Costs and Expenses are Like Rust on Metal

When you purchase a car or truck, you may plan to keep it for ten years or more. Over time, you may get scratches, dents, hail damage, and, inevitably, rust on your expensive “investment” in transportation. Your vehicle usually depreciates the moment you drive it off of the lot. If you paid $45,000 for it, ten seconds later it may only be worth $43,000. Then, over time, the rust and other wear-and-tear on the prized “investment” continues to eat away at the value of your “investment.” There is an aspect of investing that is like rust on your hard-earned savings. You can see the rust in the investment prospectus.

I had planned to call this post “Danger Ahead: Annual Operating Expenses.” I obviously changed it and used the rust metaphor. However, there is real danger in ignoring expenses.

Did you ever read the investment Prospectus of a mutual fund? Most people don’t. “A prospectus is a formal document required by and filed with the Securities and Exchange Commission (SEC) that provides details about an investment offering to the public. A prospectus is filed for offerings of stocks, bonds, and mutual funds.” – INVESTOPEDIA

If you ignore the prospectus of a mutual fund, you will probably regret not taking the time to look at two illustrations in the prospectus.

The Rust of Expenses

Most mutual funds and ETFs have expenses. These are typically annual charges and are expressed as a percentage. For example, ETF VYM has an expense ratio of 0.06%. In general, I think most investments should have an expense ratio of 0.10% or less.

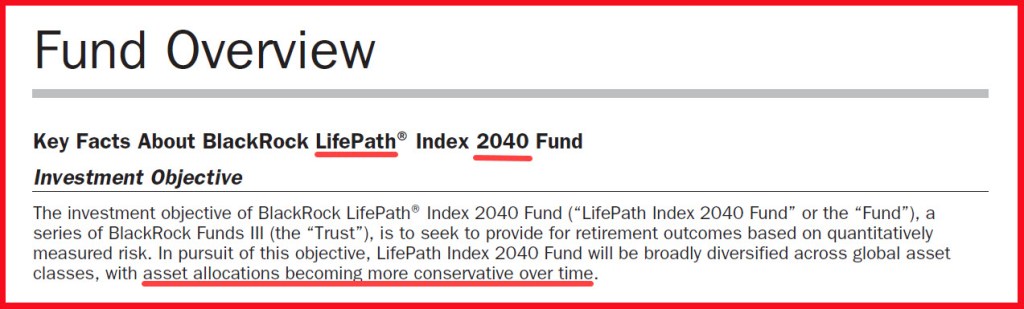

The LIKKX BlackRock LifePath® Index 2040 Fund Retirement has an expense ratio of 0.09%. That isn’t bad. There is no “front load” on the fund. However, the “P” version of the Index 2040 fund has an expense ratio of 0.39%. Even worse, the prospectus for the “P” shares shows a “Maximum sales charge”, also known as a load, of 5.25%. You need to know this. Why?

The reason is simple. If you put $100,000 into the “P” version of the fund, the fund manager skims off the load of $5,250. This is like driving a car off of the dealer’s lot. Therefore, your investment immediately rusts down to $94,750. On top of this insult, the fund will now charge you 0.39% for managing your $94,750. $369.53 is taken from you for that expense charge.

But it gets worse. Let’s assume your $94,750 grows to $150,000 in a couple of years. Now the fund is taking $585 each year your fund balance is at least that amount. Ten years later your investment in the P shares is $500,000. Now you are paying $1,950 per year for the fund to manage your investments.

Each of these charges reduces your total investable dollars. This may seem like a small thing in the first five years, but it gets very painful over time. Remember this one truth: the fund manager is not doing anything extra for the investor with $1,000,000 than he or she did for the $10,000. Over time, expenses are a terrible rust on your dollars.

The Rust of Lost Opportunity

When you invest in a conservative way, you also have growing rust that is compounded year-after-year. This means that your investment growth will be less, so the compounding on your total dollars invested will be less. If you are satisfied with 5% returns, or even 7% returns, you will have some total growth. However, target date funds tend to seriously underperform because they increase, year-after-year, the allocation in low or no growth investments like bonds. This has a compounding rusting impact on your total assets and your potential income.

The Risks of Target Date Funds

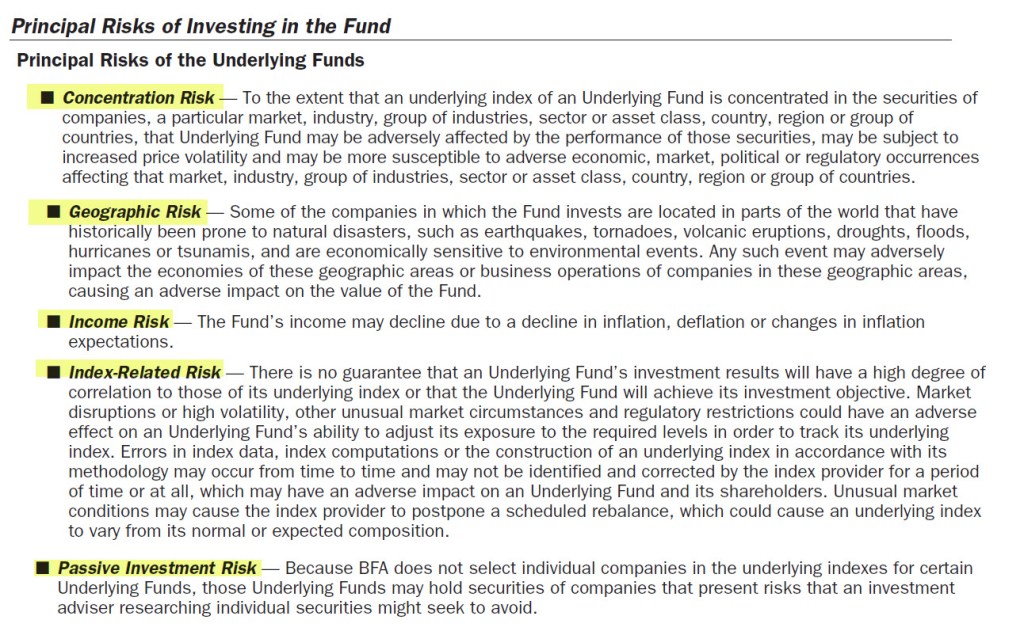

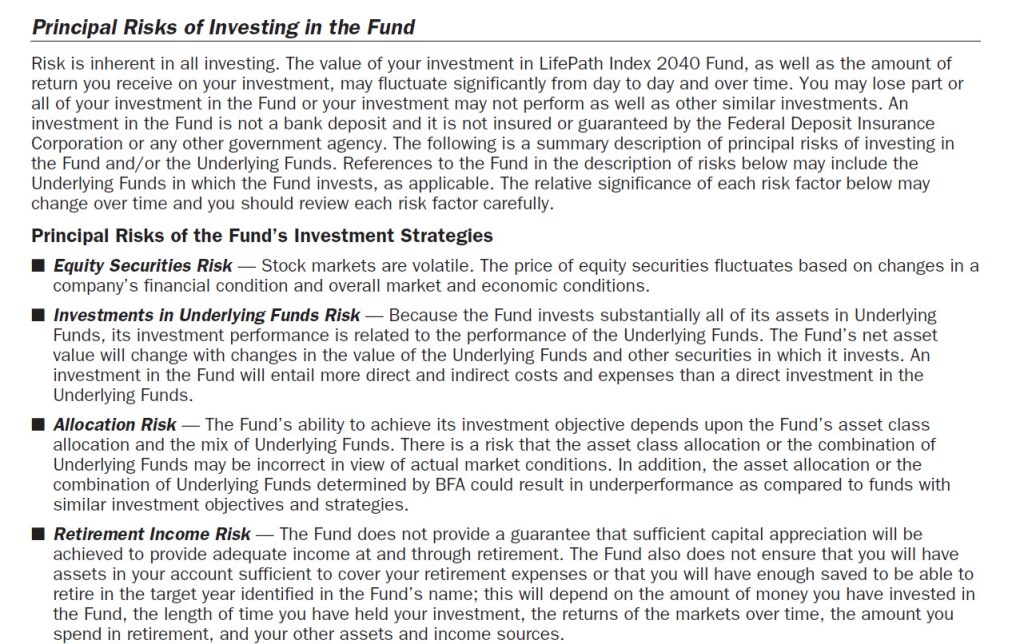

One other thing that novice investors overlook is the lack of true safety in any mutual fund. If you read the prospectus for any stock, mutual fund, or ETF, you will learn that you are taking on risk. Don’t think that the fund manager will give you any help if the fund plummets in value. You already paid them and they don’t offer refunds.

A Rule of Thumb Summary

Read the investment prospectus. Understand the costs of investing and then do some math with future projections of your total account value. You will be glad you did.

Want to Learn More?

Based on the question of a reader, I will do another post on this topic related to what older investors might want to consider when they reach their sixties, seventies, eighties, and even their nineties. You do need to think about your strategy as you get older.