An Alternative to an Annuity

This is the fifth is a series of four posts about annuities. Yes, I did say fifth of the four. I originally thought four different discussions were sufficient. However, I read something an investor said in the Fidelity Investor Community and it triggered this fifth annuity post. The investor’s handle is “stillworking” – but only in the Fidelity community.

He was talking about the concept of bucket investing, which is a strategy to make it possible to have income and some cash available so that investments don’t have to be sold during market corrections or downturns during retirement. This is also what I do.

Dependable Income in a Self-Paying Annuity

Stillworking considered an annuity. But the structure of annuities did not appeal to him. This was one of the things he said: “Annuities also did not offer enough especially if sacrificing my principal. So I created in essence, my own annuity in which I create fairly steady income, and since these are from my own holdings, I called it Self Paying Annuity, which is to remind me to focus on the dependability of the income stream vs market price.

What Does It Look Like for Stillworking?

He went on to say this about his strategy: “It is rather extensive, with equity holding of stocks with long histories of paying dividends and increasing, some other criteria on current yield and growth of dividends.”

He then also mentioned individual preferred stocks, a few open-ended bond funds, and several closed ended funds (CEF) for debt, utilities, preferred, equities and some others. He continued, “Many who delve in closed ended funds trade them quite a bit, market prices volatile, but while I may time increasing purchases in one or the other, I hold and collect those distributions, all of the above are monthly distributions.” This is probably more complicated than I would suggest for most investors. But there is a way to mimic an annuity.

Building a Self-Paying Annuity

The goal is to build a portfolio that gives you growing, sustainable, dividend income paying you monthly and quarterly. This can easily be using ETFs and individual stocks. For example, if the insurance company is promising a 3% return on the annuity, even with some growth in the overall account balance, I’m convinced that most of my readers would do much better with the following components.

- Buy ETFs that have a history of growing their dividend payout. They can do this because that is the strategy of the ETF. Some ETFs that I hold that pay quarterly dividends are VYM, DGRO, and SCHD. Other options include HDV and DVY.

- Buy stocks that pay a monthly dividend. Oftentimes this will include financial companies like BDCs (Business Development Companies). My favorites include MAIN and GAIN. ARCC pays a quarterly dividend.

- Buy real estate investments known as REITs. Two that pay a monthly dividend, that we own are O and ADC. There are, of course, other good REITs that pay quarterly.

- Buy individual stocks that pay a quarterly dividend. Pick one from each sector and look for rising dividends with at least ten years of history of increasing dividends. For example, IBM has been increasing their dividend for 22 years. Microsoft (MSFT) has been increasing their dividend for 18 years. These companies are known as “Dividend Aristocrats.”

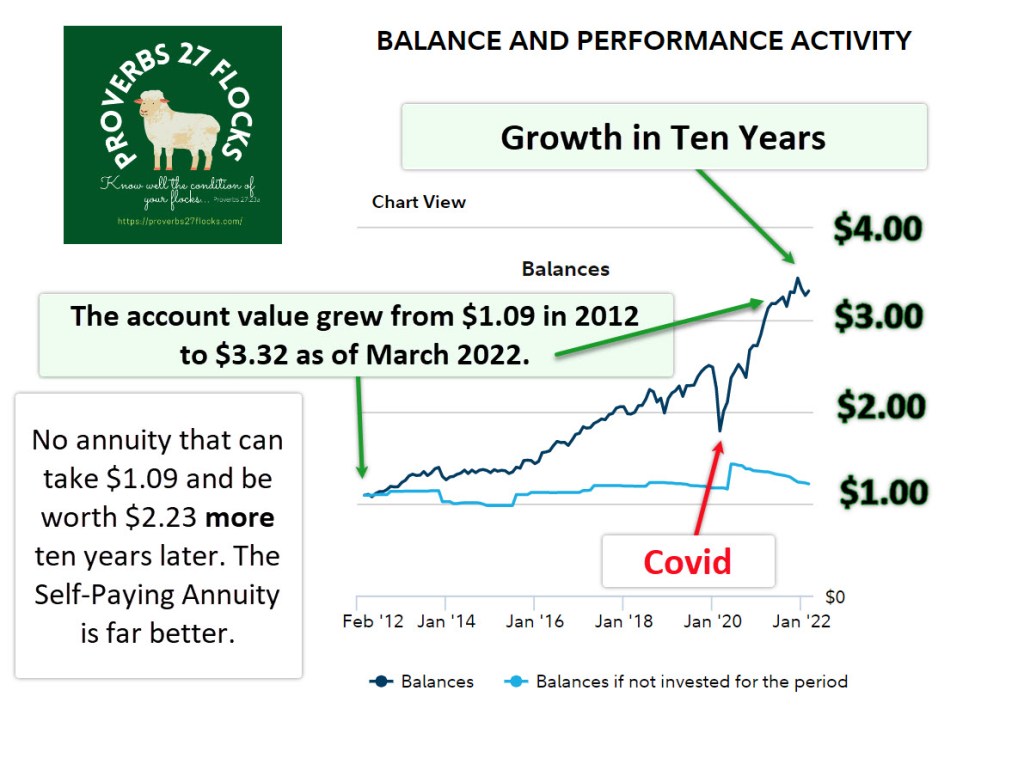

If you take this approach, it is fairly easy to see what your dividends will look like. This knowledge will keep you from being overwhelmed when the market drops. In fact, here are the last ten years of growth on our retirement accounts. At age 61, when the prevalent logic is to be 60% stocks and 40% bonds, I stayed invested. When I was 69 and Covid-19 struck dividends kept pouring into our accounts.

There is no annuity that could turn $1.09 deposited in 2012 into $3.32 today. For example, if you give an insurance company $109,000 for an annuity that pays 3.0%, you might reasonably expect to receive $3,270 per year. However, your account will not be worth $332,000. Think about that before you buy an annuity if you think it is possible you might live ten more years.

Dividend Growth Can Be Exponential

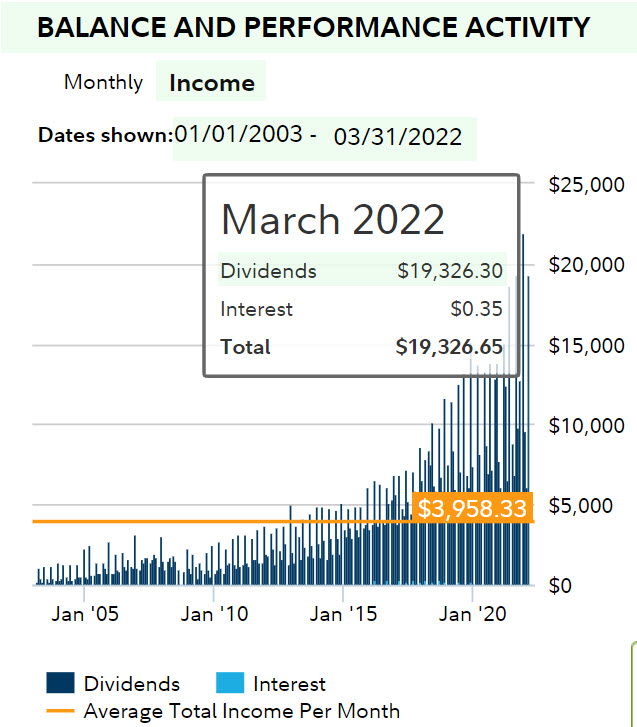

The number on the following graphs shows the average monthly dividend almost twenty years. It is $3,958 per month. Of course, our total balances are more than $109,000.

But you should notice that dividends, from dividend growth investments, have continued to grow exponentially. Our current average monthly dividend income is about $10,000. We don’t need that much, but it keeps me from selling investments during market volatility or downturns. Do you see a downturn in dividends during Covid? You should not see it because it did not happen.

You can have a nice slice of income from your investments and still keep your investments. I like having my pie and eating it too.

Very compelling Wayne. The graphs give great perspective with this strategy

LikeLiked by 2 people

Thanks for the feedback. I know sometimes things “sound good in theory” but I always like to see how the theory works with some history. 🙂

LikeLiked by 2 people

I am finally seeing the light. I am going to begin the process of the unwinding of bonds from my portfolios which percentage has already gone from 45% to about 30%.

LikeLiked by 2 people

I have also reduced my bond ETF holdings. I was at 3% and am now down to 1%.

LikeLiked by 1 person