A Good Tool for Educating Your Children and Grandchildren

Do you know what a good man or woman who is a grandparent does? King Solomon suggested one thing in Proverbs 13:22: “A good man (or woman) leaves an inheritance to his children’s children, but the sinner’s wealth is laid up for the righteous.” There are a couple of principles in this proverb, but if you think about it, the good parent or grandparent has a way of “leaving an inheritance” that is more than dollars. It is passing on knowledge, experience, wisdom, and skills.

One way that Cindie and I have attempted to do this is by giving our grandchildren gifts that enable them to learn about investing. Those gifts started in the form of UTMA accounts. Fidelity also introduced “Fidelity Youth Accounts.” When those became available, we helped our six grandchildren by giving them funds to open those accounts as well. This takes them to the next level in their investing education.

I continue to respond to requests from our grandchildren when they have investing questions. Recently I helped our oldest granddaughter with a refresher on the basics of investing. I also responded to another granddaughter’s question about investing for a class she was taking in high school. When that happens I smile. I like helping them now because I may not be around to help them later. When I see news about the Fidelity Youth Accounts or UTMA accounts, I want to understand how those changes impact our grandchildren.

Changes Can Confuse and Frustrate Us

Sometimes changes can frustrate or confuse investors. I noticed a recent post about Fidelity Youth Accounts that caught my attention. The reason was personal. As I mentioned, Cindie and I have given each of our six grandchildren $2,000 each to start their own Fidelity accounts. This is in addition to the cash we have given them in the UTMA accounts I manage for them until they reach adulthood. I am the custodian of the UTMA accounts, so I manage their accounts including the buying and selling of investments.

This is what I noticed in the Fidelity Investor Community: “Fidelity offered a Youth account for any teen 13-18 yrs old. It included a Debit Visa and a brokerage account. It was so outstanding, and I set up a total of 15 youths with this account. It was a place to teach investing, debt, DCA, and Fidelity had these neat tools and videos to help this process. On March 31st, Fidelity closed all youth Accounts. Interesting that now Charles Schwab has taken up what Fidelity gave up and started Youth Accounts. This was upsetting to me, and I’d like to know the reasons behind Fidelity doing away with Youth Accounts.”

The short answer from Fidelity was that Youth Accounts are not going away. There are, however, some good changes.

Fidelity’s Investor Community Response

There are just too many apps on my phone. If I needed to have an extra one for a young person in my home, I would prefer not to have one that just adds clutter. So Fidelity’s decision to make life easier for parents and their teens is a good one.

“FidelityJohn” had this to say in response: “Thanks for taking the time to share your thoughts with us, @foreverretired. We sincerely appreciate your dedication to teaching the younger generation about how to start saving and investing, and we’re glad to hear you’ve been using the Fidelity Youth Account to that end.

I want to start by letting you know that the Fidelity Youth Account is not going away; instead, the separate Fidelity Youth app, which until recently was the main way parents and teens interacted with the account, is being discontinued. We are not closing any Youth Accounts as part of this transition, and new Youth Accounts can still be opened online.

Most of the features the Fidelity Youth app offered are being transitioned to the flagship Fidelity Investments mobile app, where teens will have a tailored experience just for their Youth Account. Teens can now have a smoother transition when they take over the account once reaching adulthood, without having to learn a new platform.”

A Follow-up Question About UTMA Accounts

As a result of this conversation, another Fidelity client asked this question: “How did the Youth accounts differ from a UTMA account? I opened UTMAs for each grand kid shortly after birth as soon as they got their SSN’s. They are all brokerage accounts which I fund with gifts on birthdays, Christmas graduations, monthly auto transfers, etc. The oldest is now 18. When they reach the age of majority (differs by state) the account converts to a regular account. I haven’t tried to order a debit card for any of the accounts, but I thought about it for the oldest who will be in college next year. Age of majority is in PA is 21. If I can’t open a debit card, maybe that is a difference.”

The Response from FidelityLizG

This is a helpful summary: “I’m chiming in here to help you with the difference between our UTMA and Fidelity Youth Account offerings. Since you mentioned that you have several Uniform Transfers to Minors Act (UTMA) accounts for your grandchildren, we’ll start there. UTMAs are custodial accounts and are for the benefit of the minor and managed by the custodian. As the custodian, you manage trading, as well as any deposits or withdrawals, and the beneficiary doesn’t have access to view or interact within the accounts until it is transferred into their name. As you mentioned, this typically happens when the beneficiary reaches the age of majority in their state. Debit cards are not available on these accounts.

Let’s visit the Fidelity’s Youth Account next. These are designed to help teens between the ages of 13 and 17 learn about financial literacy through hands-on experience. The account was designed to teach responsible spending, saving, and investing behaviors. The account needs to be opened by parents or guardians; however, the ownership and control of the account belong to the teen. Additionally, the teen would be able to request a debit card, should they make their decision with their parent or guardian.

If you’re interested in learning more about Fidelity Youth Accounts, I’ve put the link below for you.”

Fidelity Youth Accounts LINK

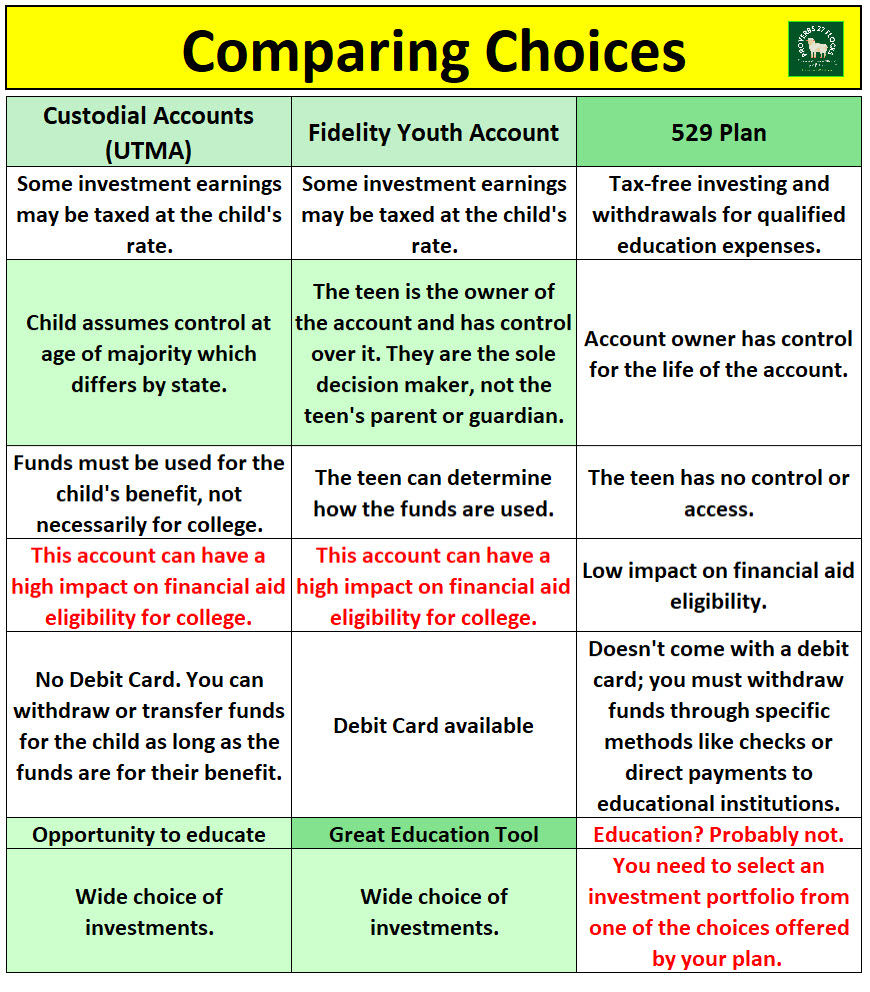

Comparing the Choices

There are three main ways to help your child prepare for their future. The first is certain the UTMA account. Obviously I also think the Youth Account is beneficial. However, there is another choice: The 529 education account. Here is my high-level comparison. While I know some really want financial aid for college expenses, I’m not a big fan of that avenue. I’ve seen far too many adults struggle with the huge debt burden that comes with “financial aid.”

What controls does a parent have over a teen’s Fidelity Youth® Account?

“Parents have certain controls over a teen’s Fidelity Youth® account. They must initiate and approve the opening of the account. They will retain the ability to close the account and/or cancel the debit card at any time, if their teen has one. They will have “inquiry access” to the account as an Interested Party, allowing them to review debit card statements, trade confirmations, and account transactions. The parent/guardian is designated as the “trusted contact” on the account and can be contacted should a situation concerning the teen’s welfare arise. However, the parent/guardian of the Fidelity Youth® Account cannot transact in the account or withdraw money from the account.” – Source: Fidelity Investments

Fidelity Youth Account: What happens when my teen turns age 18?

Fidelity lists the following:

Once the teen reaches age 18, the Fidelity Youth® Account must be converted to a standard Fidelity brokerage account. The assets will stay in the same account and keep the same account number and login credentials.

As the account owner, the teen will need to agree to a new set of governing documents, including a new account agreement. They will be prompted to convert their account starting on their 18th birthday and will have 60 days from their birthday to complete the account conversion process before their account is locked.

If the teen has a Fidelity Youth® debit card, it will continue to be valid until it expires. At that point, a new brokerage debit card will be issued. They can access information about their card on the debit card page.3

The Fidelity Youth® Account is not a custodial account, and the state law definitions of age of majority that pertain to the transition of custodial accounts do not apply to Fidelity Youth® Accounts.

Recommendations

First of all, think about the things you can do to follow King Solomon’s wise advice. “A good man leaves an inheritance to his children’s children, but the sinner’s wealth is laid up for the righteous.” Proverbs 13:22

This isn’t just about the money. It is about how you prepare your children and grandchildren to live in a complicated world that often mismanages money and doesn’t think about investing or giving from the fruits of those investing efforts. This also applies to aunts, uncles, and anyone who cares about young people in their lives. You don’t have to be a parent or grandparent to help a young person.

Secondly, give your young person the benefit of the things you have learned. Tell them about the mistakes you have made. Tell them about the change you have made over time. Of course it is important to do this in an age-appropriate manner. However, I have found that teens are more than capable of understanding the Rule of 72, the concepts related to investing in a diversified manner using ETFs and low-cost mutual funds, and in what a “stock” or “bond” is. They also can see the benefits of using a tool like Seeking Alpha.

Are there risks with giving young people $2,000? Yes there are. Not every child or teen will follow your example or advice. But your responsibility isn’t to make their life decisions for them. Your responsibilities are to train and to set an example. Someday they may surprise you by what they did with what you taught them.

All scripture passages are from the English Standard Version except as otherwise noted.

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com