Age is Relative: 60 or 969 Years Old?

There aren’t many specific references to “age” in the Bible other than the age when someone died. For example, in Genesis Moses recorded an amazing death notice: “Thus all the days of Methuselah were 969 years, and he died.” Genesis 5:27

In 1 Timothy 5:3, 9-10 Paul gives Timothy some advice about widows. He said, “Honor widows who are truly widows” and “Let a widow be enrolled if she is not less than sixty years of age, having been the wife of one husband, and having a reputation for good works: if she has brought up children, has shown hospitality, has washed the feet of the saints, has cared for the afflicted, and has devoted herself to every good work.”

Investors should also be age conscious.

Ages Investors Should Heed

AGE 13 When a young person reaches this age, they can open a Fidelity Youth Account. This is a perfect opportunity for a parent, grandparent or other family member to help a young person get started with investing.

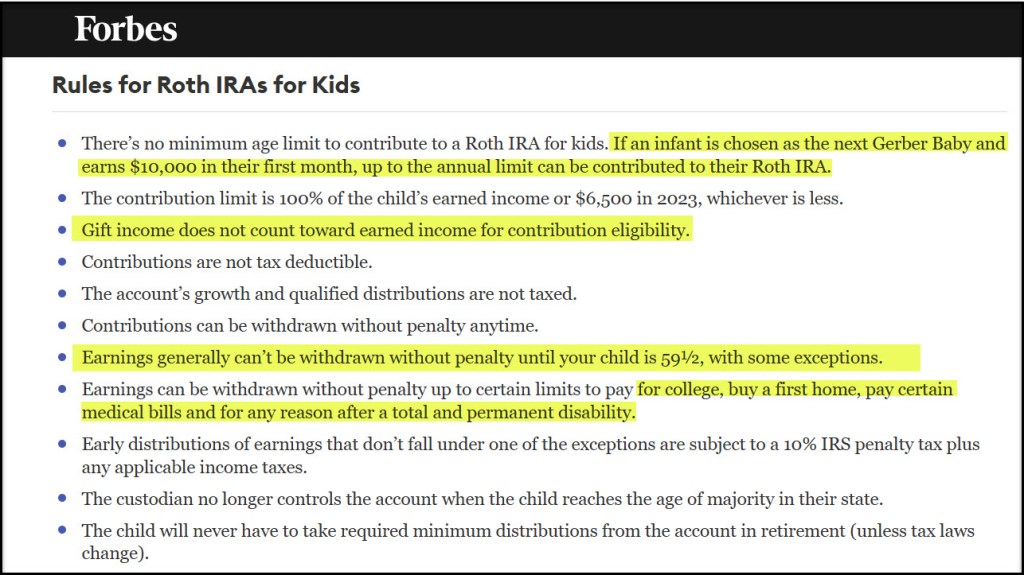

It is also possible for a young person to start investing before then. The tool for this is the custodial ROTH IRA. However, the child must earn income for this to be used. “A Roth IRA for kids is formally called a custodial Roth IRA. A custodial account is one that an adult, usually a parent, opens and manages for a child. The child gets full control of the account once they’re 18 in most states.” – SOURCE: Forbes

AGE 50 Eligible to make catch-up contributions to retirement plans such as SIMPLE IRA, SARSEP, 403(b), 457(b), 401(k) , Roth and Traditional IRAs. Catch-Up IRA contributions: Catch-Up IRA Contributions: Individuals aged 50 and older can contribute an additional $1,000, unchanged from 2024. In other words, you can contribute up to $8,000 of earned income.

AGE 59.5 Withdrawals from an IRA or 401k are possible without penalty. There are limitations.

AGE 62 This is the minimum age to collect Social Security retirement benefits. If you are a surviving spouse, you may collect as early as age 60 with reduced benefits. Note: You can start collecting Social Security retirement benefits as early as age 62, but your benefits will be reduced if you take them before your full retirement age. The full retirement age varies depending on your birth year, typically ranging from 66 to 67.

In my opinion, it rarely makes sense to delay taking Social Security beyond age 65. I started taking my benefit at age 63 in 2014. I think I know how to manage the dollars better than the government.

AGE 63 If you start Medicare at 65, 63 is the start of lookback period for the IRMAA adjustment to premiums based on taxable income. If you want to manage your taxable income to lower or avoid IRMAA, then age 63 is when to start. I’ve talked about IRMAA in previous posts. This year Cindie and I will have slightly higher Medicare premiums due to our income level and IRMAA. However, I’ve done the math, and it is worth the extra cost for several reasons.

AGE 65 You are eligible to start Medicare. It is wise to apply 3 months before your 65th birthday. Otherwise, Medicare (Part B) and prescription drug coverage (Part D) may cost more money. Some individuals can be entitled to Medicare at an earlier age only if they are entitled to Social Security disability benefits.

AGE 65 If you don’t itemize deductions, then your federal standard deduction increases if you are age 65 or older on the last day of the year. This can be very helpful if you are making QCD charitable giving contributions and your itemized amounts shrink as a result.

AGE 70 Don’t wait beyond this age to delay collecting benefits. Delaying the collection of Social Security retirement benefits beyond 70 does not increase the benefits.

AGE 70.5 This is a wonderful opportunity. You are now old enough to give Qualified Charitable Distributions (QCDs). I’ve written about this before.

AGE 73 This is the age for RMD’s from traditional retirement accounts. Required Minimum Distributions from some retirement accounts are mandatory. If you don’t take them be prepared to be penalized by the IRS!

A final reminder from Alistair Begg

“The Bible does not condemn business acumen or future planning. What the Bible does condemn, however, is a prideful, self-centered way of thinking that, whether intentionally or unintentionally, leaves God out of our decisions and future plans—a mindset that assumes certainties that are never promised to us.” – Alistair Begg

He also says, “Tomorrow is not promised. We may plan for it, but we may not assume we can control it. God’s mercy alone enables us to awaken to each new day. The sin of presumption is exposed as folly when we realize that our very life is grounded in God’s sustaining gifts. We cannot ignore our limitations and life’s brevity, but we can allow these realities to shape and transform our thinking and our decisions for the sake of His glory. So consider your plans for today, for tomorrow, for next year, and for further on in your life. Did you pray about them? Have you acknowledged that His plans are sovereign and that all of yours are contingent on His? Lift your plans up to Him now and place them in His hands. You cannot control the future. But you do not need to, for you know the one who does.”

All scripture passages are from the English Standard Version except as otherwise noted.