The Alarm Bells Should Ring

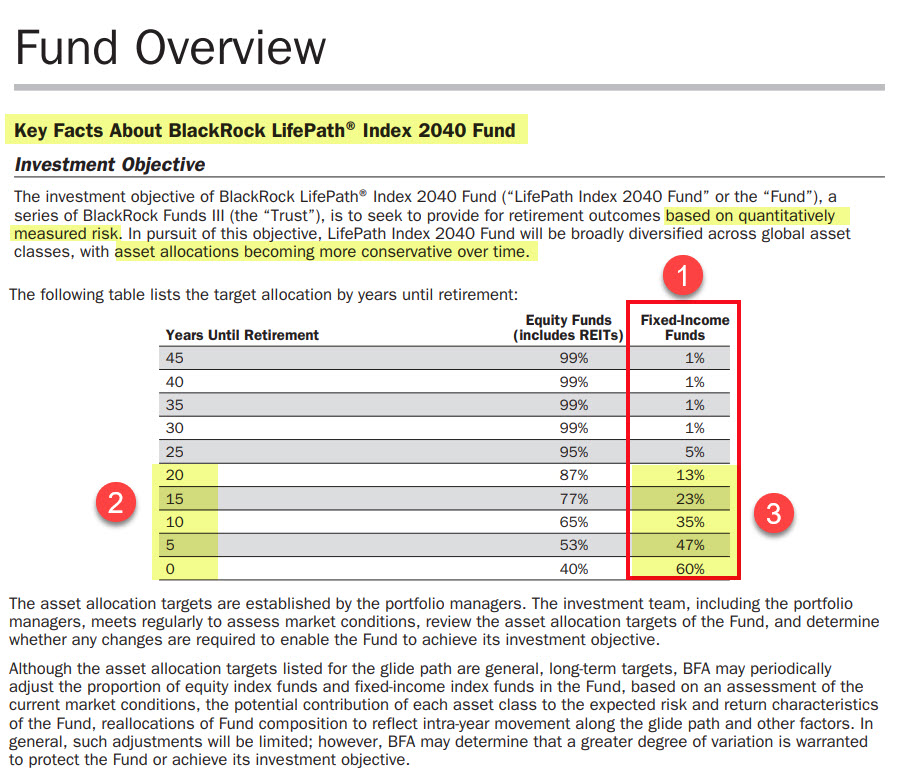

This past week I reviewed two retirement account statements. Both of them had a mutual fund investment with a year as a part of the fund’s name. The years that often appear are 2030, 2035, 2040, 2045, 2050, 2055, 2060, and 2065. The date approximates the target year when the investor plans to retire. Some examples of the fund names are, “BlackRock LifePath® Index 2050 Fund Retirement” (LIPKX), “Fidelity Freedom® 2040 Fund Other” (FFFFX), and “American Funds 2045 Target Date Retirement Fund® Retirement” (RFHTX).

What Is a Target Date Fund?

This type of fund is designed to simplify the choices of the investments in the typical 401(k) plan. Uniformed investors think they are getting a wise solution for the long term, because (on the surface) they appear to be less risky. “Target date funds provide retirement investors with a diversified mix of stocks and bonds that rebalance over time. Also known as lifecycle funds, target date funds gradually shift from more risky stocks to less risky bonds the closer you get to retirement.” SOURCE: Forbes

I created a simple bar chart to illustrate the common way that these year-centric funds work. Dear investing friend, please understand that increasing your bond allocation does not decrease your long-term investment risks. The more you have in bonds, the worse your long-term investment returns will be. This is not just my opinion. This is shown by long-term data from multiple sources.

What Do Other Investors Think?

It is easy to understand that I am just one voice and maybe I am wrong. Why would companies offer target date funds if they weren’t good solutions? There are several reasons for this, but most of them center on the fear of the employer and the fears of many employees. Both sets of fears are overblown. Caution is a good thing, but too much caution is debilitating and counterproductive. For example, bubble wrap is a good thing when packaging delicate items. However, too much bubble wrap is wasteful and does not add to protecting the item in question.

I asked the Fidelity Investor Community what they thought of target date funds. Perhaps I was missing something or perhaps had not considered enough target date funds. What follows are some of the comments I received.

Default funds are usually not the best choice. Some knowledgeable investors are concerned that employees don’t pick funds that are likely better choices for retirement and their employer defaults their retirement to a target date fund. Here is a portion of what Neli said: “Where I work, we have a 403b plan in TIAA. Right from day one, the employer contributes the equivalent of 9.3% of your salary into your 403B plan as the retirement plan. You also have the option to contribute, but if you do or if you don’t the employer still puts in 9.3%. New hires are defaulted to contribute 5% for their own contributions and can make a conscious choice to opt out to zero or change it, but most do contribute something. Every year, it automatically increases by 1% until it reaches 10%. But you have to go into TIAA (not too user friendly) and pick where you want to put it. If you don’t, (and many don’t), it defaults to a Vanguard 20XX fund, which is mostly matched to the year you turn 65. I have people come to me 10 years after they have been there. They have old plans from prior employers that were in S&P 500 Index, which is kicking the pants off of their current plans and they don’t understand why. People are begging me to do a lunch and learn series about financial topics, but I don’t have permission from work to do it yet.”

Sometimes bad ideas linger for a long time or mutate into something equally bad. For example, whole life insurance morphed into an equally bad version called universal life. A contributor called “charlesponzi” had this to say about target date funds: “I looked at them when the target date fad commenced. There’s no there there. They remind me of the Dual-Purpose load funds back in the day. They promised both income and capital gains, they produced neither. Adding insult to injury, they charged a 9.5% front end load.”

Bonds are Not Your Best Friend. The problem with 20xx funds is that they grow in a bond allocation over time. That dramatically reduces your chances of success. The contributor “mucker” has quite a few helpful things to say. First of all, mucker understood some principles about stocks and bonds that many do not understand. Here is what he said, “I consider myself lucky that both my parents tried to teach me about investing at a young age. I know I have made errors in my investing life, but I have learned from those mistakes. I also have been lucky with some investments. I chose an aggressive approach to investing. I thought if stocks return 9% per year and bonds 6% on average, if I invest in stocks my whole life, I’ll be so far ahead by the time I turn 65, I can afford stocks to go down by 1/3 and still be ahead.”

Expenses are a key factor. Many target date funds under-deliver and over-charge for those shoddy results. Contributor “mucker” continued: “If I wanted to invest in a fund the first things to look at are what are the expenses. FIOFX has an annual expense of 0.12%. SPY has an annual expense of 0.09%. LIKPX has a load of 5.25% and an annual expense of 0.39%. Why not just allocate percentages to low-cost ETF’s? A do-it-yourself strategy.” Mucker also repeated what Neli said, as follows: “Many 401K’s will put you into a target fund automatically if you don’t make choices. When I worked, my 401K had an option where they would review your allocations and make recommendations. I tried it since it was free. It said to sell everything and invest the proceeds in a target fund. I started laughing. They just didn’t want to be liable for making a bad recommendation.” Don’t miss that last sentence. Target date funds protect the employer from being charged with providing “risky” solutions. Those less dangerous solutions don’t consider the terrible impacts of inflation.

The impact of dividend growth is muted and hindered in a target date fund. Bonds do not typically have growing income in the same way that good dividend growth stocks do. Mucker said this: “I think the best bet is to educate them on how to invest individually into funds. Find a good dividend aristocrat fund that will give them a raise every year. I do respect you for trying to teach others like my parents taught me.”

A Rule of Thumb Summary

If I could have new investors learn just one rule of thumb, it would be to avoid any mutual fund with a year in the name of the fund. There is no freedom in a “Freedom®” mutual fund. The life path in a LifePath® fund is s dangerous path for the long-term investor who may live for 30 or more years after they retire. A target date fund will generally cause you to miss your retirement investments target.

The second thumb is that expenses matter and that bond income less expenses is not as desirable as picking some good stock funds and then having a mindset that volatility is not the same as risk when you have a long-term perspective.

Want to Learn More?

I plan to write a second post called “Danger Ahead: Annual Operating Expenses.” Target Date funds not only under-deliver, then take away assets that should be helping you grow your retirement fund.

Hey Wayne — Very interesting evaluation of target date funds, and very pertinent for investors in their beginning and middle years of wealth accumulation. How about us oldsters who have far fewer years to manage our portfolios? Folks in their 80s— what’s your take on investing for most likely the short-term? I’d appreciate your thoughts and suggestions for the very golden years. Thanks in advance, and I genuinely enjoy your postings. — Jerry Uhlman

>

LikeLiked by 2 people

Hi Jerry, That is a very good question. I will address that question in a future post. Maybe I will make this a three-post series. Wayne

LikeLiked by 1 person