Number Three of Twenty

This is the third in my series of posts about Howard Marks’ book THE MOST IMPORTANT THING. Today the topic is “value.” Value is an often-used word. Companies have “values”, or they lack values. We believe the $100 bill has value, even though it is made of paper. Education is perceived to have value. There are family values and community values. Something that is valuable is something of worth and is often unique or special. With that in mind, lives have value as well.

Proverbs About Value

“The tongue of the righteous is choice silver; the heart of the wicked is of little worth.” – Proverbs 10:20

Proverbs 28:19 says, “Whoever works his land will have plenty of bread, but he who follows worthless pursuits will have plenty of poverty.”

Jesus Had a View About Value

Sadly, far too many chase the trinkets of this life and ignore their own souls. There are two destinations for every person, according to Jesus. Because he valued the lives of people, he stated his mission was to “seek and save the lost.” This was more than just a temporary life-long investment, but one that would be everlasting. Jesus often encouraged his followers to look for value and understand their value.

Matthew 6:26 “Look at the birds of the air: they neither sow nor reap nor gather into barns, and yet your heavenly Father feeds them. Are you not of more value than they?”

Matthew 10:31 “Fear not, therefore; you are of more value than many sparrows.”

Matthew 12:12 “Of how much more value is a man than a sheep! So it is lawful to do good on the Sabbath.”

Chapter 3: Value

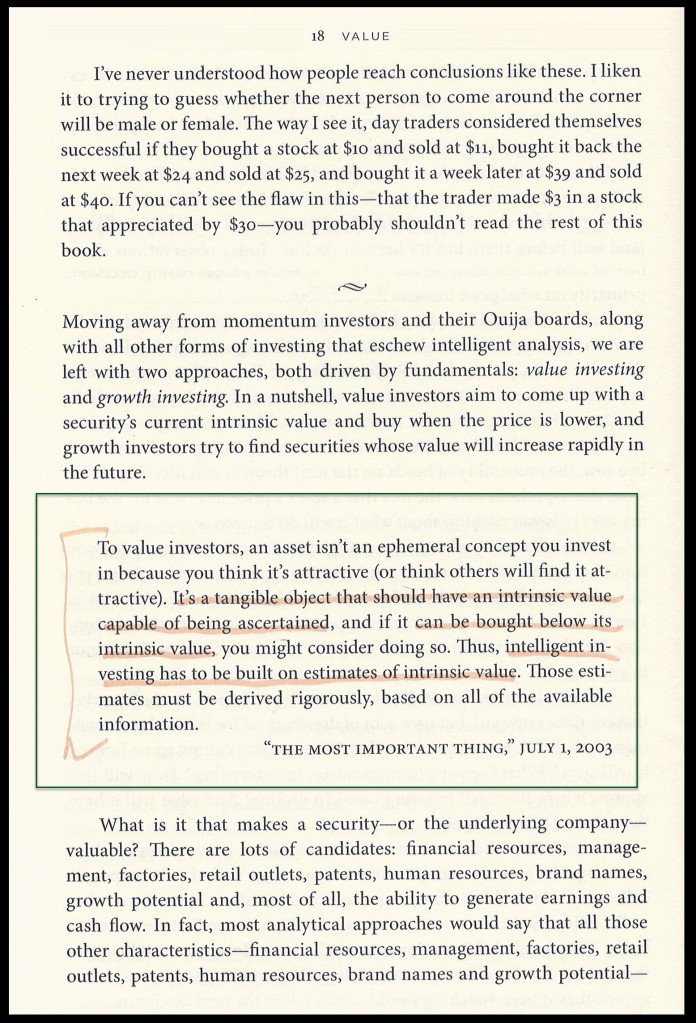

“For investing to be reliably successful, an accurate estimate of intrinsic value is the indispensable starting point. Without it, any hope of consistent success as an investor is just that: hope.” Howard Marks, p.16

Intrinsic value is the underlying true value of something. Even the Price/Earnings ratio is an indicator of value. The P/E ratio is high when investors believe the current price of an investment is too low. They are willing to pay more today for an investment because they believe the price of the shares will grow. If the current price of a share is $50, and the earnings are $1, then the P/E is 50.00. That is far too high for many investments, but the market is saying the investment is underpriced. If the price of a share grows to $100 per share because the earnings are $5 per share, then the P/E ratio has fallen to 20.00. Those who bought shares at $50, anticipating higher earnings, are very pleased with the doubling of their investment dollars.

The mantra is “buy low, sell high.” This is a value statement. The author says there are investors who invest based on the fundamentals (value) and those who prefer to chase upward price momentum using “technical analysis.” This involves reading charts and is often the practice of day traders.

Marks would have the reader understand that every investment has some intrinsic value. He suggests that intelligent investing is built on estimates of intrinsic value. The value can include patents held by the company, hard assets like property and inventory, cash, debt, product diversity, the competitive moat of the business, and a host of other fundamentals. There are intangibles like fashion, company talent, and long-term growth potential that have less weight in being able to forecast the future. “The quest in value investing is for cheapness.” (Marks, p.19)

How Is This Knowledge Useful?

You need to determine your strategy. If you are a day-trader, then you really don’t care much about the company’s intrinsic value. You want to buy for $25 at 10AM and sell for $26 before the market closes. Very few investors are truly successful using this model. Furthermore, it takes a lot of work. I know because I experimented with day trading using an Interactive Brokers account several years ago. It wasn’t worth the effort, even though I made some money doing it.

I decided focusing on dividend growth value investing was a better course of action. On Monday I purchased 500 shares of HPQ as a value investment. Yesterday I added another 100 shares of BMY to my traditional IRA as a value investment. I sold my shares of AMD (P/E ratio of 46.85) and bought value investments that pay a growing dividend. In the case of HPQ the price of the shares is going up. For BMY the price of the shares is in decline. It isn’t the momentum of either that determined my purchase. Rather, I think both have intrinsic value that is greater than the current price.

Other Insights From The Most Important Thing

There are really just two schools of investing. One is made up of value investors, and the other is the growth investing school, which includes day traders. However, the author wisely states, “Thus it seems to me, the choice isn’t really between value and growth, but between value today and value tomorrow.” (p.19) You and I should make informed decisions that are about value and then stick with those decisions until the value proposition changes.

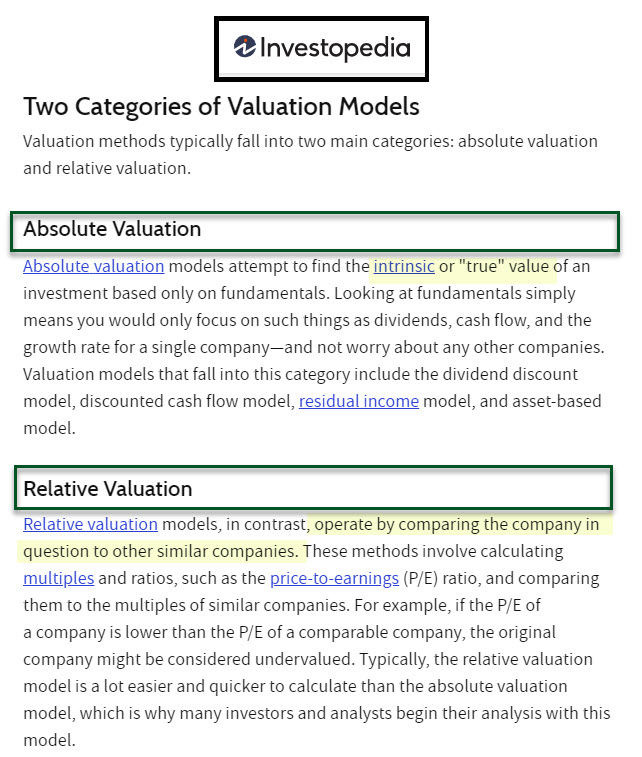

Consider the Methods Before You Invest: Investopedia

If you want to learn more, I suggest you read this article on the Investopedia website.

The Next Chapter is The Relationship Between Price and Value

The fourth “most important thing” is “The Relationship Between Price and Value.” The author starts the chapter by saying, “Investment success doesn’t come from ‘buying good things,’ but rather from ‘buying things well.’” (p.24)

All scripture passages are from the English Standard Version except as otherwise noted.