Do The Math

There are a number of things investors (those saving for retirement) don’t do. This includes not reading their monthly statements, not saving enough, and failing to budget. But there is another huge gap in the investor’s tendency to be woefully ignorant. Most adults know basic math. They can calculate percentages. For example, if you go to a nice sit-down restaurant, you will likely leave a tip. The tip may be 10% or 20%. If the total food order is $50, then you know you should probably leave a tip of $5 or $10.

When it comes to investing, most of the people I have helped in the past several years never did the expense ratio math. For example, if a mutual fund has an expense ratio of 0.85%, and they own $10,000 of the fund, then they are paying $85 per year for that fund. This continues year-after-year until they sell their shares.

When you are “only” paying $85, you probably don’t think it is a bad deal. After all, the “expert” is managing the fund. When you have $100,000 in that same fund, you are now paying $850 per year for the very same set of investments. Do you see the lunacy of that? In other words, when you only had $10,000 your cost was “lower”, but as you accumulated more shares, your cost for the very same fund management was considerably more.

Would You Pay $40 Per Gallon For Gasoline?

Let’s think about this. If you have a $5,000 car, and you pulled up to the pump, you find the price is $4 per gallon. But let’s say the law of fuel sales says that if you pull up to a pump with a car worth $50,000 (ten times as much), you have to pay $40 for the very same gallon of gas? I hope you would not. Rather, you would drive your $5K car to the station and fill the tank. Then you would drive home and siphon the gas from the $5K car and put it into the $50K car.

John Bogle’s Wisdom

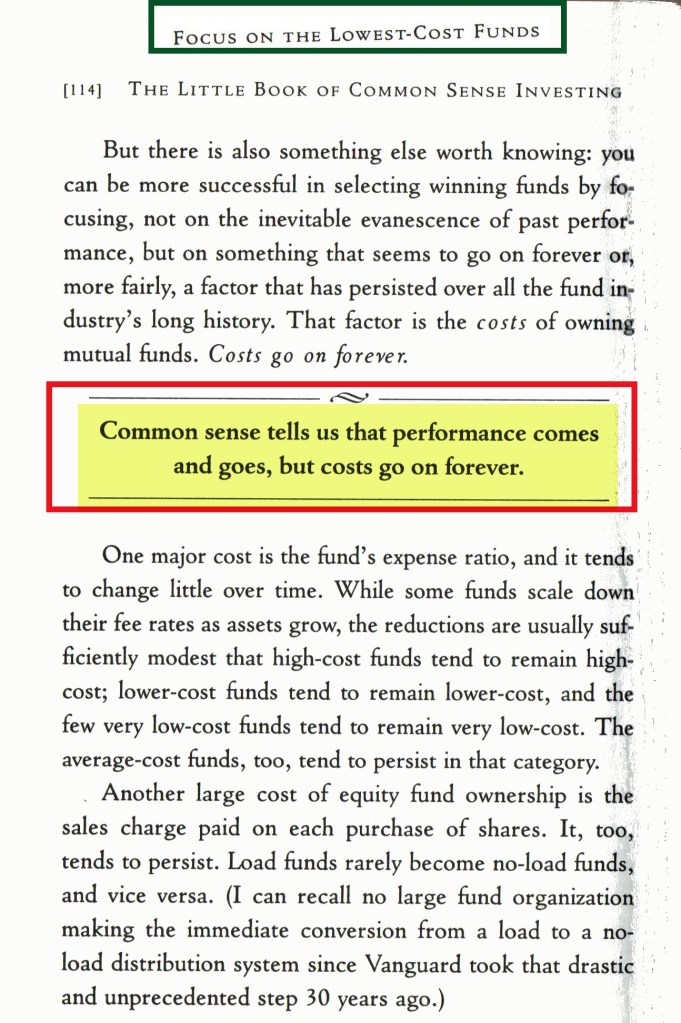

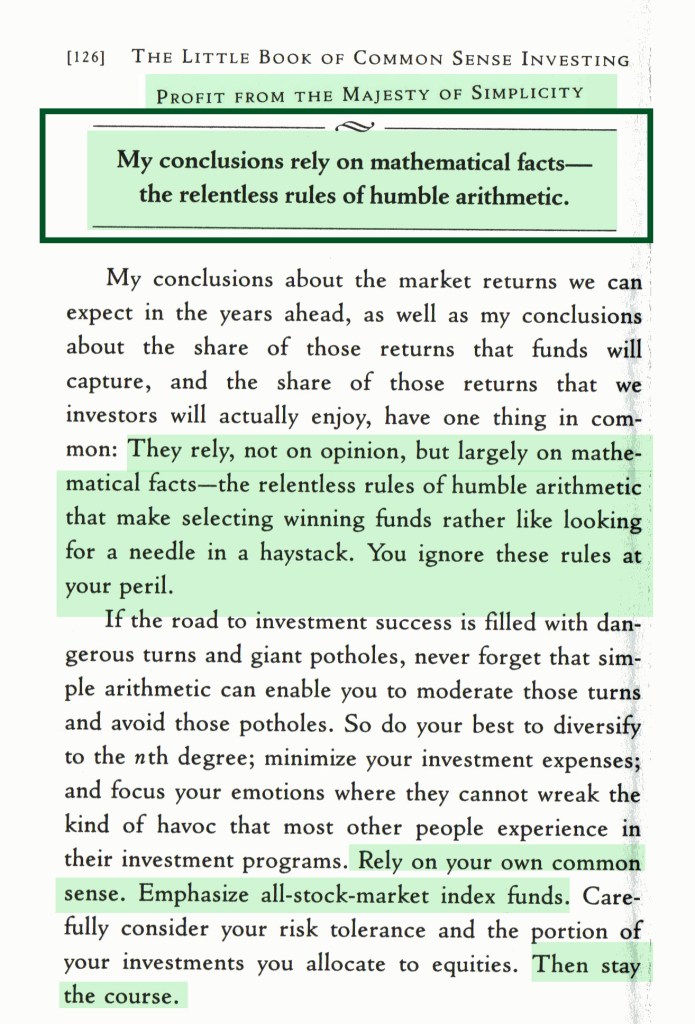

If you have never read John C. Bogle’s book, THE LITTLE BOOK OF COMMON SENSE INVESTING, then you need to do so. Here are two pages from the book to help you see why you should read it.

This is an important nugget: “Common sense tells us that performance comes and goes, but costs go on forever.” – John C. Bogle. OK, so if you have $100,000 in fund XYZXX, and the expense ratio is 0.85%, then you are not only paying $850 this year, but next year, and the year after that. In ten years you will give up at least $8,500 for fund management. This should look like an enemy to you. Furthermore, you pay the 0.85% whether the fund does well or does poorly. In other words, you can pay for bad fund performance.

Another worthwhile reminder is found on page 126 of his book. John says, “My conclusions rely on mathematical facts – the relentless rules of humble arithmetic.” He also says, “You ignore the rules at your peril.” This is why I look at the expense ratios, the dividend growth rates, and the ten-year total returns of an investment. You should too.

Why You Should Be Concerned

There is no reason to invest in high-cost investments unless you are 90-100% convinced that the expert managing the fund is smarter than just about everyone else. Let me tell you a secret: most funds do poorly. It can be difficult to find the needles in the haystack. I make this simple: buy quality low-cost ETFs and/or dividend growth stocks. Then just sit back and relax. The math is done.

Recommendation

Examine the expense ratios of the mutual funds and ETFs you own. Do the same for those you might want to buy. Then, ask yourself, “would I like to pay this dollar amount if I owned $100K of this fund?” If the answer is “no”, then explore the other funds that may have similar characteristics and a lower expense ratio.

Also, if your broker does not make the expense ratios of your investments a top priority, then you should consider finding a different broker.

then you hare not only paying

typo-then you hate …

LikeLiked by 1 person

Fixed. The word “hare” should have read “are.” Thanks for pointing this out. Sometimes I miss the obvious typos!

LikeLike

Fidelity has “gross expense ratio” and “net expense ratio.” Which should we focus on?

LikeLiked by 1 person

In the funds I have looked at, these are often the same. The gross expense ratio may be higher and it is the most that the fund might charge for their expenses. Sometimes they deduct from the gross to give a lower expense ratio. Of course, that is always at their discretion. In general, the net expense ratio is the reality.

LikeLike