Reason Number Three for Loving the Bear Market

Thus far I have talked about the benefits of buying more shares (or using the farming analogy, acres) during an economic or stock market downturn. When good assets are less expensive, it is the right time to “stock up.” If you have a dividend-growth strategy, then you are growing your dividends even faster using this approach.

The second reason to love bear markets is that a bear market usually has a limited life expectancy. So while there is some pain and “fear” during the downturn, it is often short-lived. Investors have relatively short memories. They left the market because of fear, but they come rushing back into the market when “greed” overcomes their fears. Don’t wait for the greed cycle. You don’t really know when it will come.

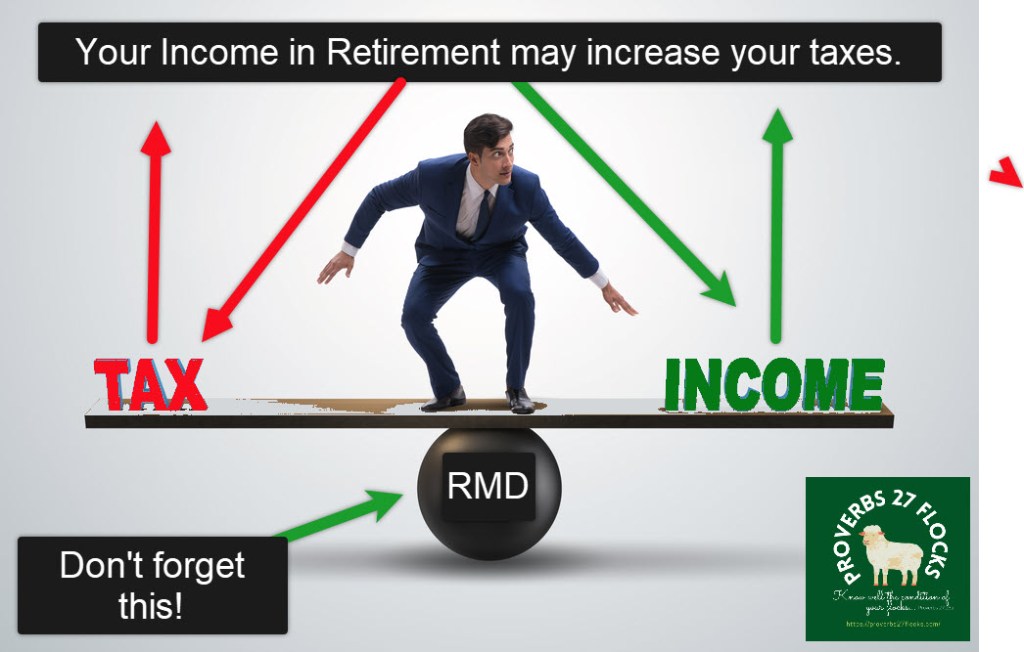

Required Minimum Distribution and the Bear

However, there is another reason, “I want to give the bear market a hug!” It has to do with “RMD’s.” I want the bear market to endure until at least January 1, 2023. If it goes up a bit between now and then, that will be sad, but it may still work to my advantage. The reason is three letters: RMD.

If my traditional IRA account balance is battered by the bear through the end of the year, I will have a 2023 RMD that is lower as a result. This gives me more opportunities to do IRA-to-ROTH conversions during times when the bear market is still active. As it stands today, incoming dividends will more than cover my 2023 RMD, even if the bull market returns. That means I don’t have to sell any positions during a bear market to get cash for the RMD.

You should develop a retirement strategy that keeps this in mind. If you are a “growth” investor, you can feel the pain when you have to sell investments to cover the RMD, especially if the bear market is in control when you retire.

Bear Markets at Year End and the RMD

An RMD is a “Required Minimum Distribution.” RMD’s are mandated by law for traditional IRA accounts and traditional 401(k) accounts. Most of my readers are not at RMD age. Therefore, you are probably thinking, “I can stop reading this post.” Before you do, be certain that you understand a painful aspect of the RMD. The income taxes will probably come to haunt you sometime in the future. So a bit of forward thinking and planning can help you prepare for what is coming.

For example, if you have a traditional IRA worth $1,000,000 when you retire, your first withdrawal must be added to your income taxes. If you also have income from a part-time job, from Social Security and/or income from a spouse who has not retired, you need to add up the income to find your total taxable income. Remember, the withdrawals from a traditional IRA or 401(k) are taxed as regular income. There is no escape from paying taxes. So your $1,000,000 is not $1,000,000 of spendable money. You probably will have to subtract federal and perhaps even state income taxes.

The IRS says, “You cannot keep retirement funds in your account indefinitely. You generally have to start taking withdrawals from your IRA, SIMPLE IRA, SEP IRA, or retirement plan account when you reach age 70½. However, changes were made by the Setting Every Community Up for Retirement Enhancement (SECURE) Act which was part of the Further Consolidated Appropriations Act, 2020, signed by the President on December 20, 2019. Due to changes made by the SECURE Act, if your 70th birthday is July 1, 2019, or later, you do not have to take withdrawals until you reach age 72. Roth IRAs do not require withdrawals until after the death of the owner.” LINK

The Consequence for Failing to take RMDs

If you do not take any distributions, or if the distributions are not large enough, you may have to pay a 50% excise tax on the amount not distributed as required.

Some Actionable Steps for Those Younger than 72

Some of your possible actions may depend on your current income.

- Try to deposit more of your income, if possible, into a ROTH 401(k) or into a ROTH IRA when the market is in bear territory so that you can buy more assets at a lower price. There are no RMD’s for these accounts. If you save in ROTH accounts, you avoid taxation later by paying taxes now. There is another ROTH strategy that I will discuss in my next post. It is another reason I like the bear market.

- As you approach retirement, ask yourself, “Do my current investments provide sufficient cash so that I can take my RMD without selling any of my stocks, ETFs, or mutual funds?” A dividend growth strategy can help you avoid the pain that can come when a bear market appears at just the wrong time. Do you have a good strategy?

Conclusion

The third reason I like bear markets, especially if they last through the end of a calendar year, is that it provides me with more options and opportunities for reducing my income taxes. You can do the same with a long-term plan. This makes other actions more attractive, including one I will discuss in my next “why I love bear markets” post.

RMD Comparison Chart (IRAs vs. Defined Contribution Plans) – IRS LINK