Minimizing Income Taxes

It is right to pay the amount you owe in taxes. But it is also wise to work to minimize the income taxes you pay. For most of the younger generation the ROTH IRA and ROTH 401(k) helps reduce the future ultimate tax burden when retirement income can be tax-free. For those who started working and saving decades ago, the traditional IRA allowed for growing a crop of retirement assets by saving on income taxes. Unfortunately, that only delays the inevitable tax bill and that drain can cause a sucking sound for your spendable income. There are, however, ways to reduce the tax.

The IRA RMD is Required and Costly

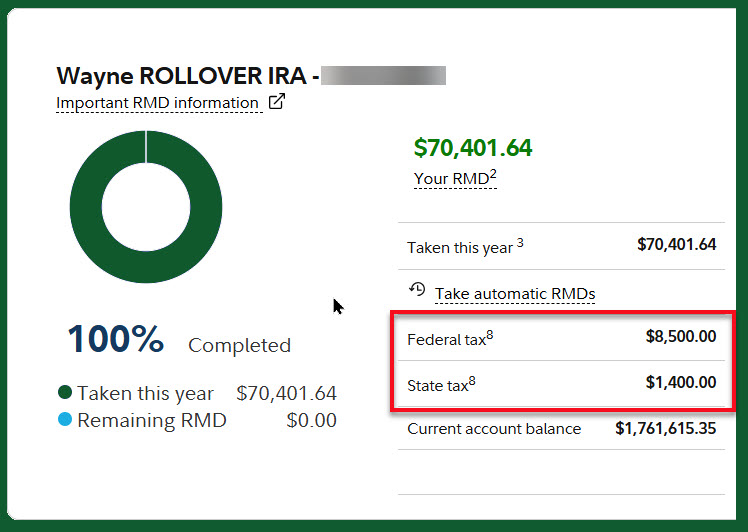

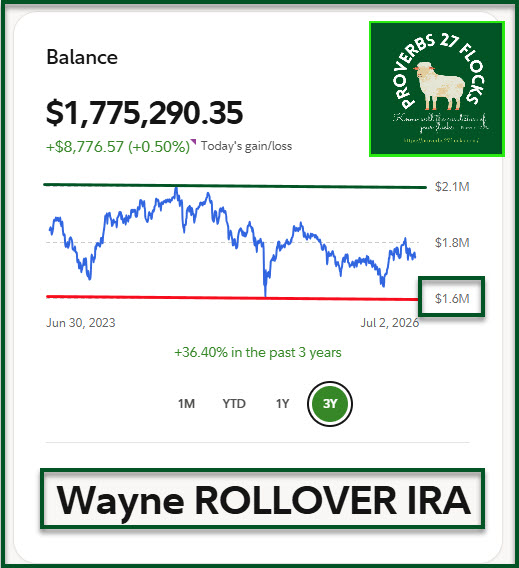

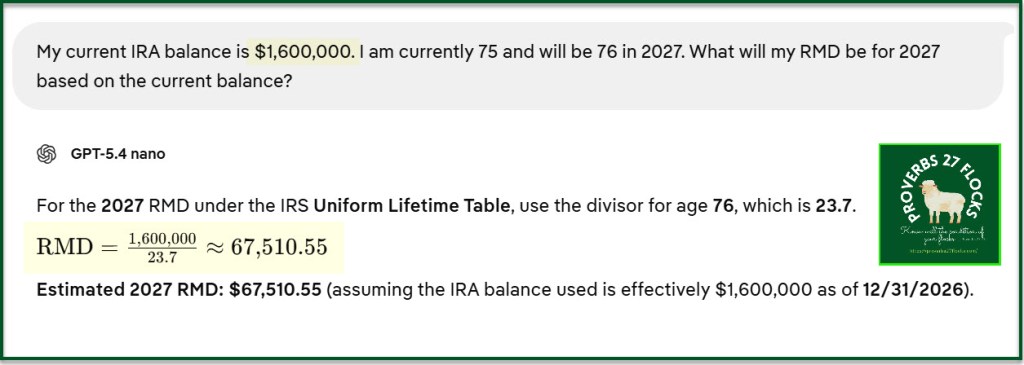

A Required Minimum Distribution (RMD) is the minimum amount that you must withdraw from your retirement accounts, such as IRAs and 401(k)s, once you reach age 73. These withdrawals are mandated by the IRS to ensure that retirement funds are eventually taxed. Because your account balance will (SHOULD) increase each year, if you invest wisely, the tax will increase. That is because the RMD is calculated each year on the last day of the year.

However, that isn’t the worst of it. The percentage you have to withdraw each year also increases as you get older. The percentage at age 73 is the lowest you will ever face. By age 85 the tax obligation can be daunting.

By way of example, let’s assume you have $1,000,000 at the end of the year when you start taking RMDs. You will have to withdraw $37,735.85 as your RMD. That is 3.77% of the one million dollars. Therefore, you have to pay taxes on the RMD and those are dollars that you cannot use for living expenses.

Let’s assume your account grows to $2,000,000 by the time you are 85 years old. Now your RMD will be $125,000. This is 6.25% of the IRA account balance. Your tax bill will have increased significantly as a result.

Married or Single

If you are married, then the tax burden is considerably lighter. However, if the IRA account holder or their spouse dies, the tax bill immediately becomes significantly more. That is one reason that doing disciplined ROTH conversions makes sense from a long-term income tax perspective.

Two Helpful Strategies

Number One: Give Generously: If you believe in charitable giving, then a tax-efficient way to give during the last years of your life is to use QCD’s. For the tax year 2026, the maximum amount you can donate through a Qualified Charitable Distribution (QCD) is $111,000 per person. This allows individuals aged 70½ or older to make tax-free donations directly from their IRA to qualified charities.

The good news for 2026 is that I have successfully completed my RMD using QCD gifts. That means I can now begin careful ROTH conversions. I have a spreadsheet of my IRA positions that I will use to inform my conversion decisions. Not every position in my IRA is a candidate for the conversion process. I consider three factors: the current QUANT rating of the asset, the dividend’s being paid by the asset, and opportunities to trade options on the asset in my ROTH IRA. (Note: The taxes shown are for our total income, not just for the IRA QCD withdrawals. These taxes will cover the ROTH conversions I plan to do.)

Strategy Number Two: ROTH Conversions: You can keep the dollar amount of the RMD in check by moving assets from your traditional IRA to your ROTH IRA. Of course, you will pay income taxes on the dollar value of the conversions, but those taxes for many people will be worth the cost.

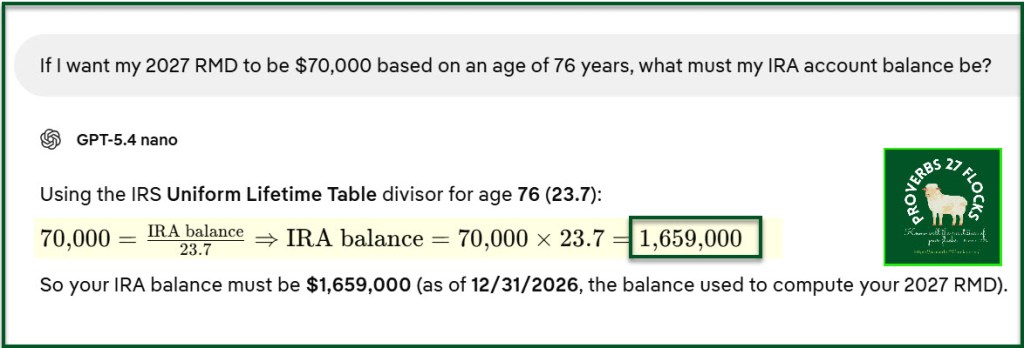

I plan to convert positions from my traditional IRA in such a way that the RMD will remain in the $70,000-$75,000 range. The lower the number, the better.

Conclusion and Suggestion

If you believe in giving, and if you are at least 70.5 years old (or if some day you are going to be that age) you may want to think about adding QCD to your alphabet soup of helpful abbreviations.

It doesn’t hurt to talk to your broker about this. Fidelity has some great options for QCDs. I ordered checks from Fidelity for my traditional IRA. I write checks to any charity that is willing to provide me with a letter acknowledging the QCD gift. Bear in mind, however, that the gifts given this way are NOT allowed as an additional SCHEDULE A deduction. That would be double-dipping. Therefore, a charity or church needs to separate regular giving from QCD giving on any statements they provide.

Seeking Alpha Subscription Renewal

I will be renewing my Seeking Alpha Subscription. On a per-year basis it is very helpful at a very low cost.

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com