Annuities May Help You to Enjoy Your Hard-Earned Money

Earlier this year I did a series of articles on the subject of annuities. The five posts were:

- Annuity Questions Everyone Should Ask – Why This Topic Matters

- Annuity Advantages – A Balanced View

- Annuity Disadvantages – A Balanced View Requires Asking Good Questions

- Annuity Selection Should Be Data Driven with a Blueprint – The Wrong Place to Start is Being “Sold”

- Building a Self-Paying Annuity – An Alternative to an Annuity

You can find these posts by scrolling down to the Category list on the left side of the main page. Just look for “Annuity”, which is the first category. My personal favorite category is “Dividend Growth.”

In the post about annuity disadvantages I wrote the following: “Without additional costs, annuities don’t help you guard against inflation. Let’s face it. A fixed annuity is a “safe” and “conservative” investment. You will not incur a riskier investment’s potential gains (and losses), such as the stock market. But don’t forget inflation. If the annuity is paying you 3% and inflation is 5%, you are losing purchasing power. If you think you might live twenty years after you purchase an annuity, you are giving up the potential for a lot of future wealth.” When I wrote that in March 2022, I had no idea what we would see for inflation. Now we know the brutal truth.

How to feel Financially Secure in Retirement

Fear seems to be a key motivator when it comes to annuities. Because an annuity is a fancy insurance product, it is sold as “protection.” People like to feel secure, and there are some annuity features that would lead a potential buyer to think the annuity will bring a sense of security.

At the beginning of this month, Fidelity wrote a post in the Fidelity Investor Community with some links to some articles in the Learning Center. Both links are included at the end of this article. One of the articles was titled “How to feel financially secure in retirement.” This article suggested that “An income annuity may help cover essential expenses in retirement that aren’t already met by Social Security or pensions.” It also said, “Fully covering essential expenses with lifetime guaranteed income sources can provide peace of mind that you’ll never outlive your money, no matter how long you live.” And, thirdly, they stated, “Annuities can also be simpler to manage and help provide greater protection against elder fraud and abuse than can an investment portfolio alone.”

Benefits of Annuities Revisited

The article listed five benefits of annuities. 1) Income that never runs out. 2) An easy, predictable paycheck. 3) Income no matter what the markets do. 4) Added protection against abuse and fraud, and 5) Confidence to enjoy your money. Let’s examine these benefits.

1) Income that Never Runs Out

Because an annuity is a life insurance product, it depends on the ability of the insurance company to provide the income. If an insurance company has a solid reputation and credit strength, then it is true the income will likely continue for as long as you live. However, without an extra rider on the annuity contract, the income gets smaller and smaller over time due to inflation. One dollar in 2022 may only buy fifty cents of products and services in twenty years.

Furthermore, like other insurance products, the strength of an annuity’s guarantee relies on the credit strength of the insurance company.

2) An easy, predictable paycheck

This is very true. However, it really isn’t much different from the first statement. Income is income and even Social Security is an easy predictable paycheck. I know that from nine years of collecting Social Security benefits. Even better, Social Security did not ask me for more money up front. I already paid my taxes, so another chunk of money wasn’t needed to start getting my easy, predictable, Social Security direct deposit to our checking account. The added plus is that I am getting a nice inflation increase in 2023. A basic annuity does not.

3) Income no matter what the markets do

This is the “feeling secure” part of the sell. It depends on how you view the stock market. If you think the market will go down year-after-year, then an annuity does offer some feeling of security. But that security can be short-lived if inflation continues to chisel away at the value of the income, “no matter what the markets do.”

4) Added protection against abuse and fraud

Sadly, there are many who look for ways to take advantage of the elderly. If you lock up funds in an annuity, it becomes harder for a family scoundrel or an unscrupulous broker or advisor to take advantage of you. So I suppose this is something to consider. On the other hand, if you are unable to manage your finances on your own, you should have an honest personal representative that will take care of managing your investments and paying your bills. If you don’t, no annuity will really bring you the full protection you think you need.

5) Confidence to enjoy your money

This one makes me smile. I guess some people think an annuity will bring joy. Again, as you get older, the things that bring you joy aren’t related to your money. If that is where you find your joy, you will miss out on the things that really bring joy.

Reviewing the Five

Numbers 1, 2, 3 and 5 are all geared to making the reader think only about the income side of the equation. I could combine all four into a single statement: “Buy an annuity for income from an insurance company that will give you a predictable paycheck and reduce your anxiety when the markets are going down.”

I think number four is of questionable real value. Some of the agents who sell annuities seem to fail to really educate potential clients as to the downsides of annuities. I’ve been to many presentations and don’t recall hearing a balanced view.

Fred’s Wisdom and His Interesting Mattress Solution

One of the responses I saw to Fidelity’s post made me smile. His first name is Fred. Fred said something very wise. He said, “Annuities are promoted as ‘guaranteed income’, but in fact, for most of your life all the income your investment generates goes directly to the insurance company. All you’re getting is a small portion of your original (non-refundable) investment back. So for example, if the annual payout is 5%, it would be 20 years before you even got your original investment back, and that would be with depreciated dollars. You could get the same result by putting your money under your mattress and taking out 5% of the original amount for 20 years. And that’s with no interest, so even if you put in something very conservative, like a money market fund, you’d likely have lifetime income.”

Another prudent investor said, “I’ve looked at them over the years but the interest rate on annuities never seems competitive. I seem to always be able to arrange better future cash flows by building a ladder with government and other investment grade bonds.”

Bonds Versus An Annuity

When I think about the options, as much as I dislike bonds, I would consider buying some bond ETFs or mutual funds long before I would buy an annuity. The only problem I would have is finding a bond fund that wouldn’t make me wince due to the current inflation and the market’s rejection of the bond in favor of short-term CDs. So that leads me back to where I would encourage you to go.

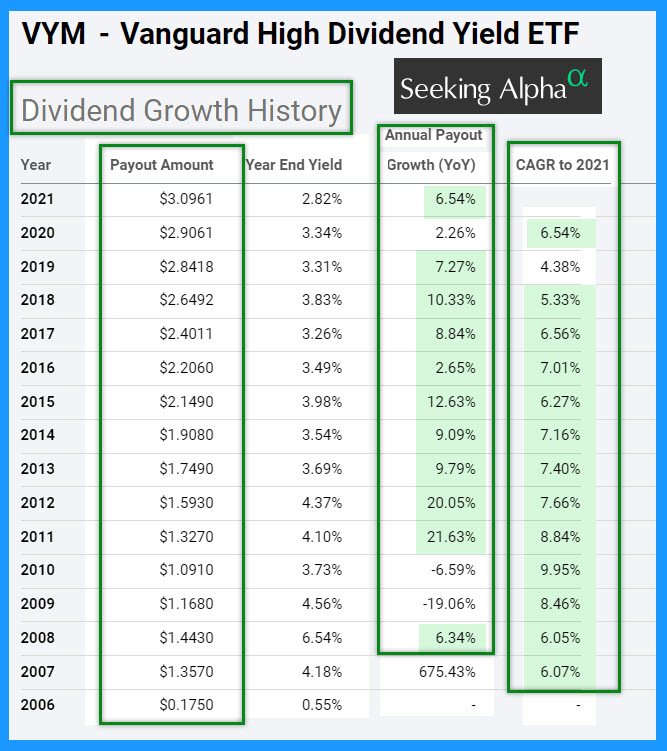

That leads me back to dividend growth ETFs. In the last ten years VYM has appreciated in value 129%. No bond and no annuity will do that. The Vanguard High Dividend Yield ETF was formed on November 10, 2006. It has been paying growing dividends for eleven years. The five-year dividend growth rate is 5.81%. Here is the data. Don’t buy an annuity unless you want the “benefits” that are offered.

Links to Fidelity Articles about Annuities