Planning for Growth

Most individuals and families know a rough estimate of their total annual income. If you are employed, on commission or own your own business, it may be difficult to know what your total income might be halfway through a year. It is probably also difficult to know what your income might be next year. When or if you retire, you can also get a reasonable estimate of your Social Security income and/or any pension income you might receive. That income, however, probably won’t increase in a meaningful way.

I knew that my Social Security would be about $2,000 per month, based on the year that I started drawing this government-provided income. I also knew that the inflation numbers the government uses to increase Social Security would not work to our advantage. I was right. In the seven-or-so years that I have been receiving Social Security, our income from that source has not kept up with inflation. I planned accordingly. I cannot depend on Social Security to cover our housing, food, healthcare, and other basic living expenses. In fact, our property taxes are over $7,000 per year in Fitchburg, so that eats away at the Social Security income at about $600 per month.

The Dividend Growth Train

It is reasonably easy to predict your income from investments if you know the total investments dollars in your IRA, Roth IRA and/or brokerage and savings accounts. If you have a million dollars, and you think you can earn 4% from this total (interest and dividends), then you can probably expect to receive $40,000 per year from your investment portfolio. What if, however, you could select investments that not only grow in value, but that also provide annual increases in your income? You can. That is the approach I take when selecting investments. I want many of our investments to be dividend growth engines.

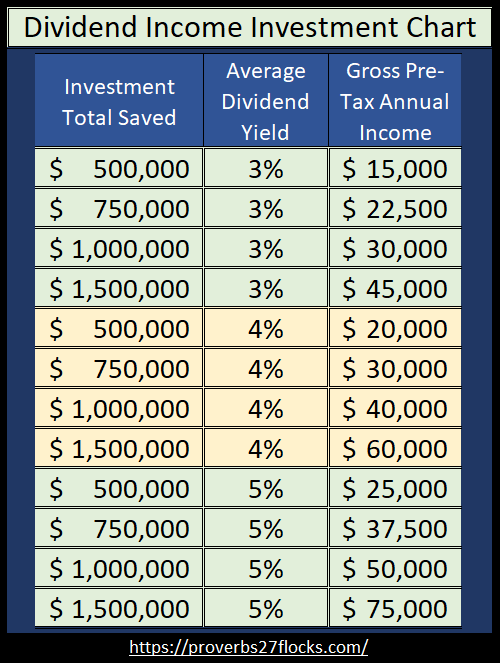

Hypothetical Income

This chart gives you a rough idea of the power of your investment portfolio, assuming either a 3%, 4% or 5% rate of return. I have found that an overall rate of return of 2.5% is easy to obtain. Because I am willing to invest in REITs and BDCs, and they pay substantial dividends, it is also easy to achieve 4.5% or more. For planning purposes, it might be best to think you can achieve 3%.

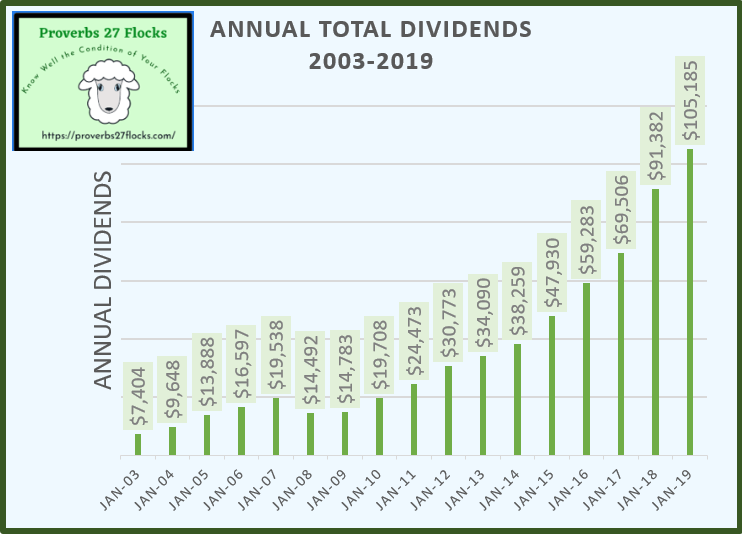

Our Results for 2003-2019

As you can see, our dividend growth in dollars has been good every year except one. The year of the decline was when I realized that my strategy was wrong, so I started selling some investments and began looking for investments that met my new strategy and goal. After fine-tuning our investment mix to include some ETFs like VYM, SCHD, and DGRO, the engine produced better than expected results.

The Same Data as Percentages

What is even more amazing are the results when expressed as percentage changes year-to-year. These numbers almost appear to be irrational.

However, bear in mind that little income has been drawn from our IRA’s and ROTH IRA’s in the last seventeen years. Therefore, the dividends were either reinvested automatically, or dividend income was used to purchase more dividend-paying investments. Because I have been receiving Social Security, the dollars needed for our lifestyle during retirement were reduced. This freed up investment dollars to fuel the dividend growth engine.

A Slice of 2020

COVID-19 hit some investments dramatically. Some of our investments in energy have been hammered. However, those investments have not only continued to pay the quarterly dividend, the investments have also increased the dividend payout. Of course, it is possible that some investments do reduce their dividend. When they did, I sold them (with a few exceptions.)

This chart shows just a small part of the investments in our portfolio that declared a dividend increase in the first one and a half months of 2020. Some of them, like LNT, VLO, MPC, ANTM, GLW, MFC (Canada), and NEE have increased dividends by at least 7.0%. This is not unusual, and this is why I like the dividend growth model. When you are still working, you can buy more shares if you have growing dividends. Don’t miss that opportunity!

RMD’s – Required Minimum Distributions

One final thought. When you reach age 72, based on the current law, you have to start taking distributions from traditional IRA’s or 401(k)’s. You can plan for that as well.

In our case, Cindie and I have ROTH IRA’s, so no RMD’s are required for those accounts. However, I also have a traditional rollover IRA. I structured the investments in that account so that the dividend income will cover the RMD. That way I don’t have to sell any investments in a panic or during a market panic to cover the amount I will be required to withdraw. Don’t miss that part of the equation either.