The Wrong Place to Start is Being “Sold”

This is the fourth and final post in a four-part series about annuities. In the first installment I explained that an annuity is a life insurance product that can pay you while you are living and even provide an inheritance for your heirs. In the second I gave the advantages some might see in buying an annuity contract. In edition three I gave you some food for thought about the disadvantages. If you need an annuity, then the process you use matters. Do not start by going to a broker, financial advisor, or insurance salesperson to buy one. That is the last step. If I were going to tell my mom what she should do, it would look something like the following.

Determine the Need

Step One: Do you have a budget? The very first question I ask people who come to me for help is, “do you have a budget?” If they don’t, or if they say something like, “I don’t like budgeting and I don’t think I need one,” then I think they don’t really know if they have a need or not. A budget doesn’t have to be complicated or take a lot of time. A budget simply is a picture of the income you receive and the money you are spending. Sometimes I help people who really need a budget because they are spending more than they make. Oftentimes they are spending more than they need to spend. Here is the bottom line, if your normal cost of living is $3,000 per month, and your income is $4,000 per month, then you should press the annuity pause button.

Step Two: Evaluate your income sources. If you are nearing retirement and have 401(k)’s scattered across three different former employers and a 403(b), and a ROTH IRA, and a savings account, you have the fuel for income. In our case, because I developed a plan and a strategy, our income from my Social Security easily covers all of the basic living expenses. Cindie also has a nice stream of income from her part-time baking job. Even if she did not, she could start to take Social Security in September which would be more than her current income from baking.

But that is only a portion of the income flow. Because most of our investments are dividend-growth stocks and dividend-growth ETFs, we receive an average of 4.5% on our total assets. On top of that, I sell covered-call options. That also provides a bit more than $2,500 per week (YTD) in additional income this year. At this point in the process, I can stop. We don’t need an annuity. If you have assets, are your assets working for you? Are you receiving at least 3.0% in dividends from your total accumulated wealth?

Step Three: Evaluate the Gap and Your Age. The third piece is to then look at the results of steps 1 and 2 and ask, “Do we have a problem?” If the answer is that your spending is greater than your income, and you aren’t able to make your retirement savings pay you enough to cover your costs, the next logical step is to work longer before retirement. Working is not a bad thing. In fact, I still work every day, but I work for “free” to help others. Sometimes I help Cindie with her garden, sometimes I teach a series of lessons to pastors in India, and sometimes I help friends and grandchildren with investing. However, if I had to work, even though I am 71 years old, I could still work.

When I say “evaluate your age” I am saying that you should not be rushing to solve a retirement cash flow problem when you are 18-65 years old. So, let me suggest that you act your age and work. Even in semi-retirement I took some part-time jobs at Target and The Home Depot to earn some extra cash, but mostly to get some exercise!

Step Four: Start to Learn About Annuities. Let’s say you have done your homework and you are 65 years old (or older) and you (or a loved one) have a need for dependable income. Annuities are a complicated beast. It is now time to start talking to some people about the annuities they offer, using the questions and concerns I raised in the previous three posts. Don’t buy the first policy that is offered. Ask questions. If the answers are hard to understand, then find a different provider. You should expect simple English answers to your questions. Furthermore, it is fair and wise to ask, “What other possible annuity solutions do you offer?”

It would be most helpful for you to go into these learning sessions with a list of questions and with a monthly income number in mind. So, for example, if you would like to receive $1,000 per month in income from the annuity, starting when you turn 66 years old, tell the provider that this is your need and expectation. Do not, under any circumstances, get talked into something that provides $3,000 per month if you only need $1,000 month.

Why is this important? The more income you need drives the amount of cash you will need to give the insurance company. You should strive to be a wise consumer and buy what you need, not what the insurance company wants you to want.

Compare the Solutions

I rarely buy expensive things without first getting a comparison of the choices on paper. So, for example, if I were going to set up a 100-gallon saltwater aquarium, I would certainly want quality components. Saltwater fish are expensive. Therefore, I would talk to more than one provider and get recommendations for a complete solution. I can then compare both the costs and benefits of each solution.

You should do the same with insurance products, including annuities. Don’t rush this decision. Once you make it, unraveling it is a very expensive activity.

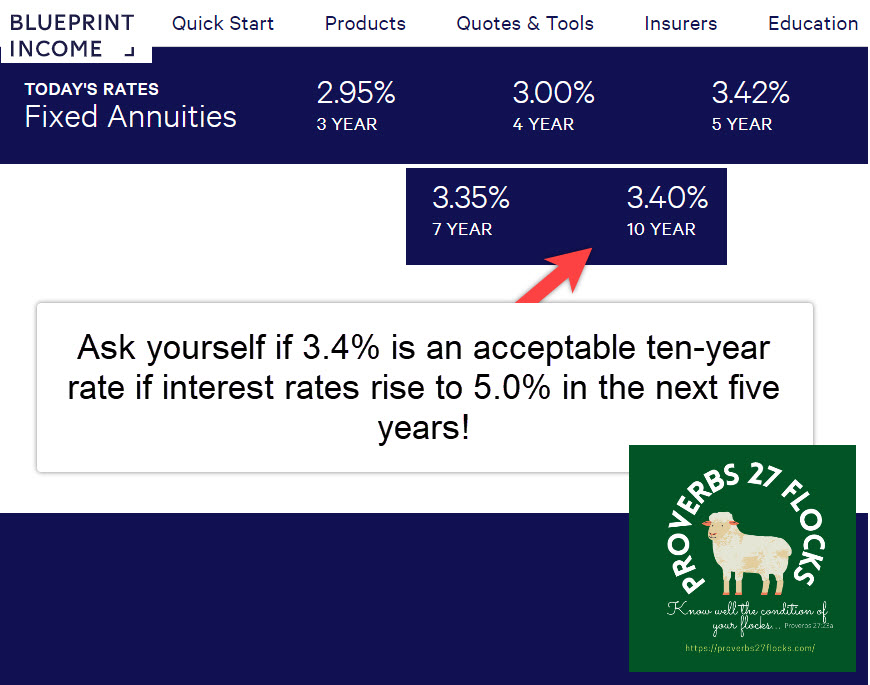

Use a Blueprint Tool

When someone builds a home, they need to have a building plan. In the dark ages, when my dad was working for a builder, he created drawings of the proposed home, and these were printed as blueprints. The blueprints made it possible to determine the materials needed and the types of workers who would be involved in the construction of the home. One good annuity blueprint resource is called Blueprint Income.

Blueprint income is a “one-stop shop.” “Blueprint Income works with more than 30 of the world’s top insurance companies to create the most competitive marketplace of good, simple annuities out there.” There is a quick start guide and you can see the insurance companies that are selling their products. In other words, it is a wonderful resource for comparison shopping.

Summary

I still believe you will find most annuities are costly and complicated solution. They are hard for the average person to understand, and they are sold using graphs that make them appear to be a wonderful solution. If nothing else, enter the world of annuities with a dose of skepticism and a lot of questions. Expect answers in plain English. Just like with other investments, if you don’t understand it, don’t buy it.

My financial adviser found an annuity with quarterly step-ups that would never go down about 8 years ago. I just wanted a small chunk of money to pay for one time expenses for the year in retirement…It is building and paying real estate taxes (even though they went up 30% this coming year because of valuation). Hind-sight I could have done better knowing what I know now but at the time it seemed good. The company quickly put that product out to pasture as they realized they wouldn’t make enough money with step ups like that.

LikeLiked by 1 person

Gary, Every person’s need is different. I am always learning new things and that is why I try not to bash an investment that I don’t like. Sometimes there are good solutions suited for some individuals. Thanks for the comment!

LikeLiked by 1 person