If You Don’t Save Don’t Fret About Income Taxes

It has been several weeks since I started this “book” series. If I were to publish it in some other form someday I would reorganize the chapters. This time I’m returning to a topic I have touched on because I think far too many of us delay some key decisions that should be strategic and that should be executed at least annually. Thinking about future income taxes is one of those key items.

I have some friends who have entered retirement and they did not save or invest during their working years. They don’t have to spend much time thinking about income taxes because their income is primarily from Social Security. They also shouldn’t bother with ROTH conversions if they have a traditional IRA or 401(k) because their total balance is less than $100K. This is not a desirable condition, but it is their reality.

If you are younger than 50 years old, it is highly likely that you have most of your retirement assets in a ROTH IRA or a ROTH 401(k). If that is you, then income taxes are likely to be less of a concern for you when you reach your retirement years.

For almost everyone else, there is a ticking time bomb. When it will go off for you depends on your age. Required Minimum Distributions (RMDs) are required from tax-advantaged accounts like IRAs and 401(k)s starting at age 72. So, if you are 55 years old, be ready for a potentially surprising income tax bill seventeen years from now. If you are married, filing jointly the pain is less pronounced, but if one of you dies with a large traditional balance the income tax burden can be substantial. The damage done by income taxes can be considerable.

Ordinary Income Will Be Taxed

RMDs are taxable. Amounts withdrawn from Traditional IRA, 401(k), 403(b), and similar plans are taxed as ordinary income. They add to your AGI and can push you into a higher tax bracket. Remember that you will also be receiving Social Security, so the combination of your income from that government program plus your RMD can be a big number. It might even be bigger than your income during your working years. It certainly is for us.

Ordinary income refers to earnings subject to regular income tax rates, including wages, salaries, tips, bonuses, and business profits. It also includes your RMDs. Social Security benefits are not considered “ordinary income” for tax purposes, but a portion of them can be taxable depending on your combined income. If your combined income exceeds certain thresholds, up to 85% of your benefits may be subject to federal income tax. So that does need to be considered.

Avoiding or Reducing the Size of the Income Tax Explosion

Roth IRAs have no RMDs during your lifetime; Roth 401(k) and Roth 403(b) also no longer have RMDs (SECURE 2.0). Therefore, putting money in a ROTH is worthy of consideration if your current income tax situation permits.

If you are generous, you can minimize the sting of the RMD by using Qualified Charitable Distributions (QCDs). If you’re 70½ or older, you can donate up to $111,000 (2026) directly from an IRA to a qualified charity. The QCD counts toward your RMD and is excluded from taxable income. This can reduce your tax bill significantly. See IRS Publication 590-B for details.

The Qualified Charitable Distribution (QCD) limit for 2026 is $111,000 per individual. For married couples filing jointly, each spouse can donate up to this limit from their IRAs. However, Cindie is not yet 70½ and most of her assets are in her ROTH IRA, so she won’t benefit from this IRS exclusion.

If You have Multiple Retirement Accounts

You have to calculate the RMD for each account separately. For IRAs (Traditional, SEP, SIMPLE), you can take the total RMD from any one or more IRAs. For 401(k)s and 403(b)s, you must take the RMD from each plan separately—no aggregation across plans. From my perspective managing multiple accounts on different platforms is just too much work. My advice: Consider moving all of your retirement assets to a single provider like Fidelity Investments. If you have retirement savings with a previous employer, create your own rollover IRA or rollover ROTH IRA so that you can focus on the big picture.

Calculate your Retirement Income Now

Even if you aren’t retired yet, there is a fairly good chance that you will be some day. Social Security provides estimates of the income you can reasonably expect at various ages based on your earnings history. Your spouse, if you are married, should do the same.

Then, calculate your RMD amount based on what you believe you can reasonably expect to have in your traditional IRA at age 72. You can use IRS worksheets for this or create your own spreadsheet. There are web sites that can do the calculations for you. Here is one: RMD Calculator

The sum of these numbers, plus income from other sources like pensions or rental properties can help you understand your true income tax situation. Bear in mind, however, that your income may be considerably more in retirement than you envision today. This is especially true for disciplined savers and wise investors.

Understand the Income Tax Implications

Whether you like it or not, you might wind up in a higher tax bracket. In fact, as you age, if your IRA balance is significant, your income taxes could increase as you get older because your RMD can grow in size. Remember this: if you stay invested, even when withdrawing funds from your IRA, the account balance might continue to grow or at least be the same. Either way you will pay more income taxes the next year.

The Medicare Premium Taxes

There is something called IRMAA. IRMAA stands for Income-Related Monthly Adjustment Amount, which is an additional charge added to Medicare Part B and Part D premiums for high-income beneficiaries. It is based on your modified adjusted gross income from two years prior.

Therefore, even after you calculate your income taxes, there are other taxes that can reduce your Social Security income. Be aware of how your RMD impacts other tax considerations, like Medicare premiums and the taxability of Social Security benefits. IRMAA can be quite a surprise if you aren’t prepared for that tax.

ROTH Conversion Impacts

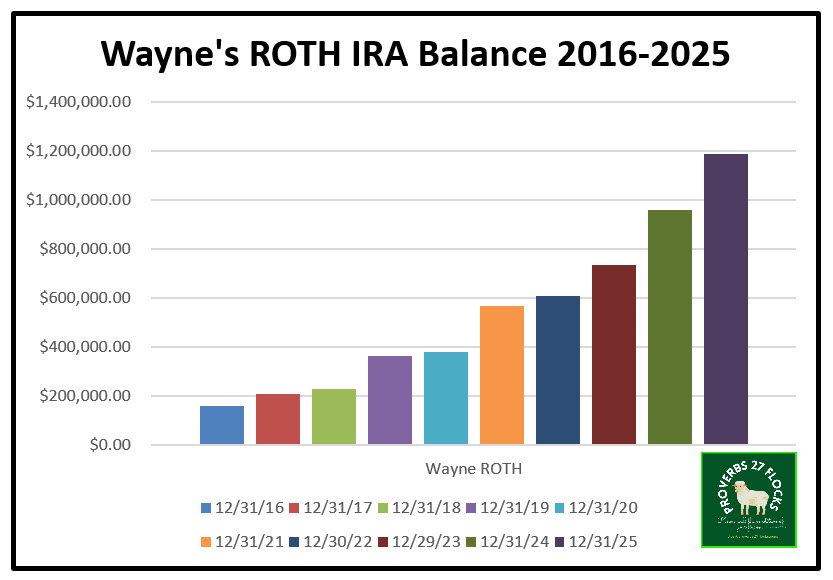

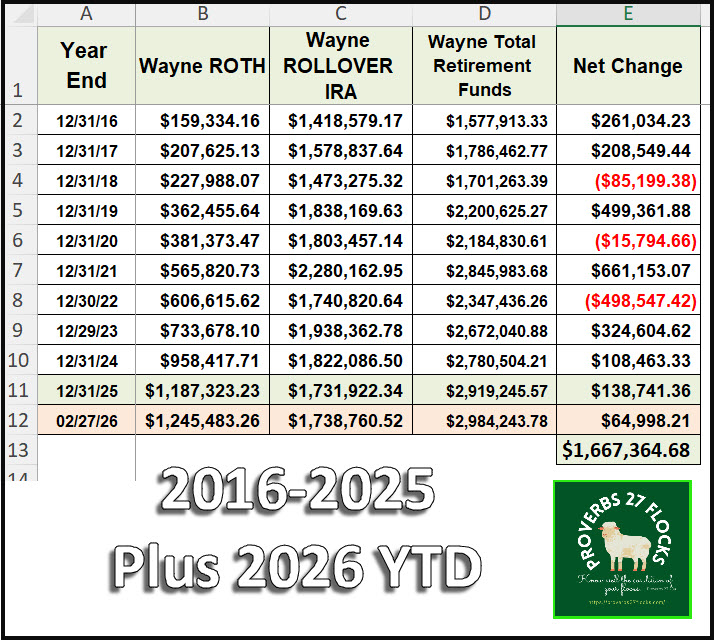

I won’t rehash this because I’ve talked about it in previous posts. My ROTH IRA has grown from $159,334.16 in 2016 to $1,245,483.26. This was accomplished by strategically moving stocks and ETFs from my traditional IRA to my ROTH and paying the income tax each year. Now, if Cindie or I or our heirs withdraw from the ROTH there is no income tax to be paid. Bear in mind that all income from dividends and from trading options in my ROTH IRA are also income tax free.

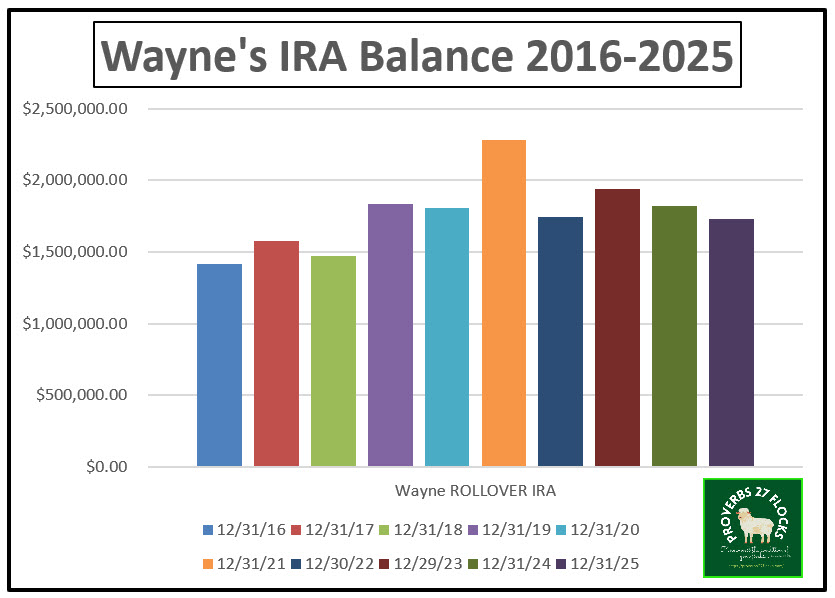

In spite of that diligent discipline, my traditional IRA has grown from $1,418,579.17 in 2016 to $1,738,760.52 today. This growth is after all of the QCD giving, ROTH conversions, and RMD withdrawals. At the present IRA balance, my RMD is just over $70K. That number helps inform the ordinary income taxes I would pay on that withdrawal if I did not do QCD giving.

Illustration Using my ROTH IRA and Traditional Rollover IRA

The first image shows what happened to my ROTH IRA from 2016-2025. There are a number of factors that have contributed to the increase in the total balance. First, of course, are ROTH conversions from my traditional IRA. But there are three other factors: 1) the growth in the value of the investments (price returns), 2) dividends that are paid by these investments, and 3) covered call option income.

The second shows what has happened to the balance of my traditional IRA. Bear in mind that some of the same things have been happening in this account. I trade options and the annual dividend income is significant. However, because I am 75 years old we are able to give charitable gifts from this IRA using the QCD approach.

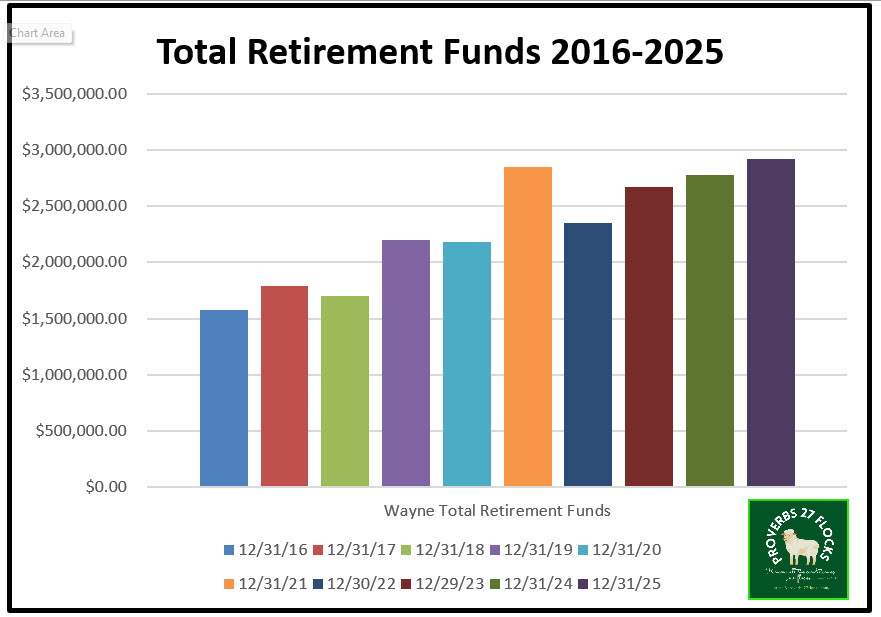

The third image shows what has happened when we combine the year end totals of both accounts. The reality should cause you to ponder your own situation.

The final image shows the data in a table. Some people like graphs, some like numbers and some like both. Notice that I have a way of observing the year end balances. This is part of a disciplined investment strategy that keeps an eye on RMDs.

Plan Your Strategy Today

Consider your overall income needs and potential tax implications when timing your withdrawals. Spreading withdrawals over several years can help manage tax burdens.

Summary

By understanding the RMD rules, accurately calculating your distributions, and strategically planning for tax implications, you can effectively manage your retirement income and minimize tax liabilities. This proactive approach can help ensure that RMDs complement your overall financial strategy.

Actionable Items

Do you like to live in a world of uncertainty? Then don’t think about goals or set them.

- Do you have an estimate of your Social Security income? If not, sign up for a Social Security account and explore your potential income for various retirement ages.

- Have you calculated your RMD based on your current traditional IRA or 401(k) balance? It isn’t hard to do. If you have 17 years before retirement, use the Rule of 72 to estimate when your account may double in size. For example, if you current IRA balance is $1M, and you are gaining 10% per year on average, your IRA will grow to $2M in about seven years.

- Proverbs 16:3 “Commit your work to the Lord, and your plans will be established.” This means that those who trust the Lord should look to him for wisdom in the decisions that are made today.

Conclusion to Chapter Ten

Like almost everything of importance, ignoring something that is coming your way is probably the least desirable approach to living. If the roof on your house needs to be replaced in ten years, it makes sense to start thinking about how you will pay for it ten years before the replacement is needed. This same thinking applies to RMD and income tax planning in retirement.

Seeking Alpha Subscription Information

Of all of the resources I use for long-term thinking related to investing, the most helpful is Seeking Alpha. Mutual funds do not have QUANT ratings. This makes them less likely for me to recommend as a part of your investment portfolio. If you decide to explore a Seeking Alpha subscription, please use the following link. Seeking Alpha

SEEKING ALPHA INFORMATION AND SUBSCRIPTION

You can also scan this QR Code to get the same information.

Past performance does not guarantee future results, Seeking Alpha does not provide personalized advice, and it is not a registered investment adviser.

We accept advertising compensation from companies that appear on our site. This website represents my opinions, which may not reflect those of Seeking Alpha, and does not constitute an investment recommendation or advice.

If you have any questions or problems getting connected to Seeking Alpha, reach out to them with this email address: subscriptions@seekingalpha.com

All scripture passages are from the English Standard Version except as otherwise noted.

Wayne,

I deeply appreciate your insights. Thank you for sharing these so freely. I have forwarded emails and recommended your site to others. May the Lord continue to bless you and make you a blessing to others!

I’ve just published a book that you might find of interest. It’s to be released this week on Thursday, March 5. https://grassmarket.press/remember-the-poor/ And I was recently interviewed on the Stewardology podcast. https://stewardologypodcast.com/283-remember-the-poor-ft-pete-smith/

I also appreciate your emphasis on generosity. You are leading the way!

Sincerely,

Pete Smith

LikeLike

Generosity is one way we can image God. He has been generous towards us in so many ways that to be less than generous with what he has loaned us is a very poor stance. Thanks for sharing your thoughts and the link to your book.

LikeLike