Sources of Retirement Income

It seems most who are likely to retire from regular work at some point in their lives have not given serious thought to two different future realities. The first is not income-related but it might dictate what they can or might do if and when they retire. It may feel like ceasing to work is a good thing, but there is no plan for what will be done except not working. Rarely does failing to plan result in a good outcome.

The other reality that is ignored involves being able to pay the bills when an employer is no longer depositing cash in their checking account. They may have a foggy idea of their potential Social Security income if they have looked at their annual Social Security statement. They might also look at their 401(k) or 403(b) retirement account balance and wondered, “Is that enough?”

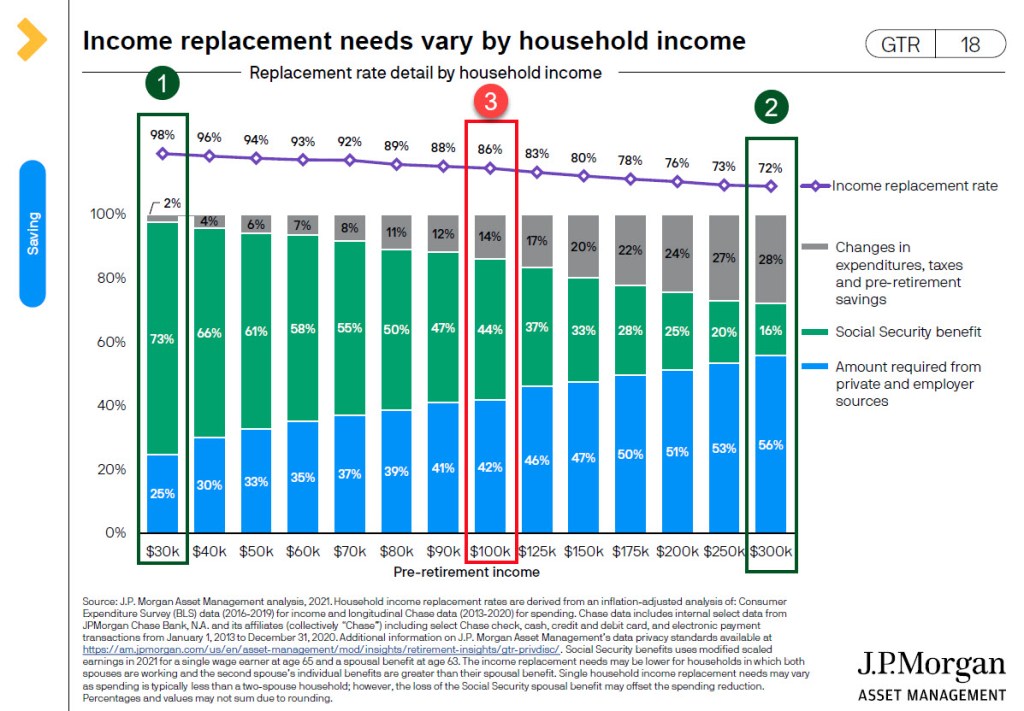

I recently saw a presentation from J.P.Morgan Asset Management with an interesting slide. The interesting thing about this slide, shown here, is that a family with $30,000 (1) in pre-retirement income will potentially receive 73% of their potential retirement income from Social Security, and only 25% from other sources, like savings.

At the other extreme, the family with ten times as much income can only expect to see 16% of their future income meeting their $300,000 (2) pre-retirement income lifestyle. Part of the change will also be a reduction in expenditures, taxes, and saving for retirement. Note you probably won’t be saving for retirement when you are retired. This however, presumes that sufficient savings have been built to fund $168,000 per year in income without lifestyle changes.

What About The Middle?

Let’s assume a more rational middle of $100,000 (3) in pre-retirement income. That would mean the family unit would receive about $44,000 (44%) of their retirement income from Social Security. While I won’t tell you what my pre-retirement annual income was, I can tell you that Cindie and I have a combined, after Medicare insurance payments, Social Security income of $43,608. According to this illustration, we would need to have $42,000 in income from other sources to live a lifestyle similar to what we had pre-retirement. Because we are mortgage-free and don’t spend money like a drunken sailor, a combined annual income of $86,000 is more than satisfactory to meet our needs.

However, because of the work I did creating an easy income approach to investing, our annual dividend income is more than $140,000 per year. This creates some wonderful opportunities for gifts to family and for charitable giving.

Agree Realty Corporation is Easy Income

ADC is one of our “Easy Income Strategy” holdings. First of all, the FFO (FWD) are $3.95 per share. FFO, by way of reminder is a REIT investment measurement known as Funds From Operations. The forward dividend rate is $2.92 with a yield of 4.41% and it pays a monthly dividend. ADC also has a decent market cap of $5.97B and a reasonable trading volume of over 600,000 shares per day. The current QUANT rating is a Buy at 4.07 on Seeking Alpha. We expect to receive $1,752 dollars in dividends from ADC in 2023.

Agree Realty Corporation is a publicly traded real estate investment trust primarily engaged in the acquisition and development of properties net leased to industry-leading retail tenants. As of September 30, 2020, the Company owned and operated a portfolio of 1,027 properties, located in 45 states and containing approximately 21.0 million square feet of gross leasable area. The Company’s common stock is listed on the New York Stock Exchange under the symbol “ADC”.

Notice in the illustration below the tenants of ADC. You might not be able to buy shares of Aldi, but you can own a piece of their real estate.

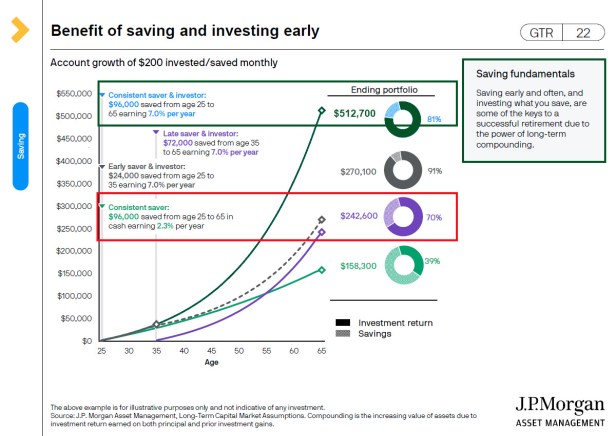

When To Get Started

There is no time like early adulthood to get started. However, if you are lagging in your planning and investing work, the best day to start is today. The following image is instructive.

Three Recommendations

1) If you haven’t already done so, you (and your spouse) should create an account with Social Security and look at the information regarding your potential Social Security income at full retirement age. 2) Evaluate your current savings and your current spending habits. 3) If you are married, begin to have a conversation with your spouse about what the future might look like in retirement. Do you have some ways to live a life that loves others and that redeems your time?

Perhaps we all would do well to reflect on what Jesus said in this regard. There was a fool in the New Testament parable who had a flawed, short-sighted, long-term plan.

“And he (Jesus) said to them, ‘Take care, and be on your guard against all covetousness, for one’s life does not consist in the abundance of his possessions.’ And he told them a parable, saying, ‘The land of a rich man produced plentifully, and he thought to himself, ‘What shall I do, for I have nowhere to store my crops?’ And he said, ‘I will do this: I will tear down my barns and build larger ones, and there I will store all my grain and my goods. And I will say to my soul, ‘Soul, you have ample goods laid up for many years; relax, eat, drink, be merry.’ But God said to him, ‘Fool! This night your soul is required of you, and the things you have prepared, whose will they be?’ So is the one who lays up treasure for himself and is not rich toward God.” Luke 12:15-21

Full Disclosure

Cindie and I own a combined total of 600 shares of ADC in our IRA and ROTH accounts. It is best to keep REITs in tax-deferred or ROTH IRA accounts to avoid or defer income taxes.

Seeking Alpha Agree Realty