Keeping Income Taxes and Advisory Costs At Bay

When we say something like “I have a home security system to keep the burglars at bay,” the words “at bay” mean that the burglar is unable to move closer to our possessions because of something in their way. My doctor prescribed an antibiotic to help fight a bacterial infection and keep it at bay and repel it. We use vaccines to teach our body to attack invaders and keep them at bay. In other words, we want a safe distance from burglars, bacteria, and other bugs in our body.

Apparently, this idiom came from hunting. It describes an animal that has been driven back and now faces pursuing hounds. There are other legal burglars (and burglars might be too strong of a term for some advisors and fund managers) or hounds that can greatly diminish your income growth and income flow. Therefore, in this final post of the series, I want to review, at a very high level, the opportunities to keep more of your income and keep taxes and expenses at bay. There are some tactics you should consider.

The Tax Man Cometh

First of all, as a follower of Jesus, I do not practice tax evasion. I practice tax avoidance within the requirements of the law, or at the very least, tax reduction. There are a couple of strategies for keeping these costs low. Far too many investors do not think about income taxes as a part of their retirement income flow. If you have a one-million-dollar traditional IRA, you might think you have one million dollars of spendable income. If you think this way, you are probably living in a dream world. The very nature of a traditional IRA exposes you to taxes at some point in the future.

Keep Records Throughout the Year

There are probably as many ways to keep records as there are online budgeting tools. I started using Quicken at the end of 2021 and it helps me see things like our various expenses and investment allocations at a very high level. But for a better understanding of our income, possible itemized deductions, and estimated taxes paid, I have a spreadsheet. As income arrives, I take one minute to add a line to the income tax spreadsheet. I also have formulas that tell me the tax obligation for both the federal and state income tax authorities. Charitable giving and local property taxes are also included as a separate sheet, so that I can monitor our likely total itemized deductions.

If all we had for income was our Social Security income and my wife’s part-time income, our total taxes would be almost inconsequential. However, I must also account for capital gains from three taxable brokerage accounts, interest income (which is now starting to grow) and for withdrawals from our traditional IRAs. By keeping records I can work on another piece of the long-term tax strategy.

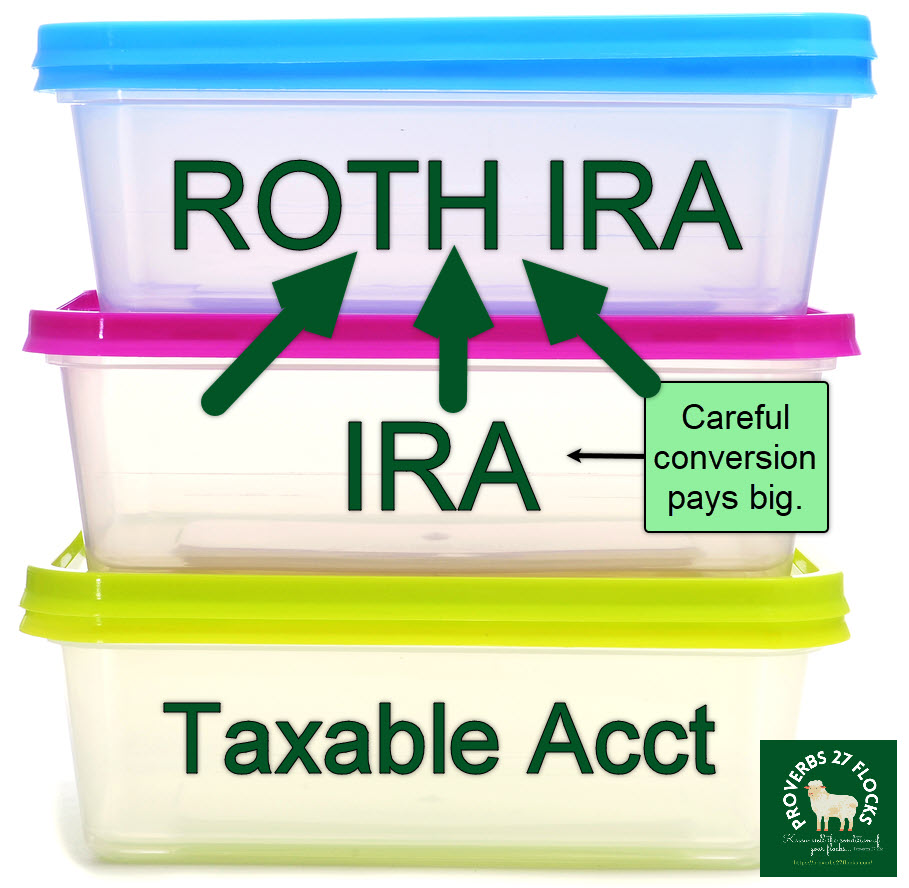

Converting Assets from an IRA to ROTH for Dividend Growth

The power of moving assets from a traditional IRA to a ROTH is a compelling way to increase income by reducing income taxes. In my case, there have been four tax-related benefits to increase our real income. The goal: increasing income and reducing income taxes so that charitable giving can increase.

Bear markets or investor pessimism have given me gifts in the past. On April 18, 2019, I moved my 500 shares of ABBV from my IRA to my ROTH IRA. The shares at that time were worth $77.57 so my total tax burden was $38,785. I had paid more than that for the shares, so they had a cost basis of about $42K. The shares are now worth $81,530. If those shares had been left in my traditional IRA, I would have a bigger tax burden to face, not to mention all of the dividends that have been paid since I did the ROTH conversion.

The total of the last fourteen ABBV quarterly dividend payments in my ROTH is $9,098.03. That income is free of income taxes. Furthermore, the quarterly dividend had been $535 in August 2019, and it is now, due to another dividend increase, $740 per quarter. Therefore, I not only legally avoid taxes on the substantial capital gains, I have zero taxes on the increasing income, which increases our real annual income by $2,960 from ABBV dividends. The reason for the total income is that ABBV announced yet another dividend increase. That new dividend is payable in January 2023.

But the story doesn’t end there. I trade covered call options on my ABBV shares. I have received $1,215.76 in income for thirty-three covered call trades on only 200 of the shares.

But even that isn’t all. During the time since the conversion I have purchased ABBV shares in my ROTH and sold them for a capital gain. For example, I bought 100 shares of ABBV in February for $146.75/share and sold them one month later for $157.50. That was also tax-free.

This brings my total potential tax-free gain to $54,159. Of course, until I sell my 500 shares, that number is very fluid. However, the point is that I can do anything I want with those shares and all of the resulting income is tax-free.

Rules for Protecting Dividend Growth

Before I move on to the cost of getting investment advice and the costs of the ever-present fund expenses, remember that there are other subtle things wise investors will notice. I have buy and sell rules in my written investment plan. One of my sell rules is, “If a company reduces, suspends, or otherwise eliminates a dividend, sell that stock.” I have done that more than once. If the goal is increasing income, you don’t want to hang on to investments that are taking you in the opposite direction. It is better to recognize the mistake, sell the asset, and buy something that will perform.

For example, I owned shares of a REIT with the ticker symbol ILPT (Industrial Logistics Properties). The investment had been paying a quarterly dividend of $0.33 per share. In July the dividend was reduced to $0.01 per share. I have no patience for that type of income reduction. My loss on the sale of my shares was over $8,000 (excluding dividends I had received). It was obvious to me that I could put the remaining $6,400 to work in a better dividend growth investment.

It would have also been possible to move my shares from my traditional IRA to my ROTH IRA. Had the future looked brighter for ILPT, I might have considered that move.

The Cost of Having Advice

Another big drain on income is the cost of professional “expert” advice. I am using the term professional to mean any broker, advisor, or firm that will help you with your investments. In my opinion, if even a novice investor took half of what they are paying an advisor and bought some good books on investing and took 1-2 classes on investing, they would realize their advisor is probably doing very little work for some significant dollars. Sadly, I have helped far too many friends come to that realization, often after their advisor has already done some damage or underperformed the market. Finding a good advisor is not, in my opinion, an easy task.

For example, I recently helped some three different friends who were each paying at least $5,000 per year to a local investment advisor. I asked them how often the advisor met with them. The answer saddened me. Furthermore, when examining their investments, I quickly realized that the advisor was playing it “safe”, and the resulting portfolio performance and income flow was just short of awful.

If you are going to pay an advisor $5,000 per year, then they should be working at least 50 hours for you and with you. Even then, realize you are paying them $100 per hour. In order for them to be worth that amount, you should be seeing excellent portfolio and income growth. Guess how much it would cost you to buy two good investment books. Less than $100 is the number I would suggest.

Of the dozens of people I have trained, only one (to my knowledge) went back to a different advisor. Sadly, he picked an advisor that I suggested he avoid. I don’t have much hope that he will be very happy with his decision ten years from now when he wants to retire. However, I will admit that some people just cannot, or do not have the time to do the work needed to have income growth as a part of their thinking.

I liked what lucky737 said in the Fidelity Investor Community: “The best thing about having an advisor, is that if the portfolio does not do well, you have someone to blame.” That is a small consolation if they have ruined your retirement and charged you $5,000 annually to do that. Think about it. Who is responsible for picking the investment advisor? You are. So you can also blame yourself.

The Cost of Fund Expenses

Another huge drain on your increasing income can be the increasing costs of the funds you or your advisor pick. This can sneak up on you. The best way to understand this creeping giant is to give you an example. If, when you start investing at age 25 you have $10,000 in your IRA and you pick funds that have an average expense ratio of 0.65%, then you are paying $65 per year for their work. Even if the total expenses were 1.0%, you are “only” giving up $100 on that $10K.

Over time you add money, and by the time you are 35 your investments are worth $100K. Now you are paying $650 per year (if the balance stays at $100K) for the very same work. At 45 perhaps your investments have grown in value, and you have continued to add dollars so that your total investment is now worth $700K. You are now paying $4,450 per year for those funds.

Each of these reduces the assets that are working for you for income growth. While some investment managers might be worth the 0.65% expense ratio, almost 95% of the time I can find a comparable investment that only charges 0.04%, 0.08% or even just a paltry 0.10%. You have a choice, so examine the choices. That is one of the reasons I chose ETFs like VYM, DGRO, SCHD, and ONEY. You don’t have to overspend to get quality investment management. Costs reduce income.

Wrapping Up this Series

My goal was to get you, my reader, to think about a goal, a strategy, and some tactics for increasing income and reducing the costs to get that result. I have not covered every possible way to accomplish the goal. You could buy real estate and have income from that investment. But you would also have to spend far more time managing your investment than I spend on the REIT’s I purchase. When thinking about how you approach investing, don’t neglect the least plentiful resource you have: time.

Summary

Always ask the question, “what will this investment choice or approach cost?” Reduce costs. Reduce taxes. Educate yourself. Ask your advisor the tough questions. Ask questions about their answers.

What Might You Do?

Consider starting 2023 with a goal statement that helps you focus on the investments that will help you reach your goal.

A Reminder from King Jesus

Jesus is my King. He is, as Handel declared, “King of kings, and Lord of lords.” There is a cost to following Jesus. But the costs are minimal in light of eternity. You have to have a long-term perspective about your life.

“Whoever does not bear his own cross and come after me cannot be my disciple. For which of you, desiring to build a tower, does not first sit down and count the cost, whether he has enough to complete it? Otherwise, when he has laid a foundation and is not able to finish, all who see it begin to mock him, saying, ‘This man began to build and was not able to finish.’” Luke 14:27-30 ESV

The Messiah Hallelujah Chorus by George Frideric Frederick Handel King of Kings

Coming Soon

I plan to start a new series on options trading. The series will focus on four or five methods I have used to increase our income in 2021 and 2022. I hope you follow my blog and continue to learn.

“My goal was to get you, my reader, to think about a goal, a strategy, and some tactics for increasing income and reducing the costs to get that result.”

Mission accomplished. Thanks.

LikeLiked by 1 person