Understand Strategy Because It Should Drive Behavior

At Conney Safety Products, we often talked about strategy. We had a strategy for Information Technology eCommerce, for who we were to be for our customers, for the types of customers we would serve, for the products we would sell or not sell, and for our financial results. When I was in the military, serving on the U.S.S. Bagley, we had a strategy (delegated from higher ranking leadership) of protecting other vessels and destroying submarines. Our drills and exercises focused on executing to the strategy. Even in my investing life, I start with a strategy. That strategy is worked out by creating rules for my choices and how I will respond to dangers and setbacks.

Winquist Investment Portfolio Strategy

My investment strategy is quite simple. It is related to cost avoidance, to preservation and gradual growth of our assets, and growing income. I don’t want to get hammered by expenses, inflation or income taxes. I don’t desire or need massive growth in our retirement years. I prefer to see our income increase annually so as to avoid selling any investments because “I have to in order to pay for the necessities of life.” These strategic choices cause me to limit my exposure to high-cost mutual funds and similarly high-cost ETFs. I try to make withdrawals in a tax-efficient manner. I don’t buy investments that cannot hope to keep pace with inflation. I buy investments that are likely to at least maintain, but also grow our annual income. Therefore, I generally invest in dividend growth ETF’s (VYM, SCHD, DGRO, DVY) and dividend growth stocks or dividend champions.

Sometimes the best way to see the way a strategy plays out is through images. In the next seven images you will see elements of my strategy and why each element is important. The elements are 1) What to do when investors are in retreat; 2) Where in the world I will invest; 3) My concentration of investments and diversification goals; 4) My asset allocation (stocks, bonds, cash); 5) My thinking about the sectors and sector diversification; 6) My choice to prefer value stocks versus growth stocks, and 7) Why I don’t care what the rest of the total market is doing.

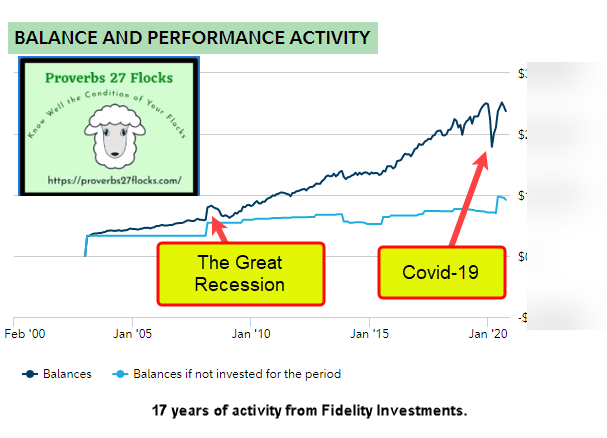

What to do when investors are in retreat.

There have been two major retreats in the last twenty years. I ignore the retreats, with a few minor exceptions that are written in my buy/sell rules. An exception is if a company cuts or suspends their dividend, I consider selling. In the most recent Covid-19 downturn, I eliminated several positions related to hotels, hospitality, and entertainment. Those that go to cash are my friends. I can often buy their shares at discounts to the real value.

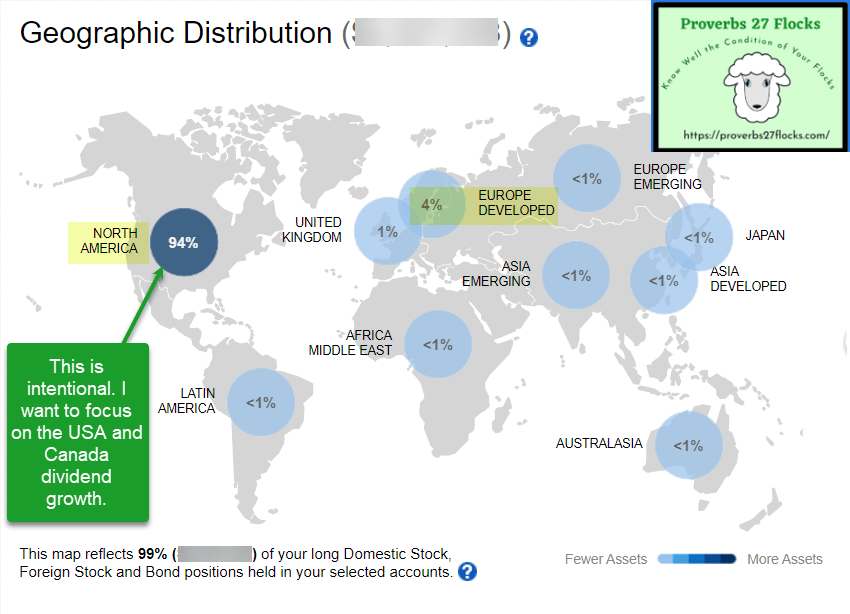

Where in the world I invest.

Many advisors recommend a more robust allocation to international companies. While I see value in some countries, there are others with serious governance and free enterprise issues. As a result, most of our investments are in the USA and Canada. Of course, many USA companies have business overseas, so my allocation isn’t exactly as this image would suggest. However, it is probably safe to conclude that our international investments don’t make up more than 10% of our total stock investments. Fidelity seems to think that I have 9% in foreign investments, but that includes some significant allocation to banks and telecom stocks in Canada.

The concentration of investments and diversification goals.

If any single stock is 5% of our total investment mix across all seven major accounts, I seek to lighten up. Our biggest holding is an ETF: VYM. That reduces concentration and VYM contributes nicely to our dividend growth focus.

The asset allocation model (stocks, bonds, cash).

As I have said many times before, I think too many investors, especially younger ones (55 and younger) have way too much money in cash and bonds. I wish I could convince them that they have greater risks from that approach than they do with a more “aggressive” stock investment approach. Sadly, far too many investors think that volatility is risk. It is risk only if you don’t have enough money to live on. If you have enough income from your job, Social Security and from income-producing investments, then I think anything more than 10% cash and bonds is a way to lose opportunities.

Which sectors and general sector diversification.

This is another area where I beg to differ with many experts. I have no desire of creating an investment portfolio that mirrors the total stock market, the NASDAQ, the Dow Jones Industrial Average (DJIA), or the S&P 500. Furthermore, I don’t see a need to keep my sector allocations in line with what the “market” is doing. Therefore, as you can see, I have more than the “normal” amounts invested as a percentage in financials, utilities, and real estate. I’m want performance, and I don’t care about the origin or nature of the investment based on sector. Now, it is true that political and economic changes can cause me to reevaluate a sector. For example, I still like energy stocks, but I am not looking to add more of them given the recent oil glut caused by government shutdowns of our economy.

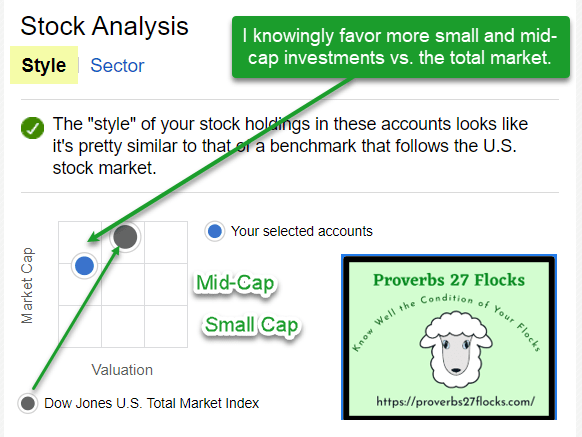

Preferences regarding value stocks versus growth stocks.

By their very nature, dividend growth investments usually aren’t growth stocks in the strictest sense of the word. Many, if not most growth companies do not pay a dividend. That doesn’t mean I don’t buy stocks unless they pay a dividend. For example, I own shares of companies like RKT. Most companies transition from growth to value over time. I also have some utility stocks that have proven they are growth stocks.

Why I don’t care what the rest of the broad market is doing.

By definition, a strategy isn’t concerned about what “everyone else is doing.” It isn’t in trying to conform to a set of requirements. Therefore, while many investors are seeking, and may need growth, that isn’t my goal. The goal of growth can be accomplished by leveraging dividends with wise additions to existing positions or adding new positions at opportune times.

One of the benefits of my approach is that Cindie won’t have to do anything to keep getting growing income if I am no longer able to do this work for her. My approach is essentially “set it and forget it.”

Summary

If you have not done a similar analysis of your investments, let me encourage you to do so. If you have your accounts at Fidelity investments, this is easy to do. All of the screen shots shown in this post were captured from Fidelity’s Analysis tool.