Why You Should Do This and What to Know

Every month I glance through my Fidelity Investments Statement. Our statement is 78 pages long and contains information about our eight investment accounts. Two of the accounts are traditional IRAs, two are ROTH IRAs, and the other four are taxable brokerage or money accounts. Reading 78 pages every month is not a good use of my time. But there is a good reason to read some of it.

There are two things you should look for in your monthly statements. You should look for motivations for you to stay invested. Then you should look for things that might be problem areas to address. This can be done in less than 15 minutes. Of course, you could spend more than 15 minutes, but I don’t see a need to do so.

If you have a different broker, you might want to see if your statement tells you what mine tells me. I have been generally disappointed in the statements that friends have shown me from other providers. If the statement is confusing or hard to read, then you might have a broker who doesn’t want you to know some important things about your investments. If you don’t see the fees that a full-service broker or advisor charges, then you need to look more closely. You will see at least quarterly fees if you have someone managing your investments for you. Far too many people do not read their statements.You should.

Reasons to Stay Invested

There is no reason to invest if you don’t have a plan to spend or give away the results of your investing activities. If you are interested in income and if you want to see what your income is and potentially will be, the Fidelity Investments statement will help you understand this aspect of your investing life. This has value for both the retired individual and for someone who is trying to think about what their retirement income might look like down the road.

Calculating Potential Future Retirement Income

Most people will have two primary sources of income in retirement. One source is usually Social Security. The other source will either be dividends and interest or income from selling investments plus dividends and interest. I believe the best long-term model is to seek to base your income on Social Security plus dividends and interest. For the more advanced investor, you can also add in covered call options income.

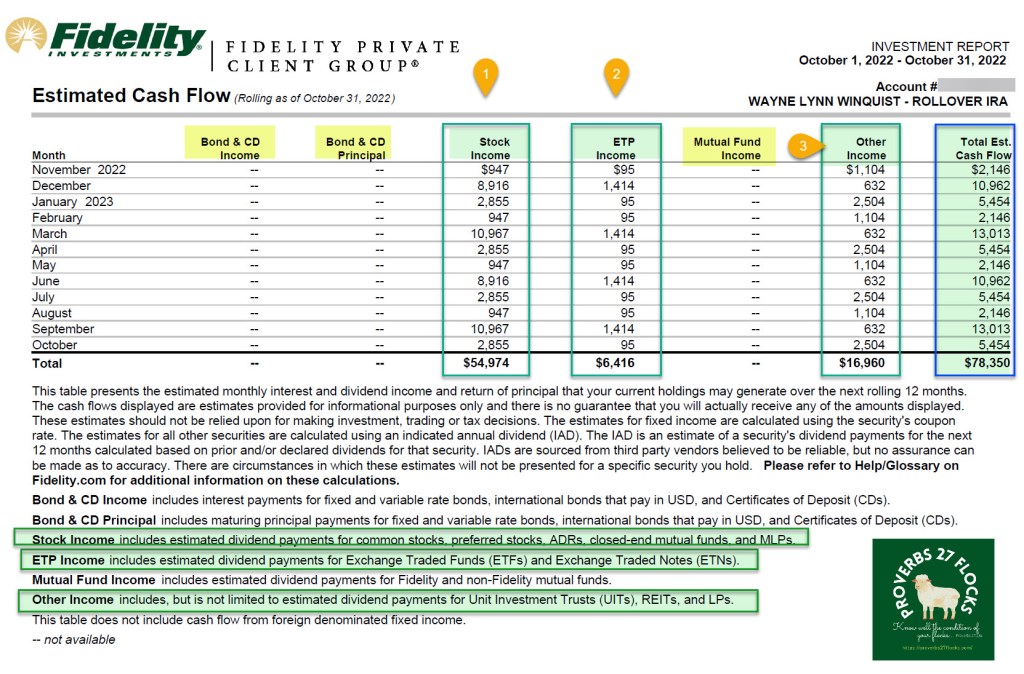

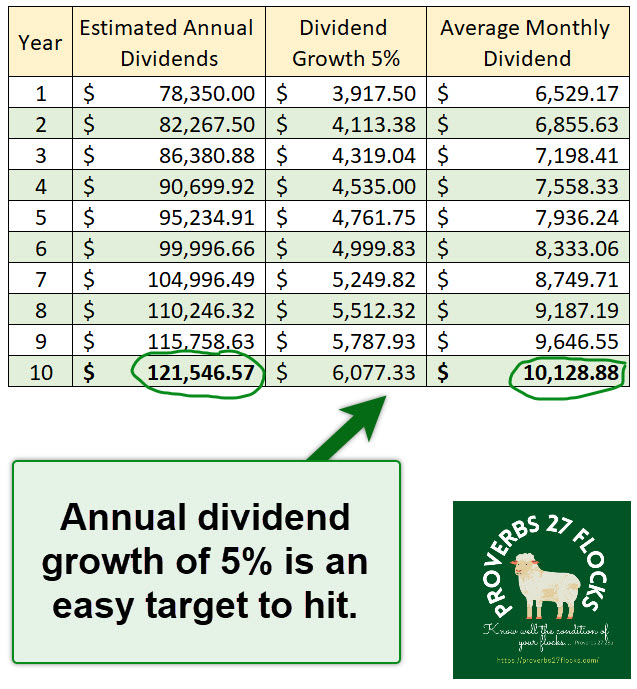

If you look at your Fidelity Statement, you should see a page that says “Estimated Cash Flow” for each account. Here is an example. It shows, by month, the estimated income for each of the next twelve months. This includes stocks, ETFs, mutual funds, and “other income.” As you can see on this sample, because I don’t invest in bonds in my traditional rollover IRA, I have no bond income. The total estimated cash flow from my IRA is $78,350.

Let’s pretend I have not retired and still have ten years to grow my retirement IRA account. Let’s further assume I can create dividend growth of an average of 5% per year. Using a spreadsheet or a calculator, I can see that I should set a goal of $121,546. This will be just over $10,000 in income per month ten years from today, if I choose investments that focus on my goal. By the way, five percent dividend growth is a very reasonable goal.

This goal-setting exercise will give you reasons not to panic and sell your investments during a bear market decline.

Setting Long-Term Goals

Before I retired, I set a goal to achieve $60,000 in annual dividend income by the time I retired. This goal was not pie-in-the-sky wishful thinking. This was based on a strategy that included dividend growth and reinvesting the dividends. This income, plus Social Security, would give us sufficient income for all of the normal expenses in our budget plus much more for giving and for large purchases and vacation travel.

Looking at your monthly statement can help you see if you are increasing your potential income or not. If you set a goal, you should track progress towards that goal.

Problem Areas to Address

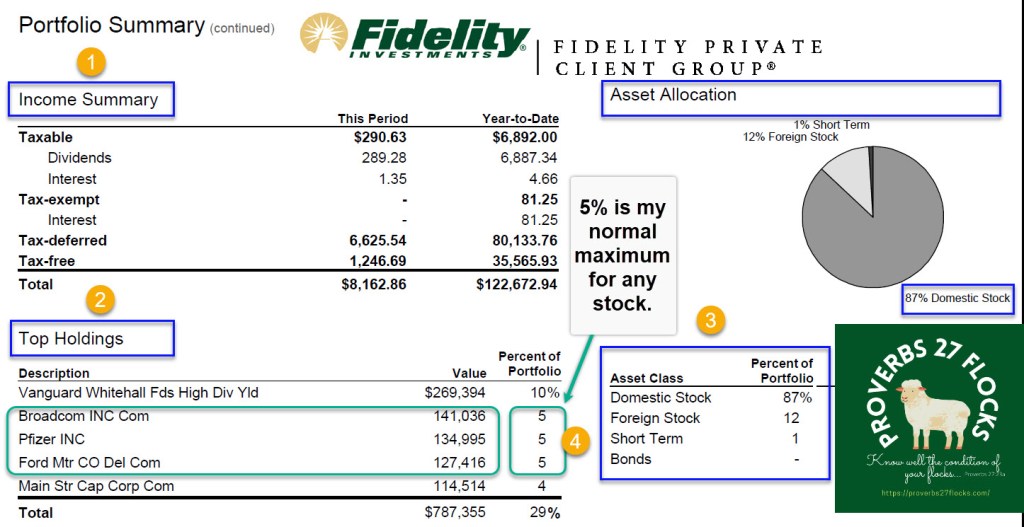

If you have too much invested in a single company’s stock, this can be a problem. The Fidelity statement can help you pinpoint areas of potential trouble. For example, if you have Apple stock, and that stock is 10% of your total retirement savings, then you might want to revisit that allocation.

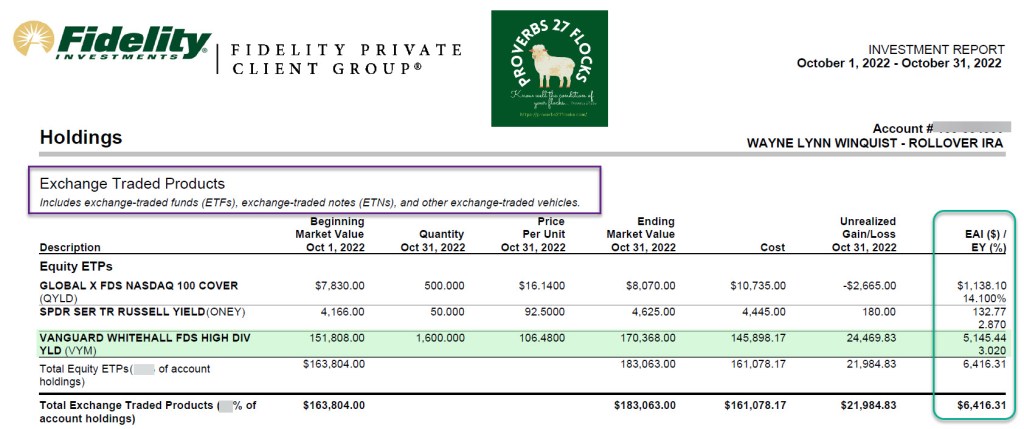

What is Missing from the Fidelity Statement

One thing you won’t see in your Fidelity Statement is the drain on your investments from the ETF or mutual fund expense ratios. However, if you have been careful in your selection of these investments, you should not need to see the total cost of owning the ETF or mutual fund shares. For example, VYM has an expense ration of 0.06%. If the value of my VYM shares is $170,000, then my expenses for this ETF are $102 per year. This is insignificant compared to the estimated dividends of $5,145 per year.

thanks for the update Willie dónnett

LikeLike