Are You Trying to Juggle Too Many Balls?

Life is complicated and the hours are few. Far too many have created unnecessary complications in their lives by failing to consolidate their financial accounts. Trying to keep track of multiple accounts at multiple brokers and banks can be very time-consuming and it is easy to drop one or more balls.

I see this frequently when helping others. They have old 401(k) accounts at a former employer or employers. They have more than one banking relationship. They get multiple statements, and as a result, usually don’t take much time to read them, much less understand them.

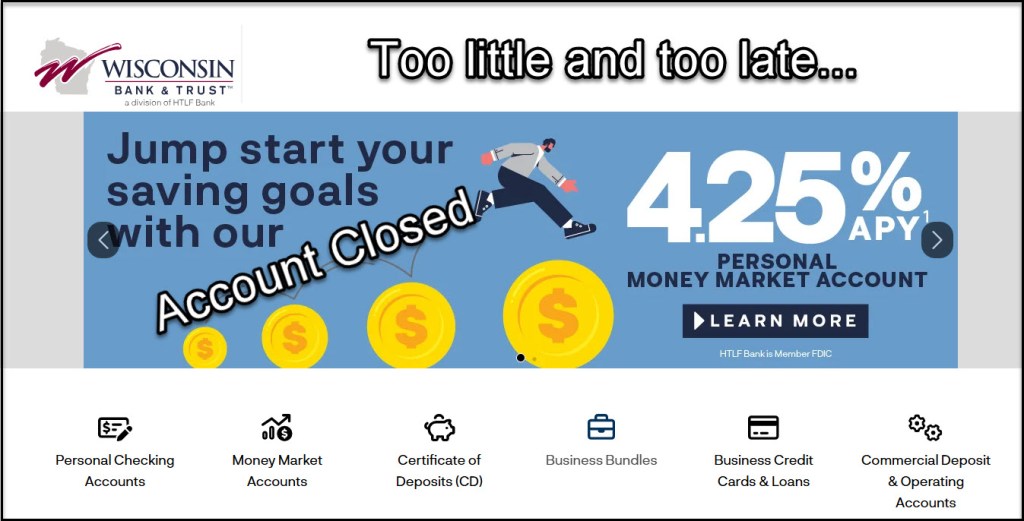

Simplified our Banking During 2024

We used to have at least three (if not more) bank accounts. Each one served a specific purpose. However, after looking at the modest and often inconsequential benefits from the different accounts, I decided to close them. Yesterday I stopped at our local Wisconsin Bank and Trust branch to close our checking account. The balance was less than $100.

I had kept it open thinking that it might be helpful to have a local banking relationship in the event that we needed something we could not do online or at an ATM. As it turns out, I haven’t seen any needs in the last twelve months, so I closed the account. We did the same with our Ally Bank account earlier this year.

The Benefits of Consolidation

There are probably more benefits than disadvantages to consolidation. These days every financial relationship has some online services. This means that you need to have a login ID and password. This is just one more path for scoundrels to use to compromise your financial health.

Furthermore, most smaller banks have a strained IT staff and budget for software and consulting experts. They cannot hope to have the same resources for security as a large firm like Fidelity has.

In addition, every institution has their own statement format. This makes it more of a chore to review each one. It is far better, if you own multiple investment accounts, to have them consolidated with a single broker.

Customer service is also a consideration. I have found that the phone support provided by Fidelity Investments is superior to the phone support (if available) from most banks I have used. In addition, the “doors” are rarely locked with a major provider like Fidelity, Vanguard and Schwab.

Most banks offer poor choices for CDs (Certificates of Deposit) and you have to jump through too many hoops to get the multiple CDs set up. Also, I have rarely found the bank’s CD rates to be competitive.

The one possible downside of not having a brick-and-mortar bank is that I cannot deposit cash using the Fidelity banking app on my iPhone. However, we rarely receive or use cash anymore.

Wisconsin Bank and Trust’s Final Attempt

When I walked into the WBT branch, I noticed a couple of things. It is a big branch but there were only two employees. The only employee servicing customers wasn’t even from this branch. He was there from a different branch. In addition, he did not have access to change for my checking withdrawal and had to go to the other employee to get change.

To his credit, he tried to offer me the WBT money market account. I declined simply because I don’t need an account that has a separate statement that I need to look at.

Great advice …i need to do consolidate all accounts as well. Thanks Wayne!!

LikeLiked by 1 person