A Great Question

Question from a reader: “I have a question about dividend reinvestment: what criteria do you use for auto reinvestment or selective reinvestment of dividends?”

Why I don’t automatically reinvest dividends.

There are several reasons to avoid, or at least scale back on automatic dividends. First of all, automatic dividend reinvestment is an all-or-nothing proposition. Let’s say, for example, that you own 1,500 shares of VYM. The annualized dividend rate for this ETF is $3.31 for the trailing twelve months. That will cause $4,965 to come in as a dividend during the next twelve months unless the dividend decreases for some reason. But perhaps I don’t want the entire $4,965 to be used to buy more VYM shares. I might want to buy some VYM and also add more SCHD and/or DGRO.

Secondly, VYM is trading for $106.10 per share. But the 52-week range of the price of the shares has been between $94.59 and $115.53. On March 23 the price per share was $100.82. If the dividend appeared in your account on March 23 (the dividend pay date), you paid $103.07 for the automatic reinvestment. However, if you had waited one day, you could have purchased shares for $101.70. The question I have to ask is, “do you want to buy shares at $103.77, or would you prefer to pay some lesser amount?” So a second reason is you want to buy at your price and at your timing.

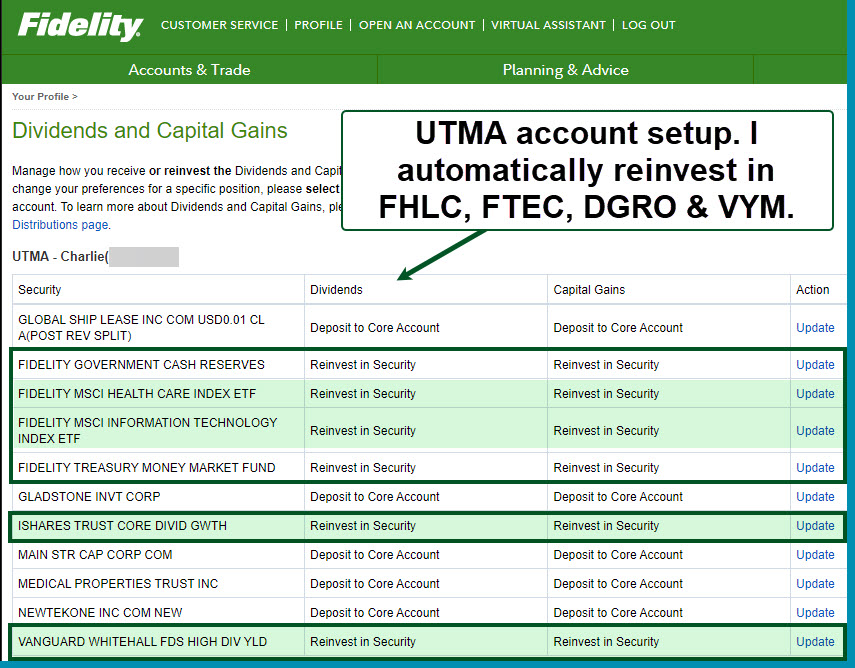

How do I know the price for the reinvestment of VYM? The answer is easy. The six UTMA accounts have dividend reinvestment set up for VYM dividends. This makes sense for their accounts, because the number of shares they hold does not result in enough dividend income to warrant trying to save a few dollars. The work is not worth the reward. However, most of their positions do not have automatic dividend reinvestment turned on.

Another reason to avoid automatic dividend reinvestment is if you are thinking about selling an investment. I own shares of IBM, and I don’t plan to hold them indefinitely. In fact, I own them because I trade covered call options on the shares. Covered call options require 100 share lots, so having additional shares purchased via automatic reinvestment doesn’t really help me with my options strategy. Even if I wasn’t trading options, I might not plan to hold IBM long enough to warrant buying more shares today.

Finally, there is no trading cost on Fidelity to buy shares of VYM, SCHD, or DGRO. In fact, there is no buy or sell cost for most stocks and ETFs. Therefore, there is no cost advantage associated with automatic reinvestment. You can buy one share or 100 shares and not pay a single dime.

The Cash Needs Require Prudent Plans

Cash is only king if you need cash for purchases. We keep less than 2% in cash most of the time. However, cash is best obtained from Social Security and dividends. It is not wise to look to gain cash in a timely and investment prudent manner by selling dividend growth investments. Therefore, dividends are income, and you should think about major purchases and charitable giving when you receive your dividends.

Why do I selectively reinvest dividends?

There are many good reasons to selectively determine how and when the dividends will be used. I will give you four of them.

1. The best way to buy an investment is to use a buy limit order. If VYM is currently trading at $106.10, I don’t want to buy the shares. So I will enter a buy limit order to buy at $105.75. Furthermore, I might only buy five shares today and then another five next week. There is no rush to buy on the dividend payment date.

2. VYM isn’t the only good dividend growth investment. If I received $1,240 on March 23 for my VYM shares. I might want to buy some shares of VYM, SCHD, and DGRO. In fact, I might only want to put 20% of the dividend to work in VYM shares, and 40% in SCHD and 40% in DGRO.

3. There are times when I want cash for a purchase or to pay our estimated Federal and Wisconsin income taxes. Our next tax payment is due April 18, so I will hold some cash for that purpose. Remember a key principle I use when investing – I don’t want to hold much cash. However, because dividends are arriving almost every day, some of them can be put to work on home improvement projects, charitable giving, tax payments, or a trip to visit family in West Virginia.

4. This sets the stage for retirement. Next year I will be 73, so I will have to start taking the RMD (Required Minimum Distribution.) The dividends from the investments in my traditional IRA will cover the RMD. Therefore, having automatic dividend reinvestment turned on is a poor strategy.

5. Choosing when to reinvest also has a powerful potential impact on future dividends. One of the reasons I invest like I do is to increase income faster than the rate of inflation. This is best done in a thoughtful way.

Recommendation

If the dollar amount of the dividend is less than $100, it may make sense to automatically reinvest, especially if you have limited time and interest in making dividend growth decisions. If you are investing in ETFs, then perhaps you might benefit from automatic dividend reinvestment. I think that is a lazy way to invest, but then I like to be more strategic in my investing buys and sells.

Full Disclosure

With the exception of some ETF positions in the UTMA accounts, none of our dividends are automatically reinvested. The selective reinvestment process is far more advantageous.

Some More Helpful Information

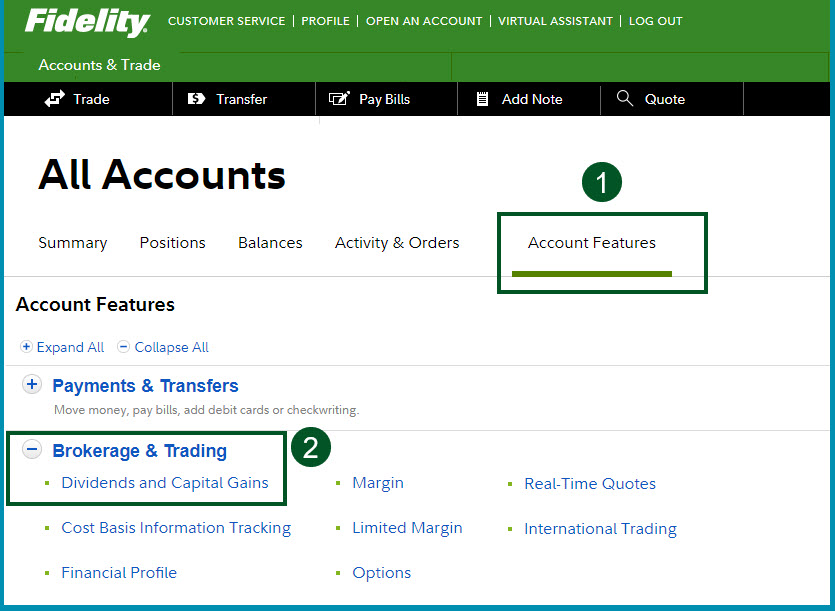

There are two links below. One is for Fidelity’s instructions. The second is from Five Cent Nickel. That post also discusses this topic.

I’ve just discovered your blog and have been absorbed in it for the last hour! Great information! I’m coming to this investing game rather late so am scrambling somewhat to catch up…I will keep reading as long as you keep writing!

LikeLike

Don’t hesitate to ask questions. If I don’t get too many I make a point of trying to answer those who have a question. As a result of the WSJ article it appears the activity on my blog is picking up, so I may not be as quick to respond to every inquiry. 🙂

LikeLike