If You Are a Giver, Give Wisely and Liberally

In my first discussion of this in November I started talking about my QCD (Qualified Charitable Distribution) findings. I want to reduce my Federal and state income tax, maximize my ability to do ROTH Conversions, and increase our charitable giving in a tax efficient manner. Even if you are not 70.5 years old, it is worth knowing how this works so that you can help older family members or friends with managing their finances wisely.

What is a QCD?

“A qualified charitable distribution (QCD) is a direct transfer of money from an IRA to a 501(c)(3) charitable organization that is eligible to receive tax-deductible contributions.” Fidelity Investments

Am I eligible for QCDs?

“In prior years, the rules that permitted QCDs required reauthorization from Congress each year, and those decisions were sometimes made late in the calendar year. With passage of the Protecting Americans from Tax Hikes (PATH) Act of 2015, the QCD provision is now a permanent part of the Internal Revenue Code. This means you can plan your charitable giving and begin reviewing your tax situation earlier each year.

Because QCDs are not includable in income the QCD is also not deductible as a charitable deduction on Schedule A. As such, the QCD can remain an option for your charitable giving, even if you claim the standard deduction in a given year.” Fidelity Investments

The rules of QCDs (From Fidelity’s web site with some editing)

- You must be at least 70½ years old at the time you request a QCD. If you process a distribution prior to reaching age 70½, the distribution is taxable income. If the check for the QCD is made payable to you, it is also taxable income. The funds must go to the charity.

- For a QCD to count toward your current year’s RMD, the funds must come out of your IRA by your RMD deadline, which is generally December 31 each year.

- Funds must be transferred directly from your IRA custodian to the qualified charity. This is accomplished by requesting your IRA custodian issue a check from your IRA payable to the charity. You can then request that the check be mailed to the charity or forward the check to the charity yourself.

- The maximum annual distribution amount that can qualify for a QCD is $100,000. If you’re a joint tax filer, both you and your spouse can make a $100,000 QCD from your own IRAs.

- The account types that are eligible for QCDs include: Traditional IRAs, Inherited IRAs, SEP IRA (inactive plans only*), and SIMPLE IRA (inactive plans only*).

- Certain charities are not eligible to receive QCDs, including donor-advised funds, private foundations, and supporting organizations. You are not allowed to receive any benefit in return for your charitable donation. For example, if your donation covers your cost of playing in a charitable golf tournament, your gift does not qualify as a QCD.

What Has Been Done and Some Cautions

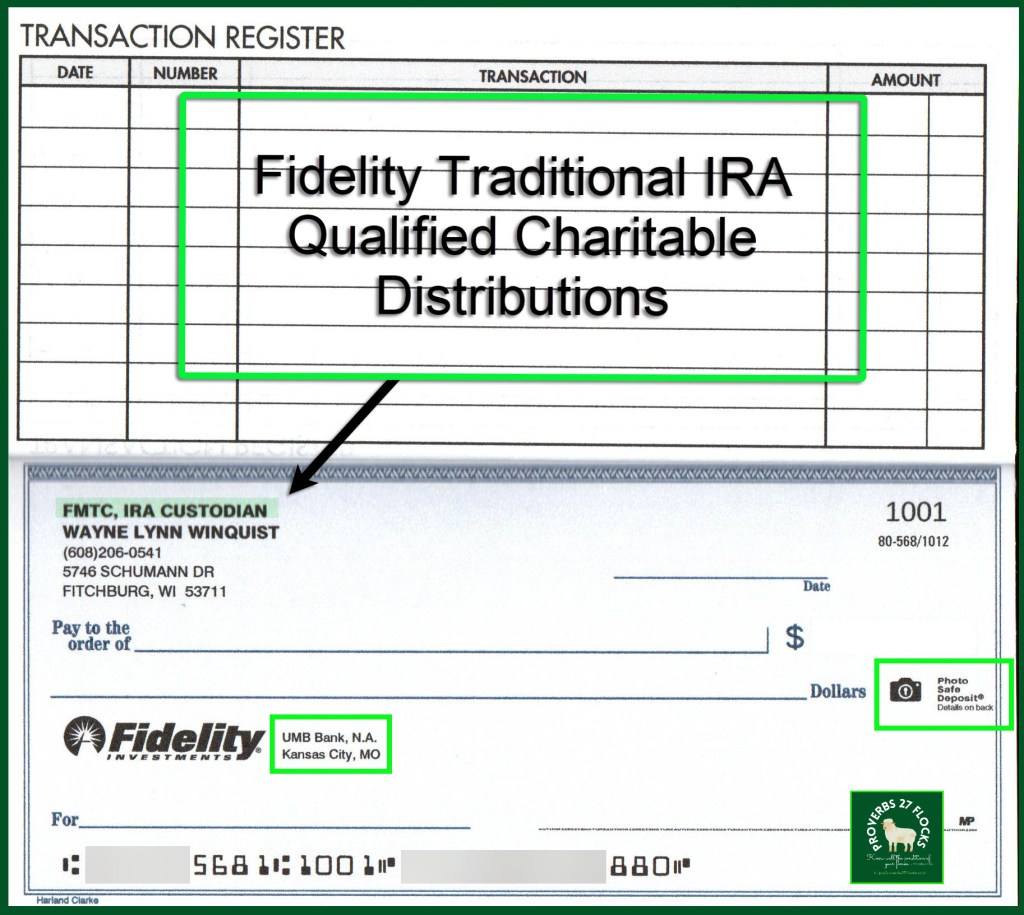

The first QCD contribution from my traditional Fidelity Investments’ IRA has been sent using Fidelity’s web site. I requested checks for my traditional IRA to make it easier to send funds directly to a charity without waiting for Fidelity to print and mail the check. Those checks arrived yesterday.

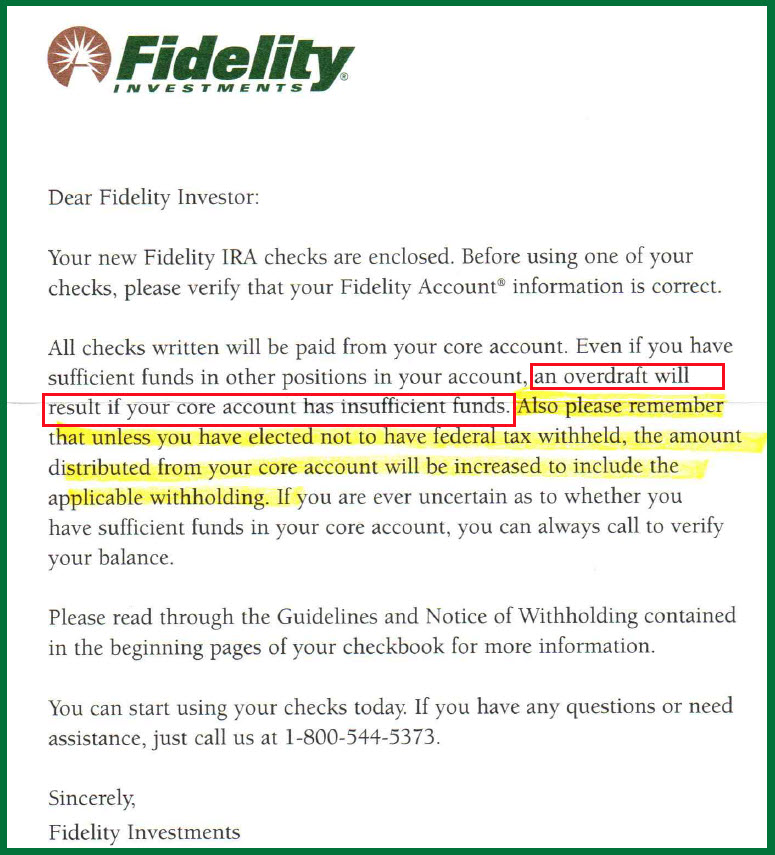

I also called Fidelity to verify that there would be no taxes withheld if I write a check. The Fidelity representative confirmed that there is no withholding set up as the default for my account. Therefore, if I write a check for $10,000, the entire amount goes to the charity and there is no additional cash that is sent to the IRS or to the Wisconsin Department of Revenue.

I also read the fine print and warnings. For example, if I have $9,000 in cash in my account, and I write a check for $10,000, that creates an overdraft situation. OVERDRAFTS are NOT permitted on IRA accounts.

Furthermore, if a charitable organization does not cash the check by the end of the year, it does not count towards the RMD. You should encourage charitable organizations to cash the checks promptly.

Verify With the Charity

I have already checked with three of the charities we support: our church, the camp where our granddaughter serves as a counselor and that our church supports, and the private school our grandchildren attend. Each of them understands that the QCD needs to be reported separately from normal giving. Therefore, I will make it clear on the check “For” line that this gift is a QCD. The charity must acknowledge the gift with the date the check was received, the amount, and the fact that we did not receive any benefits from giving the gift. This makes sense, as some would look for ways to “give” to a charity and then get something in return. That really isn’t a gift.

Tax reporting (From Fidelity)

“A QCD is reported as a normal distribution on IRS Form 1099-R for any non-Inherited IRAs. For Inherited IRAs or Inherited Roth IRAs, the QCD will be reported as a death distribution. Itemization is not required to make a QCD. While the QCD amount is not taxed, you may not then claim the distribution as a charitable tax deduction. A QCD is not subject to withholding. State tax rules may vary, so for guidance, consult a tax advisor. When making a QCD, you must receive the same type of acknowledgement of the donation that you would need to claim a deduction for a charitable contribution.”

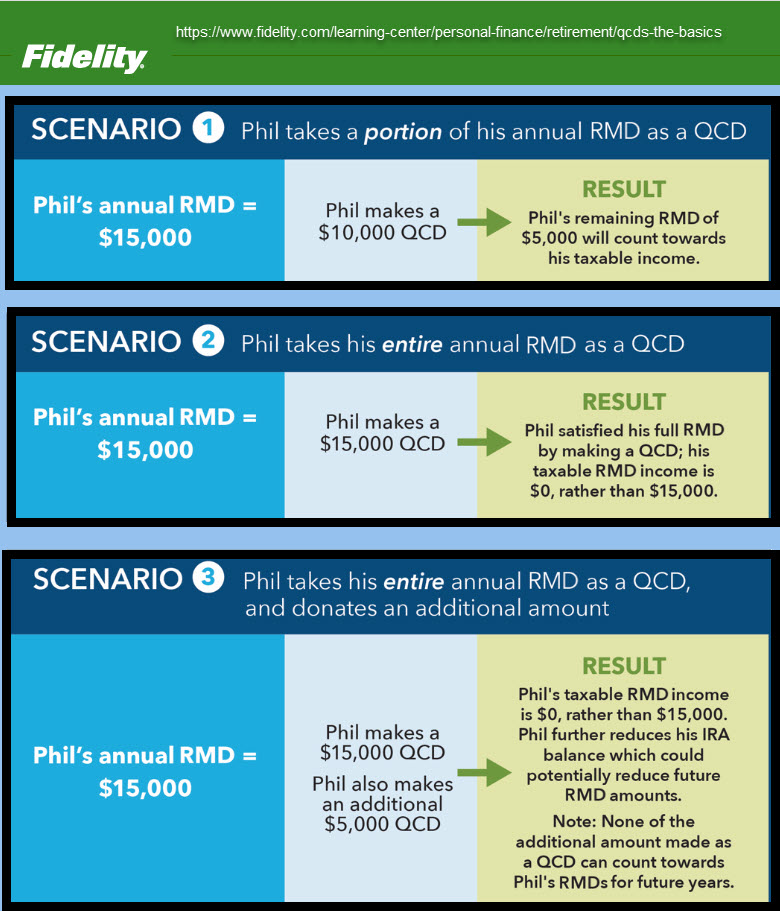

Three Examples from Fidelity

To help you understand the impact and importance of QCD’s, consider the three following scenarios. The first one shows what happens if only a portion of your RMD is covered by a QCD distribution. The second one reveals the benefit of giving away your entire RMD. You pay zero taxes and the charity will receive more because you did not have to pay income taxes.

The third scenario illustrates another of my objectives: keep reducing my IRA account balance so that future RMDs will be kept in check.

Conclusion

It pays to be aware of the opportunities to increase your charitable contributions to the ones you support. If you are involved with a charitable organization, perhaps you will want to educate your charity’s leadership as to this opportunity. It wouldn’t hurt to help your donors know about this option as well.

In future posts I hope to continue to provide insights with examples of what I did. I’m looking forward to giving even more of our cash away in 2024.