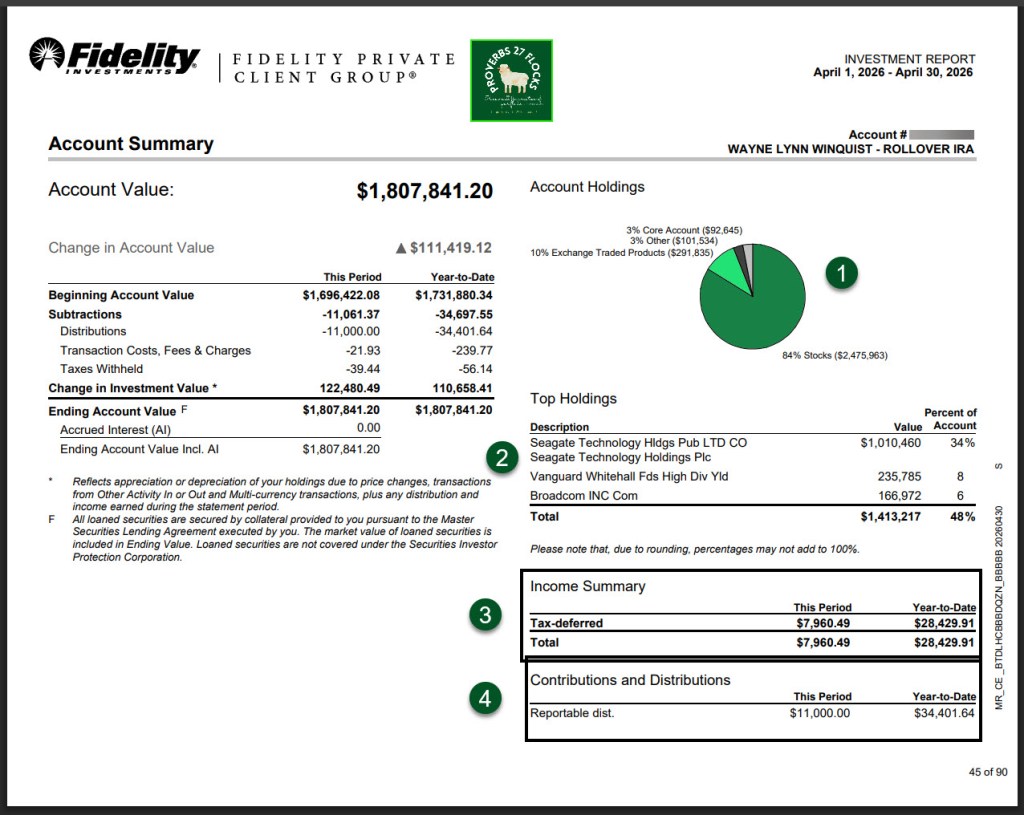

Our current statement is 90 pages long. It includes our eight accounts at Fidelity Investments. I don’t read all 90 pages. However, there are some pages I always consider. The first one is page 3. You might wonder why I don’t spend much time on page 1. It declares the “Portfolio Value” and Year-to-Date changes in total investment value. There are several problems with these numbers. While they are true, they don’t adequately reflect the total returns on the investments. They overlook the significant income from dividends. Page three reveals those truths.

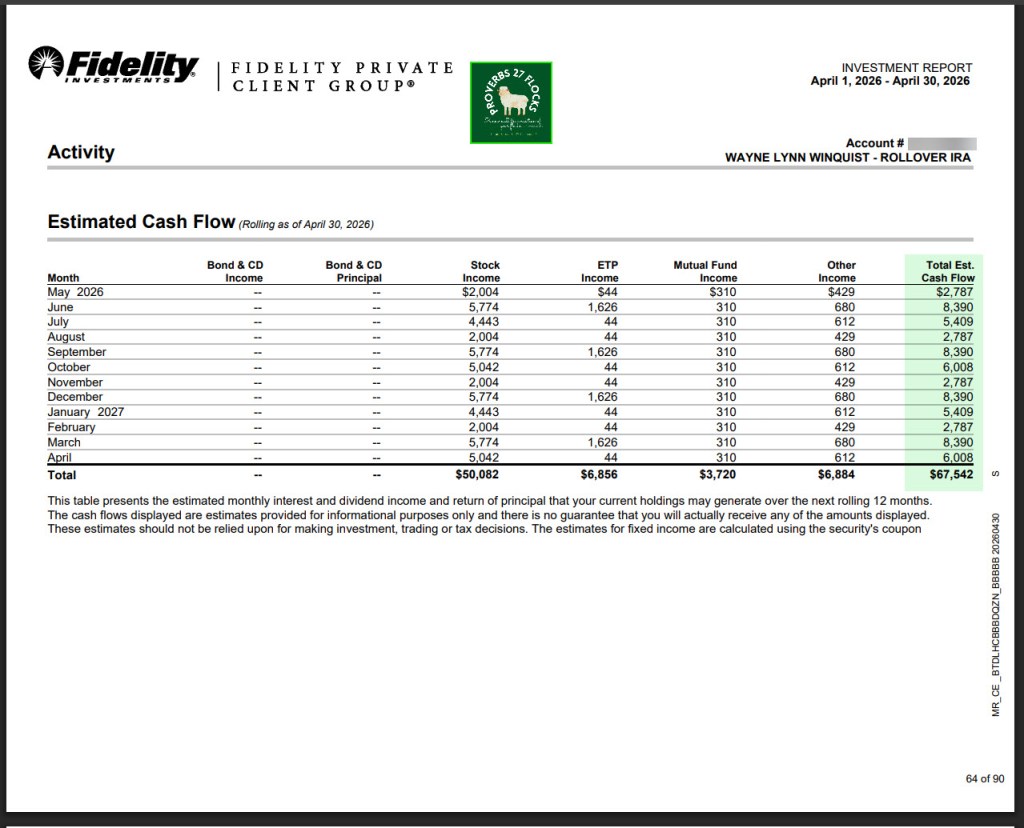

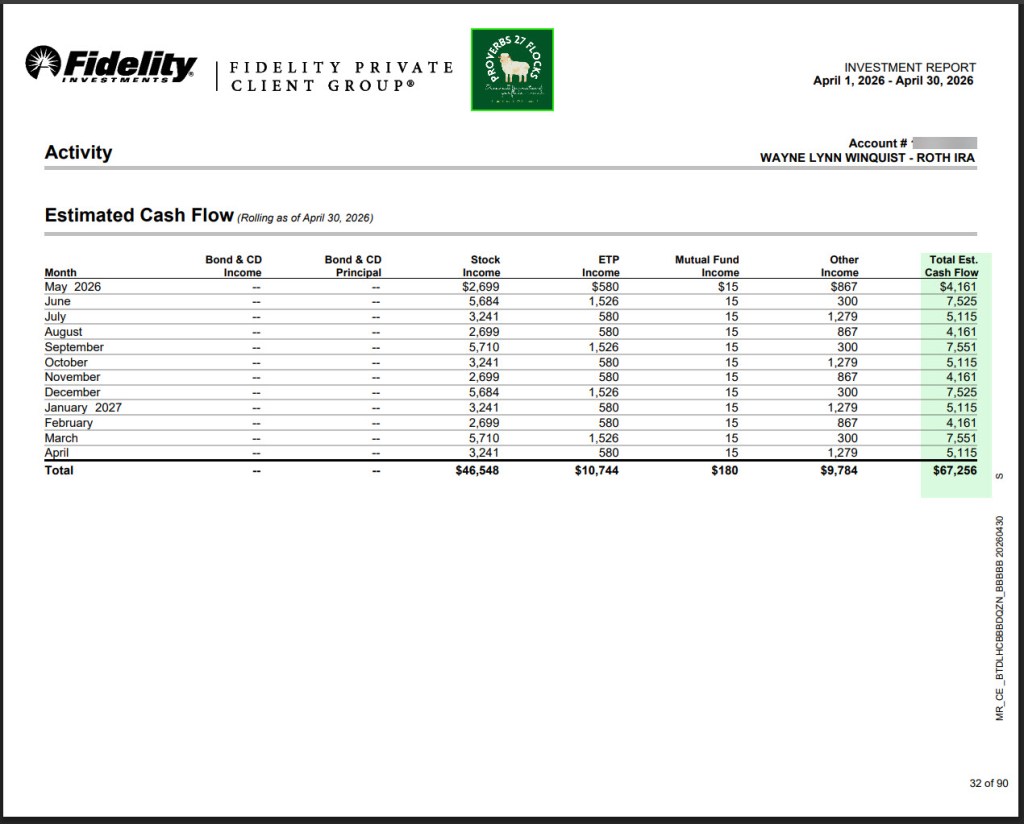

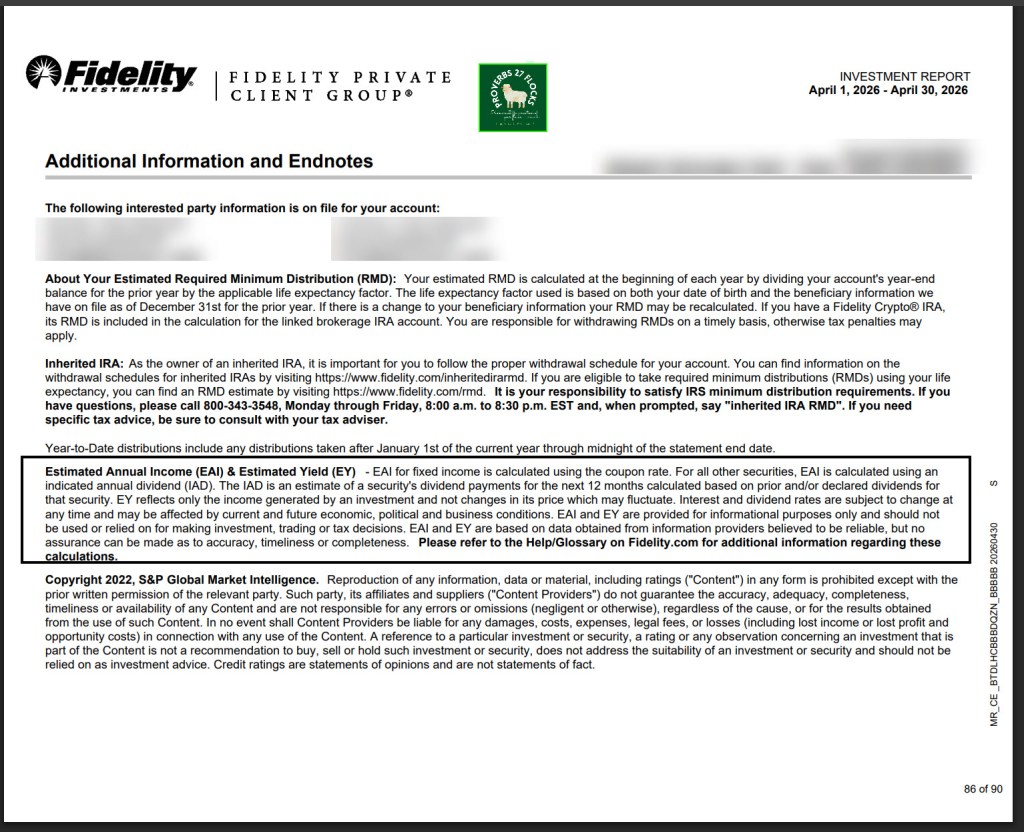

I’m also interested in Estimated Annual Income (EAI). This is especially true for my traditional IRA account, as I want the income to be greater than my RMD. Unfortunately, the Fidelity statement underestimates the EAI. However, it is a helpful reminder of the reason we invest for the future: income in retirement.

Here are a few pages from our most recent statement that I reviewed. As you can see, I only looked at pages 3, 32, 45, and 64. Page 86 contains notes about Estimated Annual Income.

From my statement page 85: “This table presents the estimated monthly interest and dividend income and return of principal that your current holdings may generate over the next rolling 12 months. The cash flows displayed are estimates provided for informational purposes only and there is no guarantee that you will actually receive any of the amounts displayed.”

“These estimates should not be relied upon for making investment, trading or tax decisions. The estimates for fixed income are calculated using the security’s coupon rate. The estimates for all other securities are calculated using an indicated annual dividend (IAD). The IAD is an estimate of a security’s dividend payments for the next 12 months calculated based on prior and/or declared dividends for that security. IADs are sourced from third party vendors believed to be reliable, but no assurance can be made as to accuracy. There are circumstances in which these estimates will not be presented for a specific security you hold.”

Recommendations

Read your statement. If you don’t understand what you are paying your advisor and the total costs of your investments, including trading costs and mutual fund expense ratios, dig deeper and ask questions. Look at the total EAI for your investments. Can you live off of that income in retirement? If not, you may want to have a plan to get there.

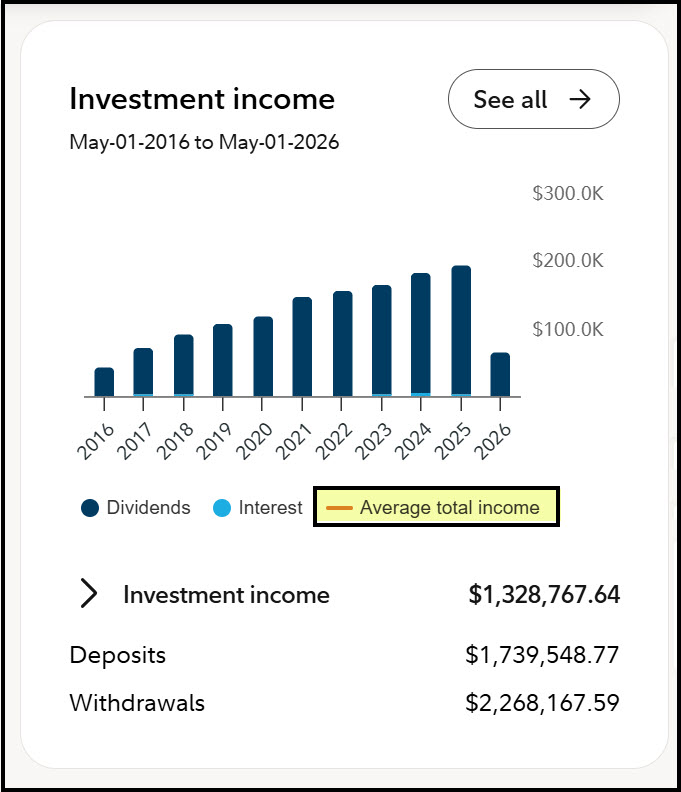

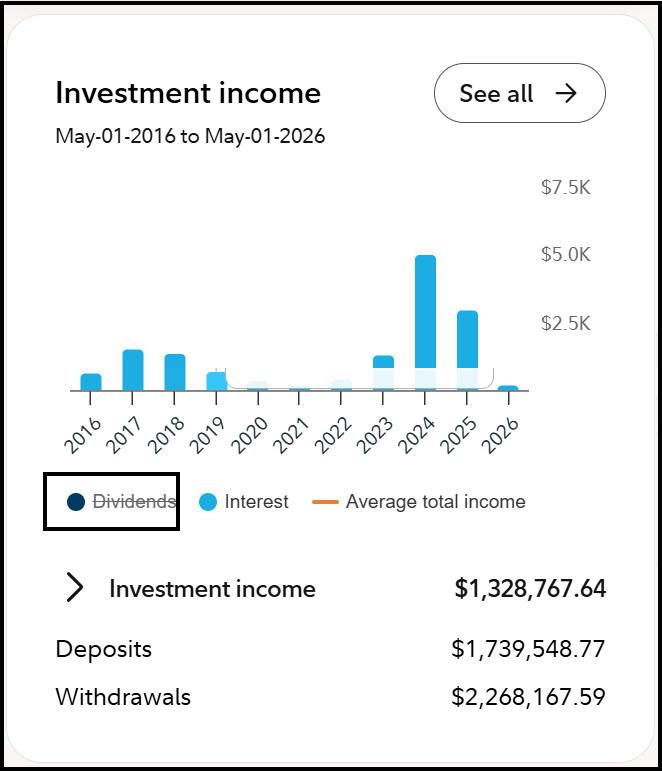

Here are some images from the Fidelity Investment’s Performance page for our investments. This view of history shows the “easy income” that has continued to flow into our accounts during a ten-year period.

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com