Does Your Advisor and Funds eat like T-Rex or a Mouse?

If you had a choice between having a Tyrannosaurus eating away at your investment accounts, or a mouse, which would you choose? We don’t really know much about the T-Rex, other than what we can learn from the skeletal remains. But it is probably safe to assume it had a good appetite. A single mouse, by way of contrast, can eat very little and be satisfied. Some investments eat away at your assets like the T-Rex, and some investment advisors are also very hungry.

One of my readers, Greg H., shared a helpful website link with me. Larry Bates’ website is a way to get your “Your T-Rex Score.” Your T-REX Score tells you how much of your investment return you will actually get to keep after the T-Rex, or the mouse eats their share. The T-REX Calculator allows you to determine T-REX Scores for an endless range of scenarios. A link to T-REX is included at the end of this blog post.

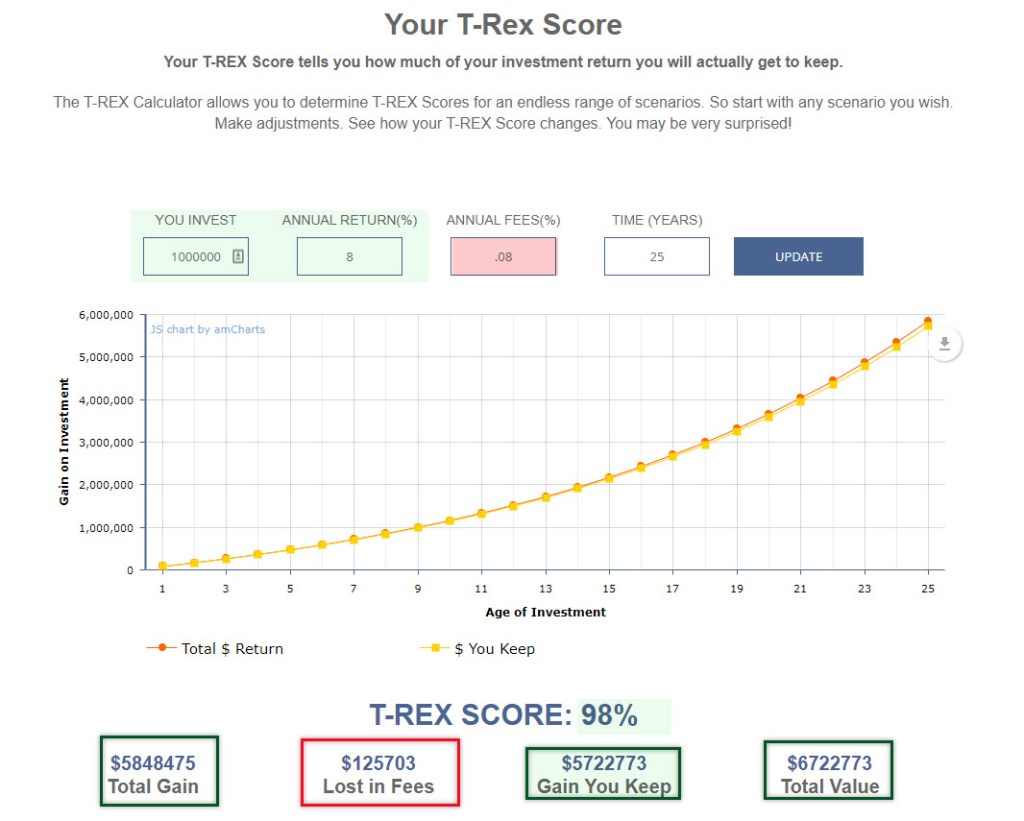

The thing I like about this tool is that it illustrates the drain that advisory fees and expense ratios have on an investor’s portfolio. If, for example, your advisor has been able to get you 8% returns and he or she does that for 25 years, they charge you for their work. What you might not realize is the total dollars you are giving to your advisor and to fund managers is quite large. This knowledge might cause you to rethink the way you invest.

Because every advisor, and every ETF or mutual fund has different costs, it is sometimes difficult to know what you are paying in total. I have certainly seen advisors who charge 1% or more for their services. It is not uncommon to find mutual funds that charge 0.65% or more. ETFs generally have lower costs. For the sake of illustration, I will use 0.65 as the total cost. However, I know some investors who pay at least 1.5% in total. What does this really mean and what are the real costs?

Three Examples to Get You Started

Example One: You Only Have Ten Thousand Dollars

What happens if you have ten thousand dollars today and your advisor gets you 8% returns and charges you 0.65% (fund expense ratios and advisory fees combined)? Instead of having $58,485 25 years from today, you are left with $48,891. Just remember inflation when you look at that number. Twenty-five years of inflation is a real killer. But it gets worse if you give your advisor one million dollars.

Example Two: You Have One Million Dollars and an Advisor

Pretend you are 65 years old when you retire, and your investment accounts have reached the one-million-dollar amount. While you might not live another 25 years, perhaps your spouse will. What happens if you have a million dollars on your 65th birthday and your advisor helps you realize 8% returns and charges you 0.65% (fund expense ratios and advisory fees combined)? You lose almost one million dollars, but you will have almost six million dollars. Perhaps it is worth it.

Example Three: You Have One Million Dollars Invested Differently

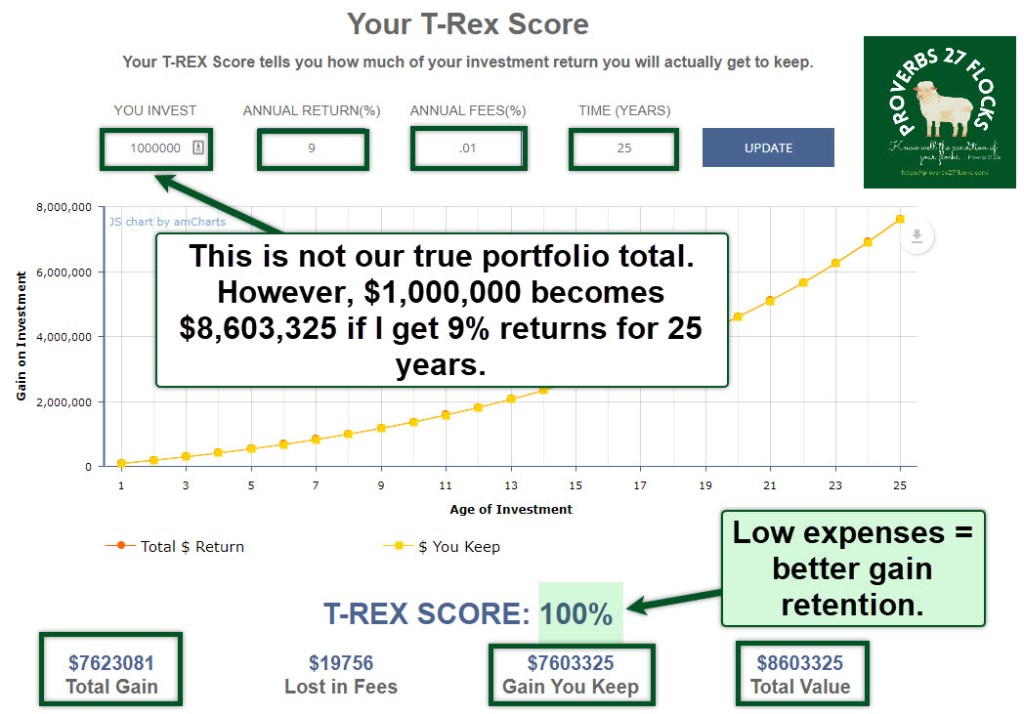

What happens if you have a million dollars today and you manage your own investments? You have learned enough about investing to buy good index funds, low-cost ETFs and you don’t pay an advisor. We will assume 8% returns and assume the expense ratio average for all of your investments is a reasonable 0.10% (fund expense ratios averaged). You lose only $125,703 in fees and you will have almost seven million dollars. Perhaps it is worth it to manage your own investments. Don’t forget inflation. After 25 years seven million dollars is worth less than seven million dollars today.

My T-Rex Score

Here is my T-Rex score: 100%. It is reasonable for me to average at least a 9% return per year. Our expense ratios across our entire portfolio are less than 0.01%, but I used that value just to get the score. The reason our expense ratio is so low is that we own both low-cost ETFs and a lot of individual stocks. If your investment advisor can get you 15% returns, perhaps that advisor is worth what you are paying them. Are they doing it or not? Don’t let your dividend growth feed your expense ratio!

T-REX LINK

The T-Rex Math Explanation LINK