Reviewing is Ubiquitous

Most of life contains some type of review. My dentist reviews my history and images of my teeth. The Ford dealer reviews the condition of the brakes, filters, tire wear, tire pressure, and fluid levels when I take our Escape in for an oil change. When I was working, Gene, Don, Mike, and Bruce (my superiors in three different businesses) reviewed my performance. I could name many more, but you get the idea.

One of the things most people don’t do, at least based on my experience helping dozens of family and friends, is review their investments. A review includes looking at asset types, sector weightings, allocations to fixed income, the expenses associated with their investments, diversification, asset growth, income (including dividends), and even overlap in mutual funds and ETFs their advisor has incorporated in their retirement accounts.

A New Series to Help You Review

This is the first in what I hope to write about how I review investment portfolios. My hope is that you will take the time to review your investments with a critical eye. Be like my primary care physician. Ask a lot of questions about your portfolio and your advisor. Read your statement to see what has happened in the past. Check all the vital organs with your investment stethoscope.

Although I have not created a list of the final topics, I have three or four churning in my mind and in a collection of notes I have created. I welcome your suggestions and questions. For example, there are multiple parts to the diversification piece of wise investing. Many think that because their advisor has included ten ETFs in their portfolio that they are diversified. Sadly, that is rarely the case. Let’s start with one aspect of diversification.

Market Capitalization for Diversification

One of the biggest flaws I frequently see in an investor’s retirement portfolio is a lack of true market capitalization diversification. The temptation is to buy large companies that are well-known and “safe” for the investor. This can happen with individual stocks, mutual funds, and with ETFs. One often used index is the go-to for many investors: the S&P 500 Index. This is a market-weighted index, which means that the top ten companies will make up a substantial portion of your total investment dollars. For example, VOO, the Vanguard S&P 500 ETF, is a good large cap ETF.

VOO has the same top ten holdings that every other S&P 500 index fund holds. The top ten make up 30% of the fund’s holdings. Understand there is risk in that investment mix. Yes, Apple, Microsoft, Amazon, Google, Meta, Berkshire Hathaway, and Tesla are all marvelous companies. However, notice that the top two make up over 14% of your total investment dollars. That is a high-risk approach to investing, especially if more than fifty percent of your total assets are in VOO.

Defining Some Market Cap Terms

The most common way to refer to market capitalization is by saying a company is either large-cap, mid-cap, or small-cap. There are other names, but we will stick with these for now.

The following definitions are taken from Fidelity Investment’s glossary:

Market Capitalization (Market Cap)–Market cap is a measurement that differentiates securities based on the size of the issuing company. It is calculated by multiplying the number of company shares outstanding by its average stock price.

Large Capitalization (Large Cap)–Stocks that when ranked largest to smallest by market cap generally represent the top 70% of the broader equity market’s capitalization.

Mid Capitalization (Mid Cap)–Stocks that when ranked largest to smallest by market cap generally represent the range of market caps falling between the top 70% (i.e., large cap) and the bottom 10% (i.e., small cap) of the broader equity market’s capitalization.

Small Capitalization (Small Cap)–Stocks that when ranked largest to smallest by market cap generally represent the bottom 10% of the broader equity market’s capitalization.

While large cap stocks are viewed as the “safe” way to invest, this sector does not always contain the best companies for the long-term investor. Therefore, it pays to diversify a portfolio into multiple parts of the market. This can be done with a total market ETF or mutual fund. For example, ETF ITOT (iShares Core S&P Total U.S. Stock Market ETF) has 3,296 holdings. This includes a wide array of companies. However, the top ten are the same top ten that are in VOO. Be careful.

ITOT has a decent track record, so allocating a portion of your portfolio to this type of investment might make sense. Bear in mind that there are other ways to gain exposure to multiple portions of the market. There are mid-cap and small-cap ETFs and mutual funds. Two examples are IJH (iShares Core S&P Mid-Cap ETF) and IJR (iShares Core S&P Small-Cap ETF.)

Reviewing My Allocations

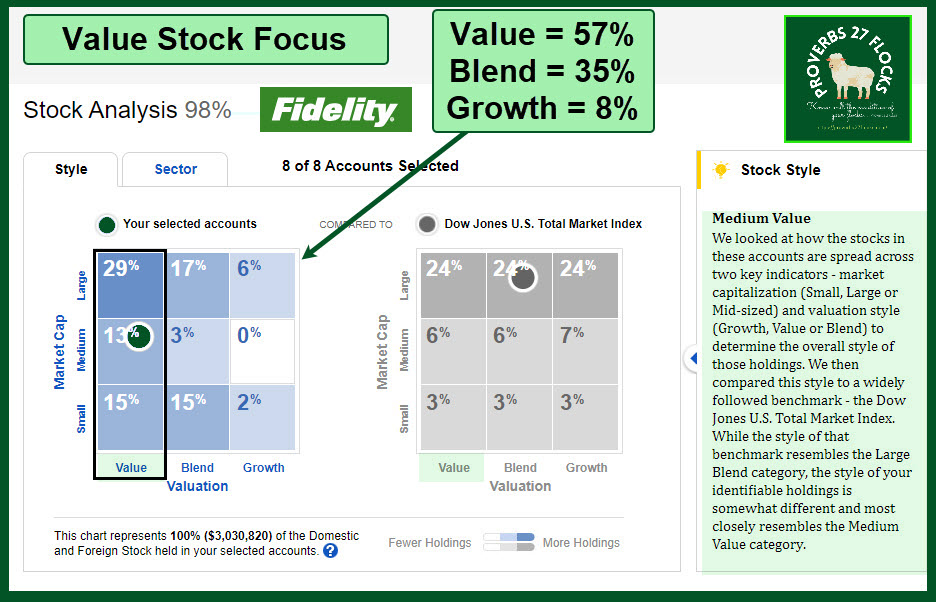

My first image might make some investment advisors very nervous. Notice that I have a significant portion of our stock and ETF investments focused on mid-cap and small-cap stocks. The reasons are elementary.

First of all, many of these companies pay a decent, sustainable, growing dividend. Secondly, smaller companies are often acquired by larger companies at a significantly higher price than the current market price. In addition, smaller companies have the potential to double in size much more quickly than most large-cap companies can ever grow. Notice that Fidelity says my portfolio (eight different accounts) is Medium Value.

My second image (value will be the topic of my next post. There is a good reason to determine if your portfolio is a growth portfolio, a value portfolio, or a blended portfolio. There are good reasons to be growth oriented, and equally good reasons to be a value-focused investor.

Full Disclosure

Cindie and I own sizable portions of investments like VYM, AVGO, MAIN, PFE, and ABBV. We do not own shares of any of the ETFs I mentioned above.

Here is a reminder of wisdom from thousands of years ago: “Know well the condition of your flocks, and give attention to your herds, for riches do not last forever; and does a crown endure to all generations?” Proverbs 27:23-24, English Standard Version

Do you see the diversification and the careful attention to the assets?

Portfolio Review: Great topic and very important in my opinion. I truly believe a lot of us don’t have a good handle on our true diversification, plus a plan or roadmap for our actual objectives. Thanks Wayne. Always looking forward to your posts.

LikeLike

Thankfully, those who use Fidelity Investments can use these same tools to get the big picture. There are other tools, and I plan to share them in future posts. Thanks for the encouraging comment, Warren. Wish we lived closer so that we could play another round of Chinese checkers.

LikeLike