Sizable Changes Over Time

The Fidelity community includes Fidelity employees. They ask questions of the community to generate discussion and ideas. For example, “FidelityAmber” asked this question: “Since you’ve started investing, is there anything money related that you’ve changed your mind about? Why or why not? Let’s discuss below.”

Then there are my readers with curious minds and great questions. One reader, Shawn, asked the following questions: “I was curious if you’d be willing to share, but I don’t know your background for employment and everything through all the years but when you were in your early 50s, where were you at in terms of your retirement accounts what I mean is what did you have for value compared to now almost 20 years later? Were you investing as much as you possibly could at that time or was this something that happened more in the latter half of this timeframe?”

My Employment Background was Information Technology Leadership

From 1976 to 1999 (ages 25-48) I was employed at Universal Foods Corporation (UFC) in Milwaukee, Wisconsin. I started as a clerk in Data Processing, became a mainframe computer operator and eventually was promoted to the Operations Supervisor position overseeing the computer operators and data entry team. As time went on I was promoted to Operations Manager and then ultimately to Director of Operations in the corporate office. I contributed to a traditional 401(k) during my time at UFC.

In 1999 Cindie and I moved to Madison where I took a job as the VP of Information Technology at Conney Safety Products. Again, I contributed to a traditional 401(k) at the maximum company matching level. I was at Conney until 2009 (age 58) when the company was acquired.

During a brief time I did some consulting work for companies like the Prince Corporation in Marshfield Wisconsin.

In 2010 (age 61) I joined Parts Now! LLC as their CIO. My employment at Parts Now ended in September 2012 when the company was acquired. During the time I was at Parts Now I had a ROTH 401(k).

Older and Wiser

My 75-year-old self is more knowledgeable and, I hope, wiser. Much of this is the result of listening to good advice and rejecting poor ideas. Let’s face it. We don’t start out with much in the way of knowledge and many with knowledge have very little wisdom. The scriptures point out the value of wisdom. Even the wise need more of it.

“Let the wise listen and add to their learning and let the discerning get guidance.” – Proverbs 1:5

“The beginning of wisdom is this: Get wisdom. Though it cost all you have, get understanding.” – Proverbs 4:7

“If any of you lacks wisdom, let him ask of God, who gives to all liberally and without reproach, and it will be given to him.” – James 1:5

“For wisdom is better than jewels, and all that you may desire cannot compare with her.” – Proverbs 8:11

“Listen to advice and accept instruction, that you may gain wisdom in the future.” – Proverbs 19:20

I’m not done gaining wisdom. The best way to get it is to ask God for it. However, he also provides others with wisdom to help us learn about the best way to gather information, understand the information, and act on the information. That has certainly been true in my life.

Some Investing Context

Changes to Investments in Those Years

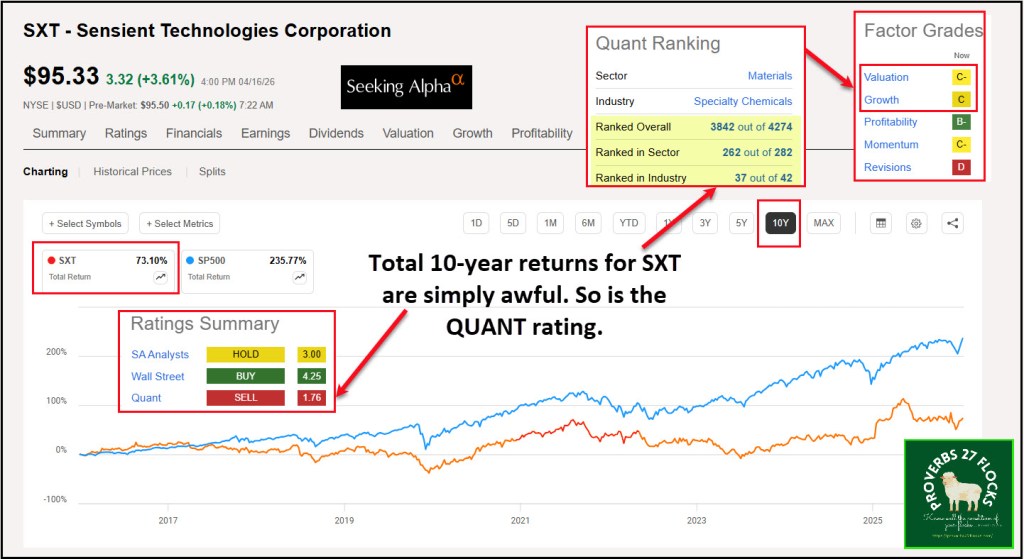

The most significant employment I had from 1976 through 1999 was at Universal Foods Corporation (UFC) in Milwaukee, Wisconsin. I was, quite frankly, an investment idiot. Thankfully I still made the wise decision to participate in the company 401(k), and I increased my contribution as I received raises and promotions. When I left UFC and Conney Safety Products I rolled the 401(k) accounts into my Fidelity Traditional Rollover IRA. (UFC is now Sensient Technologies – it isn’t a very good investment. The ticker symbol for Sensient is SXT)

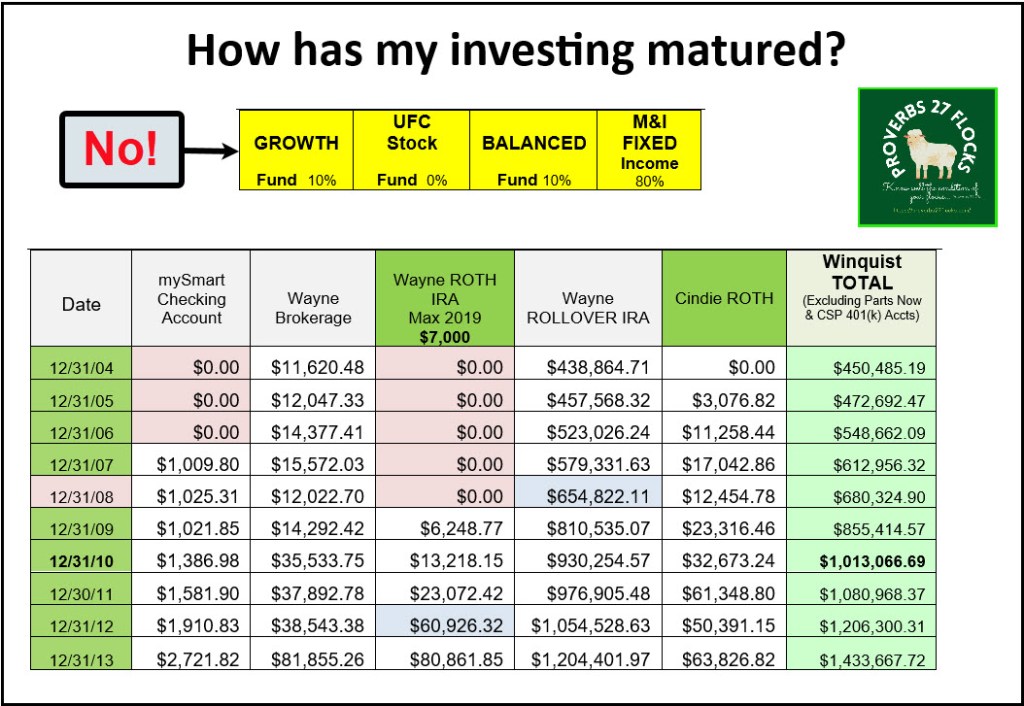

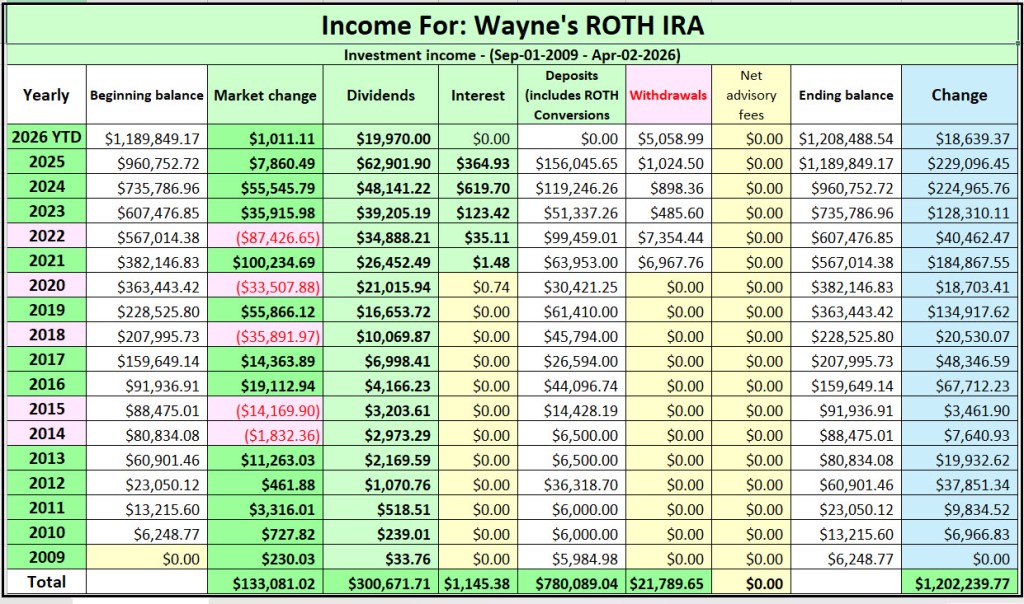

At the end of 1998 and just as we were getting ready to move to Madison for a position at Conney Safety Products, my traditional IRA had a balance of $333,915. In November 1997 my traditional 401(k) at Universal Foods Corporation was $173,389 and I also had an ESOP of Universal Foods stock worth $78,753.51. I also had a very small brokerage account at RW Baird that was fueled by stock options from UFC. The balance of that account in 1998 was $21,786. I owned shares of CPQ, HMK, IS, LHSP, PFE, SO and IFMX. Let’s just say the broker who was “helping” me was less than helpful.

My investment mix was awful. I had 80% of the total 401(k) in “Fixed Income.” Only 20% was in stocks (mutual funds.) To make matters worse, 10% of that 20% was in “Balanced Fund” investments. That is a recipe for long-term investing disaster. This allocation of assets is so far removed from my current views that I am certain our current retirement balances would not be what they are today if I had continued in that line of thinking.

What Has Changed?

The list of things that have changed is longer than you will want to read. However, I am convinced that, for the most part, investments that provide consistent dividends and dividend growth are the path to success. I also think that knowing some “rules” has changed my investment philosophy. For example, The Rule of 72 quickly clarifies the disaster of owning bonds, blended funds, and “target date” or “retirement date” funds.

Also, I have come to learn that things that seem mysterious or difficult to learn aren’t really all that mysterious or complicated. For example, you don’t need a list of twenty things to look at to find a good investment. It is better to focus on four or five things that matter and make decisions based on those critical factors.

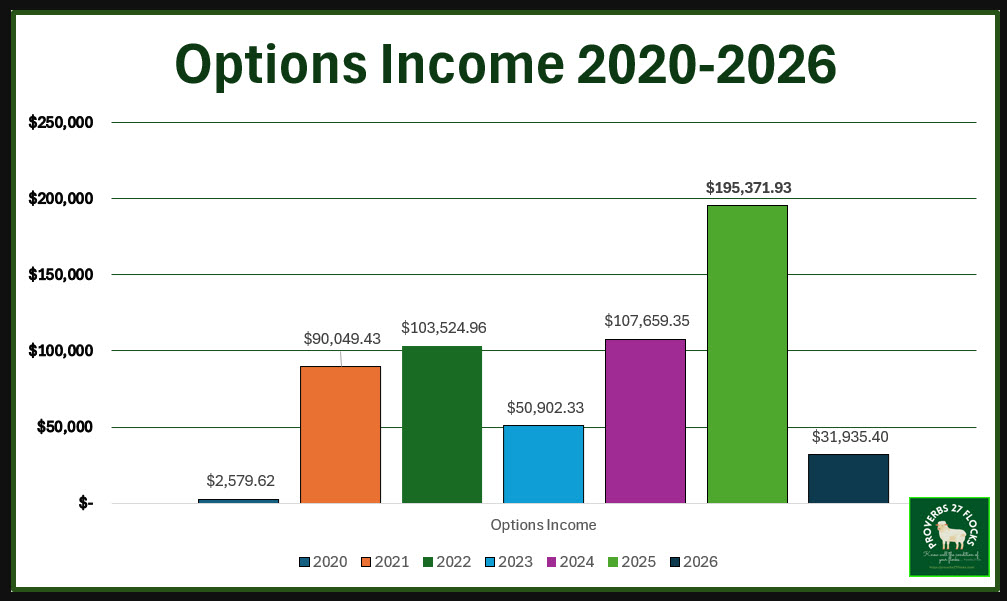

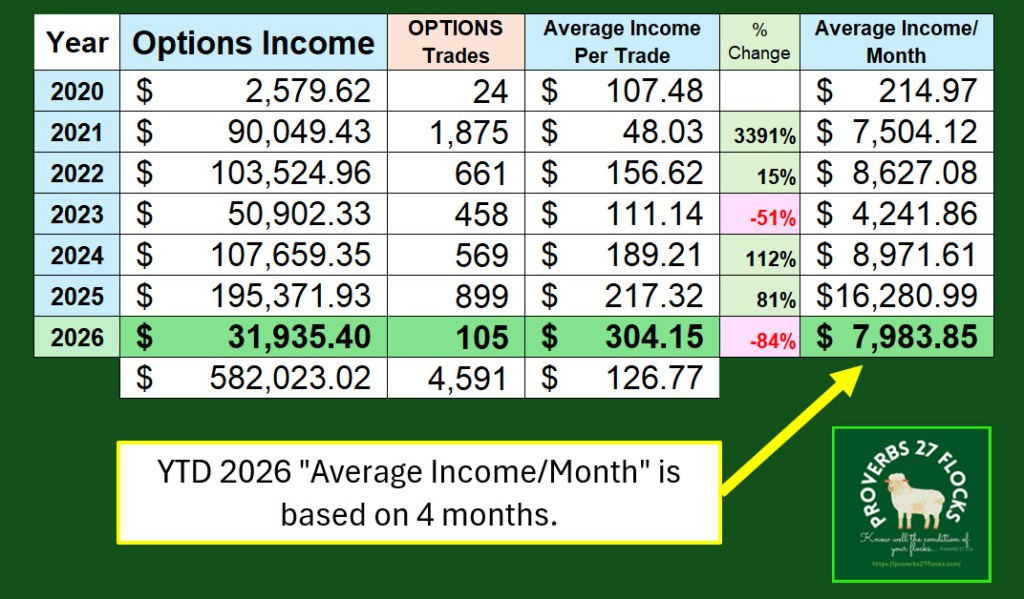

Many things have changed. I no long day-trade stocks but I do buy and sell options contracts on a regular basis. I do want to do ROTH conversions and pay the income taxes now and not later. I look at the horizon rather than the latest news from Ukraine, Iran, Washington DC, or the Wall Street Journal.

I have also discovered that paying a subscription for helpful information makes more sense than making foolish investing decisions. That is why I am willing to pay for a Seeking Alpha subscription.

What I Have Learned Influences My Investing Behaviors

There is no easy way to cover all of the bases in a single post. Let me share, with some additional commentary, what I said in response to FidelityAmber’s question on the Investor Community website. This is not exhaustive, but I can tell you that I would not have thought this way about these ten things in 1976.

1) Rebalancing used to make sense to me. Now it is the last thing on my mind. The goal is to buy quality investments. Whether or not I am “balanced” or need to rebalance is not an important question. Brokers and advisors want their clients to think that this is a good idea. I submit that it is questionable at best.

2) I used to think “balanced” funds and bond funds were a good idea. Now I run for the nearest exit when I see them recommended. The total returns of all bonds and bond funds ignore the reality of inflation and they ignore the times when bonds have not been a good investment.

3) Costs matter. I didn’t really understand the silliness of some expenses that didn’t offer results. When I was young, I thought paying more would get me more or better results. That doesn’t work in most areas of life.

4) Advisors like to take the “safe” path and, therefore, fail to recommend some investments because they are volatile. I have come to understand that risk and volatility are two different things. Volatility is the normal thing that happens in the market each week and sometimes every day. Risk is buying junk and expecting it to last and perform.

5) Annuities are VERY expensive insurance. Even when they are repackaged they are usually a very bad idea. There is a rule that wise investors always follow. If you don’t understand something, then it isn’t an investment you should buy. In my experience, the vast majority of those who purchased an annuity only heard one side of the story: the agent’s view.

6) Day trading is a waste of my time. I tried it on Interactive Brokers and made very little progress based on the time it required. Day trading does not, generally, care as much about quality as I think the long-term investor should. Options trading, I believe, is a far less time intensive way to earn significant cash.

7) Dividend growth investing is easy income that can be a powerful wealth builder. Autopilot works just fine and provides easy income. One of the ways to track this is to become somewhat proficient in a tool like Microsoft Excel.

8) Total Returns matter. This means dividends plus price growth.

9) Think Long-Term. This is more than just about investing in general. This is about what happens to Cindie if I head to my eternal home (John 3:16) before she does. This also means that Cindie and I delight in funding UTMA accounts for our grandchildren and giving them some seed money to start their own Fidelity Youth Accounts when they became teenagers. This also includes thinking long-term about inflation and income taxes.

10) I am just the manager. This is connected to what the Bible clearly teaches. I really own nothing. Someday I will be held accountable for what I did with the resources God has placed in my hands to manage. That type of thinking informs every aspect of our finances, including our giving. If you die with a large pot of gold and enter eternity without understanding what the Bible says, you are bankrupt and won’t like the long-term consequences.

Closing Thoughts

What part does wisdom play in your investing mindset? Does your advisor try to “rebalance” your investments? Be sure to ask questions if you don’t understand why this is recommended by your advisor. Sometimes they create income for their own wellbeing by doing what they do.

Do you have an investing goal that is something you can measure? Does it have a time element? Does it factor in the ultimate reality of RMD withdrawals? Does it ensure increasing income? If not, perhaps you won’t be satisfied with your results unless you have “luck” and things just go your way by chance.

Seeking Alpha Subscription Information

Of all of the resources I use, the most helpful is Seeking Alpha. The Seeking Alpha QUANT rating is a huge factor in my investment success. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com

Wayne

I am constantly amazed at your investing prowess. I have tried everything or at least it seems that way and yet I keep coming back to your website and being amazed at the wisdom I find. A big part of that is that you are a Christian man! The way you make public your investments and life is amazing!

But I have a problem I just can’t bring myself to eliminate bonds because being 81 I still remember 1999 and 2008 clearly. So today I find myself sitting in a balanced ETF CGBL. But I can’t help but be envious of how well you have done. Perhaps you could help me to find my best investment mix?

God Bless

Terry Justison

LikeLike

Wayne

I am constantly amazed at your investing prowess. I have tried everything or at least it seems that way and yet I keep coming back to your website and being amazed at the wisdom I find. A big part of that is that you are a Christian man! The way you make public your investments and life is amazing!

But I have a problem I just can’t bring myself to eliminate bonds because being 81 I still remember 1999 and 2008 clearly. So today I find myself sitting in a balanced ETF CGBL. But I can’t help but be envious of how well you have done. Perhaps you could help me to find my best investment mix?

God Bless

Terry Justison

LikeLike

I remember 1999 and 2008 as well. The problem is that many people consider those years the norm instead of viewing it as a speed bump. The best thing about down markets is that they weed out the bad investments and the good ones forge ahead. In my opinion, bonds have never been a wise long-term strategy. They seem to bring comfort to those who dislike volatility, but they don’t add much in the way of total returns. I wish you well and hope you continue to learn. We all need to do that.

LikeLike