Do Your Current Investments Prepare You For Retirement Income?

Many investment portfolios contain two components I see as fundamentally less than ideal for both growing your investments and for income potential. The two components are an over-reliance on bonds and bond ETFs, followed by the exact opposite: an overly aggressive set of growth stocks and ETFs. While I am certainly not opposed to holding growth stocks, and I buy and hold some growth investments, there is a better way to grow wealth and then have a ready-made income stream for retirement. Far too many investors, I believe, focus on growth, and then have to transition to income. I prefer to focus on growth and income.

Bonds as a Retirement Income Source

Bonds provide income. The question you should ask yourself is, “Does the protection and comfort provided by bonds really protect me?” Is it worth the higher risks that come with owning bond mutual funds and ETFs?

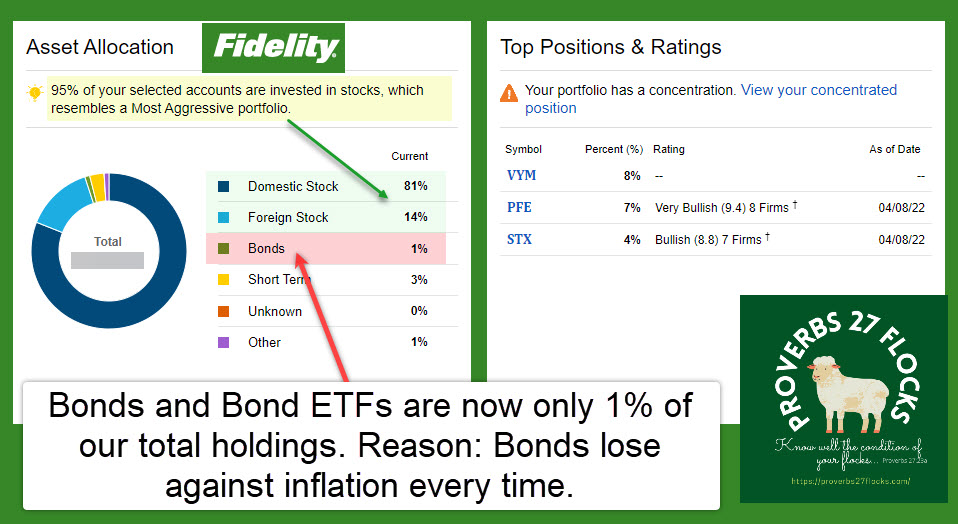

I have decreased our bond ETF holdings. Most of the ETFs have already been sold. The only one that remains is VCLT (Vanguard Long Term Corporate Bond ETF). However, I sold covered call options on all of our shares, and it looks like they may not be called away. If they are called away, our total bond holdings will fall below 1% of our total holdings. I still have one municipal bond in my brokerage account, but it is tax free for our Federal income tax return. Bonds are not a great investment, and they offer very little protection when interest rates and inflation are rising. If your bond or bond ETF isn’t paying 8% or more, your dollars are losing their purchasing power. That is because the annual inflation rate in the US increased to 8.5% in March 2022.

The annual inflation rate in March is the highest since December of 1981 from 7.9% in February and compared with market forecasts of 8.4%. Energy prices increased 32%. Also, food prices jumped 8.8%, the most since May 1981. The CPI rose 6.5%, the most in 40 years but slightly below forecasts of 6.6%. Source: U.S. Bureau of Labor Statistics

Growth Stocks as a Retirement Income Source

Growth stocks are only growth stocks when the market is going up. When the market is going down, many, if not most, growth stocks suffer. They tend to suffer more than value stocks that pay a dividend. Let’s assume you have 100 shares of Google stock. If you are retired, the only way to get cash from most growth stocks, including GOOG, is to sell them. It is true that some growth stocks pay a dividend. The problem is that those that do usually have a very poor yield.

So, for example, Google (GOOG) does not pay a dividend. In the last five years GOOG is up over 200%. That is wonderful! But the growth in the value of the shares cannot pay the bills in retirement. Year-to-date GOOG is down a bit more than 10%. If you need $5,000 per month in income today, and you don’t have other sources of income this month, you will have to sell two of your Google shares to raise the cash. Unfortunately, this would be the wrong time to sell shares. I’m not suggesting a retiree should avoid growth investments. However, understand the risks of doing so. Bear markets can make a retiree’s life very difficult.

Dividend Stocks as a Retirement Income Source

There are growth stocks that pay a dividend, but value stocks tend to pay a higher percentage. It isn’t uncommon to be able to get 2.0% or greater on many value dividend stocks. McDonald’s (MCD) for example, is not likely to grow as fast as Google. In the last five years MCD’s stock has only grown about 92%. That is less than half of Google’s growth. However, MCD’s stock has only declined a little over 6% YTD. Why is this? Because investors who own MCD know they will be receiving a dividend that currently yields about 2.2%. McDonald’s shareholders don’t have to sell their shares to get the dividend. Not only will they receive about $5.50 per share in dividends in 2022, but it is also highly likely that MCD will increase the dividend in November every year. In the end, you give up some growth, but you still get growth plus income. The biggest plus is that you don’t have to sell your shares to receive income. Before you retire, you can reinvest the dividends, and this has a snowball effect in growing your income base.

Dividend Growth Stocks and ETFs as a Retirement Income Source

There are many great companies that pay an increasing dividend every year. The easiest way to participate in this dividend growth, with a decent yield, is to buy ETFs that focus on the stocks of companies that have a history of growing dividends. That is why VYM is the largest holding in our accounts at Fidelity.

If you want to invest in individual company stocks, TXN (Texas Instruments Incorporated) is an example of one technology stock that is attractive. TXN has shown dividend growth for the last sixteen years. The current yield is 2.68%. Each shareholder can expect to receive about $4.60 per share in dividends. But even more importantly, TXN has a five-year dividend growth rate of 19.78%. Think of that number in relation to inflation. It more than covers the current inflationary climb. Another good example is AVGO (Broadcom Inc.) The yield is 2.82%, the payout ratio is a very comfortable 38.24%, and the five-year dividend growth rate is 38.24%. AVGO has increased their dividend for the last eleven years.

Options Trading for Retirement Income

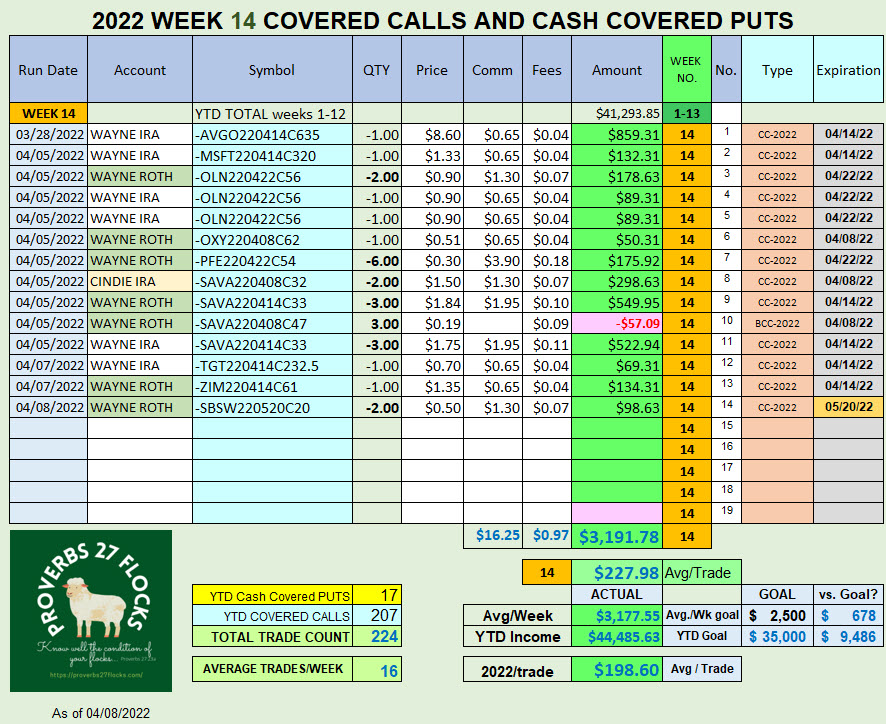

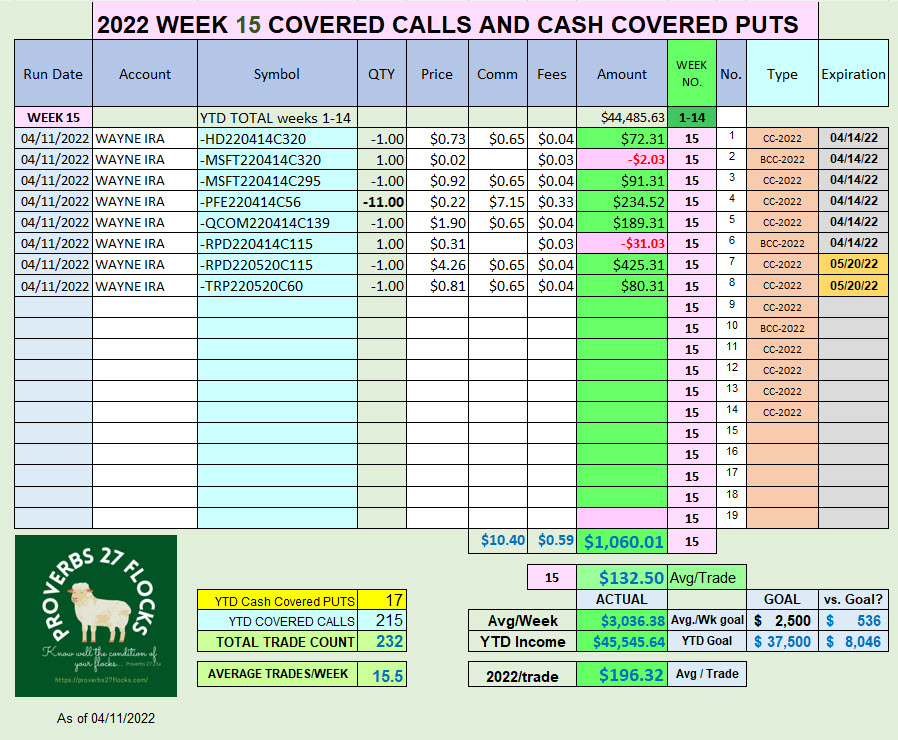

Finally, it is relatively easy to learn how to trade options. I do it every week. It only takes about four hours to make $2,500 in the average 40-hour week. So I make around $625 per hour without much work. This includes covered calls, cash covered puts, and some option rolls. The only problem with this approach is that you have to be willing to learn how to do it. You also need to own a minimum of 100 shares of the stock you want to use for options trading. Furthermore, ETFs, in general, are not a good source of options income. I have found that selling covered calls on growth stocks can be a great way to get pseudo-dividends from a company that doesn’t pay a dividend. For example, I have been growing my holdings of Amazon stock (AMZN) with the intention of trading covered calls on my holdings.

This is a significant income opportunity. Last year our total income from options trading was $90,631. YTD 2022 (in just a little over three months) we have had $45,545 in additional income. Bear in mind that this tactic is not necessary for retirement income success. In the first three months of 2022 our dividend income of about $35,000 by itself is more than sufficient to cover giving and discretionary spending.

Putting It All Together

Think about your income needs in retirement. Can you forecast a date when you have eliminated your mortgage payments? Using a minimum of 3% annual inflation, adjust your anticipated cash flow needs based on your current budget.

For example, if your budget (without mortgage payments) is currently $60,000 in 2022, and you plan to retire in 2032, you will have a real budget of $78,000 based on 3% inflation. Let’s assume you will receive $24,000 per year in Social Security benefits. That would mean your total assets in your retirement accounts would have to be about $1.4 million and you would need a dividend yield of about 4.0% to make up the $54,000 shortfall. I realize this is very simplistic. There are other factors like your health, your children’s needs, and the number of years you can work that can complicate the analysis. I’m only trying to encourage you to think long-term as you evaluate investment options and opportunities.

Then, after you have approximated your needs in retirement, start learning to invest in a way that gets you started on that path so that you don’t have to make dramatic investing changes when it comes time to retire. Include growth stocks in your portfolio but be thoughtful about how much you devote to that segment of the overall market. This becomes even more important during the five years leading up to your anticipated retirement date.

Very nice article. I sure do like your investment approach. You are going to get me into options yet…

LikeLiked by 1 person

Terry, you probably don’t need to do options trading. I think you would be better served to just focus on dividend growth investments. However, if you ever want a 15-30 minute overview during the trading day, I can show you how I evaluate a covered call trade using Zoom. You will be able to see my desktop and see how I evaluate a trade and how I enter it in Fidelity’s Active Trade Pro. That is the easiest tool for me to use and to illustrate how to do the trade. However, I doubt that you will need to do options trades to have success. 🙂

LikeLike

Interesting approach, although I’m not in retirement years yet but I’m learning to invest and make addition income by trading. Is your excel for ledger tracking sharable? I have my own version where I keep CCC and CSP separate, but I noticed you have one sheet for both trades!

LikeLiked by 1 person

The spreadsheet image that I share on the Fidelity Investor Community is just for the purpose of sharing highlevel details on my blog and on the community page. I have a different spreadsheet for the actual options work that I do. I can share as sample. I will send it to you via email.

LikeLike

Thank you very much

LikeLike