Reason Number Four for Loving the Bear Market

This is the fourth in my loving the Bear Market series. When hordes of investors are bearish it is likely that overall sentiment (outlook, opinion, attitude, feeling, emotion) is negative. The AAII organization does regular polls of investor sentiment. I love the current bear because I don’t have to make any income, investing, or giving decisions based on sentiment. Furthermore, the bear market sets me up for some great ROTH conversions! This is true today and might also be true in early 2023.

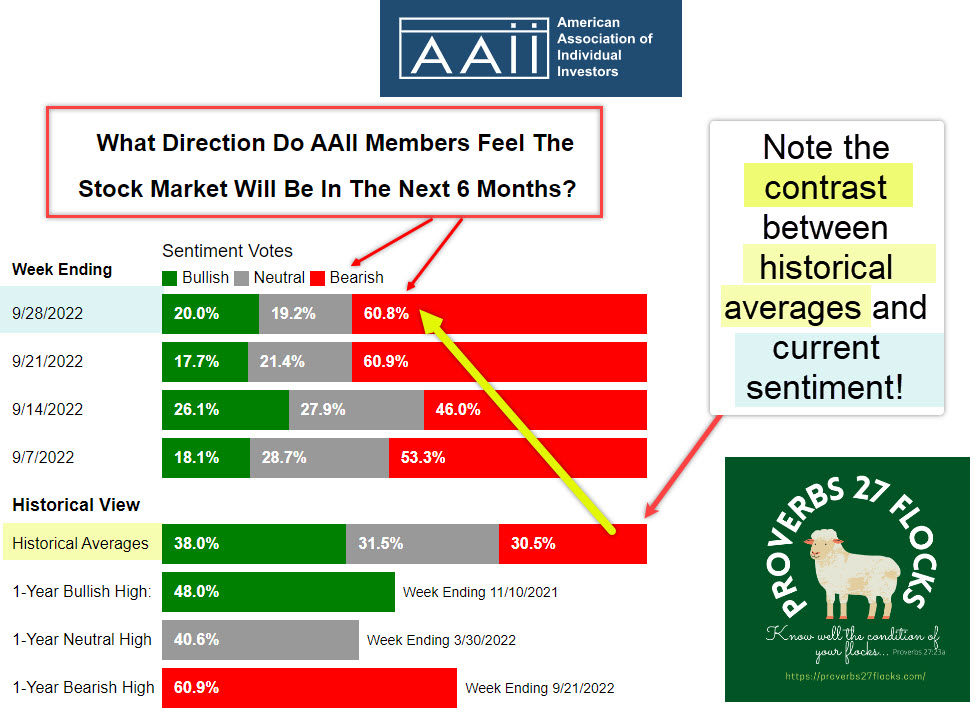

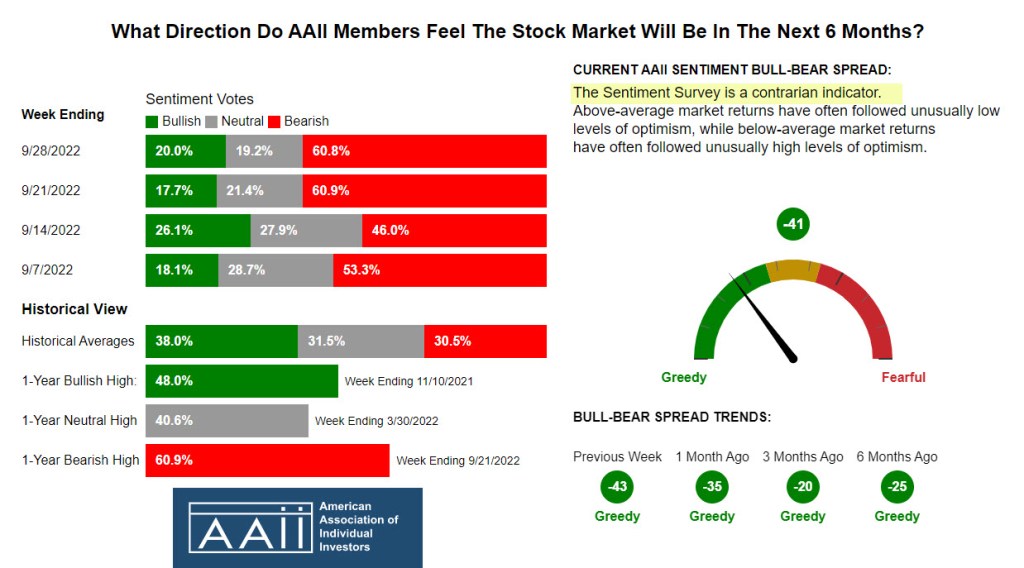

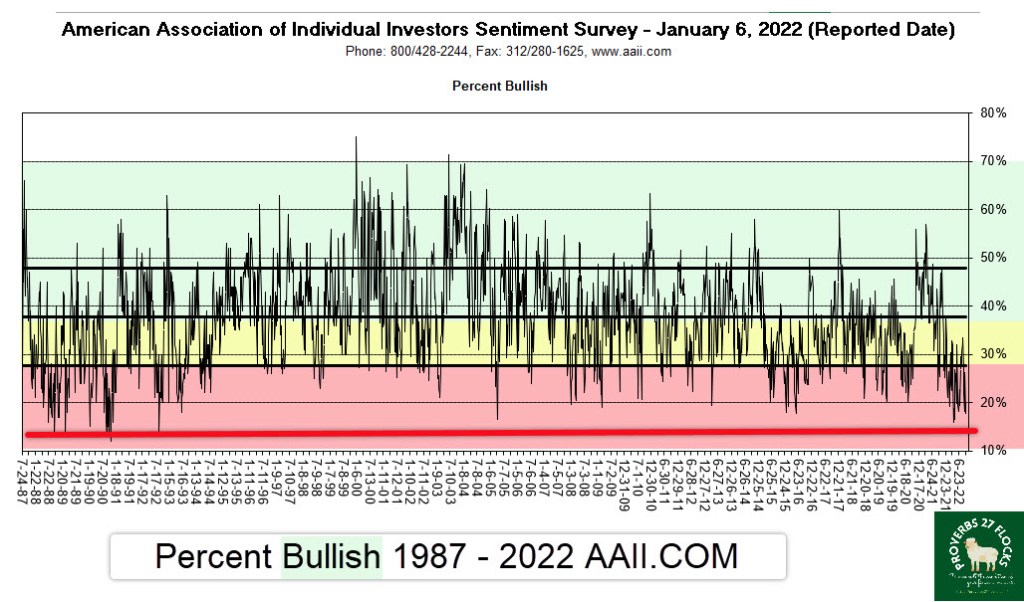

“The latest AAII Sentiment Survey shows that the percentage of individual investors describing their six-month outlook for stocks as “bearish” rebounded to its highest level since 2009. Plus, this week’s bullish sentiment reading ranks among the 20 lowest in the survey’s history.” AAII LINK

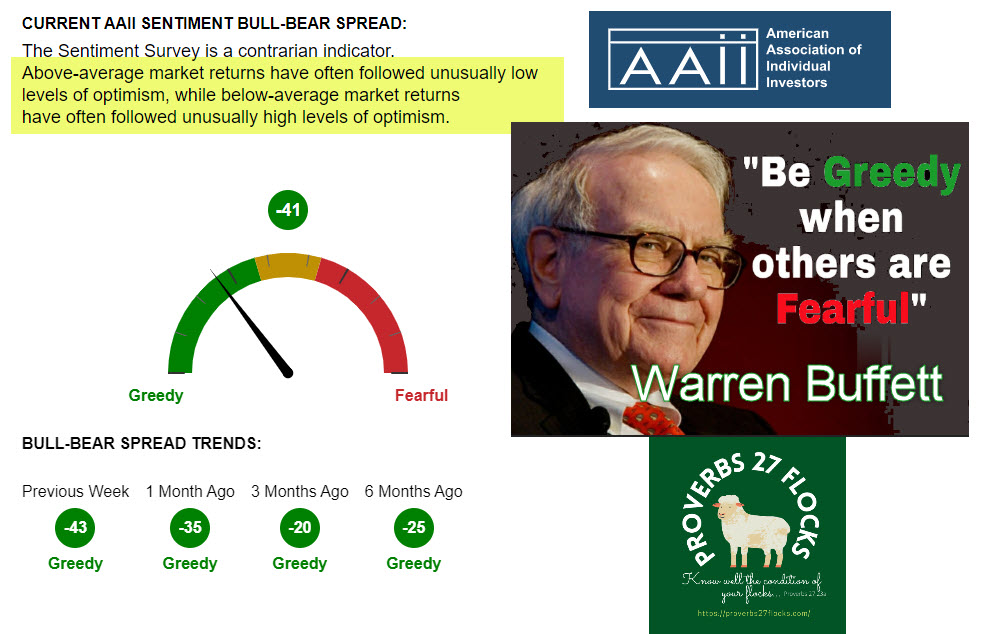

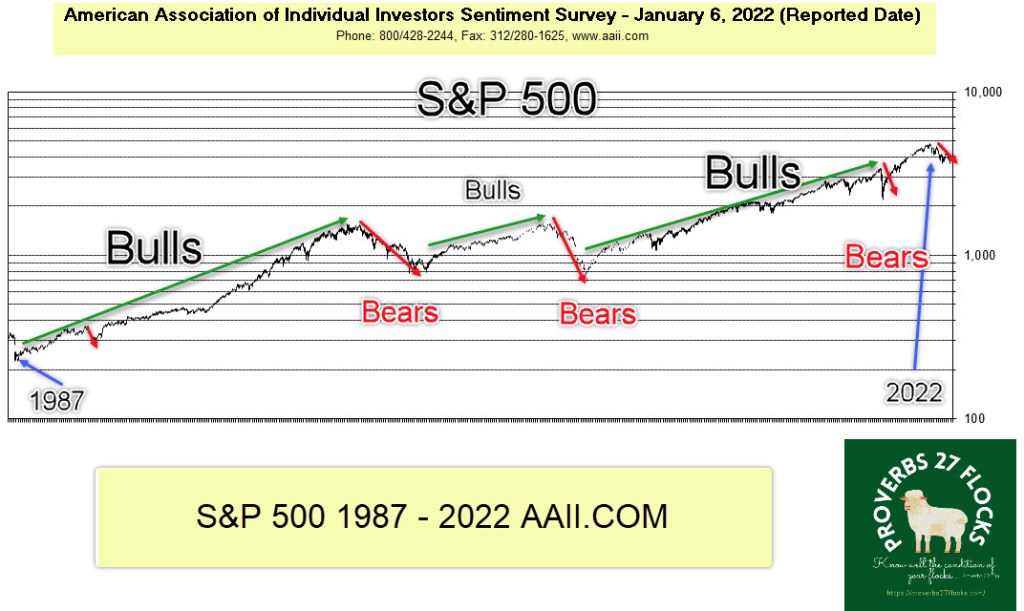

Warren Buffett once said that it is wise for investors to be “fearful when others are greedy, and greedy when others are fearful.” (Chairman’s Letter, 1986) His statement is a contrarian view on stock markets. It relates to the price of an asset: when others are greedy, the bull market races higher in irrational ways. One should be cautious lest they overpay for an asset that subsequently leads to poor returns.

Some of the people I have advised in the last couple of years ignored my cautions about the top-heavy nature of the S&P 500. They felt good because the index was riding higher. It was riding higher, but not because of the 500 companies in the index. It was a rush to the top for a select few large-cap stocks. Having said that, when others are fearful, this may present a good investment opportunity. In other words, I like to substitute the word “greedy” with “opportunistic.” Opportunity is knocking.

Required Minimum Distribution and the Bear

If my traditional IRA account balance is battered by the bear through the end of the year, I will have a 2023 RMD that is lower as a result. This gives me more opportunities to do IRA-to-ROTH conversions during times when the bear market is still active. As I look at our current positions, and total income for 2022, we can still do a ROTH conversion without creating a higher Medicare Part B premium.

Remember this truth before you reach age 72: You must take your RMD before you can convert any other assets from your traditional IRA to your ROTH. Conversions don’t count towards your RMD requirement. In just over a month, the projected RMD I will be required to take in 2023 has fallen by over $10,000. This is wonderful news. It means I can then use that $10,000 buffer to move some other positions from my IRA to my ROTH at a lower cost basis in 2023. Then, the dividends and any growth will appear in my ROTH. This increases our tax-free income.

Furthermore, as it stands today, incoming dividends in my traditional IRA will more than cover my 2023 RMD, even if the bull market returns. That means I don’t have to sell any positions during a bear market to get cash for the RMD. The extra cash from dividends can still be withdrawn to be used as gifts for family or for non-profits my wife and I support.

You should develop a retirement strategy for both income and giving well before retirement. Don’t listen to the radio talking heads that ask you to come in for a free analysis of your portfolio and help in changing your portfolio from growth to retirement income. You could and should be doing that today.

Remember, if you are a growth-focused investor, you can and will feel the pain when you have to sell investments to cover the RMD, especially if the bear market is in control when you retire. Let me say something that may not be obvious. I don’t consider bonds or annuities to be good income choices for most investors. When I say retirement income, you should be thinking “dividend growth stocks” and “dividend growth ETFs.”

Conclusion

The fourth reason I like bear markets, especially if they last through the end of a calendar year, is that it provides me with more options and opportunities for creating more tax-free income in the future. I also like bear markets because I am not driven to make decisions based on the emotions of other investors. Their decisions, in an unintended way, are helping me! But the fun won’t last!

Let me repeat what I said earlier: I love the current bear because I don’t have to make any income, investing, or giving decisions based on sentiment. Furthermore, the bear market sets me up for some great ROTH conversions! This gives us more tax-free income in the future.