Does Easy Income Really Work?

Many investment advisors give advice, but they don’t share their own personal results. Why is that? Because they really don’t have the same limitations on their own investing style. They have to act as a “fiduciary” for you (if that is how you pay them) and, therefore, they have to invest in assets many would deem safe. In other words, they allocate some of your money to bonds or money market funds, so as to help you sleep better in the short term. Perhaps they also invest that way for themselves.

Because I recommend a different approach, it is only fair for you to ask me to do a report card on my own retirement investment income. That is the purpose of today’s EIS update.

EIS Investment First Quarter Summary

March dividend income was $28,414.09. My best months are always March, June, September, and December. Other months have monthly payments and some quarterly dividends from a couple of investments. My average per month for the first three months of the year was $15K. That is far more than we need for living expenses. Social Security covers all of our living costs. I will continue to be 98-99% stocks and equity ETFs.

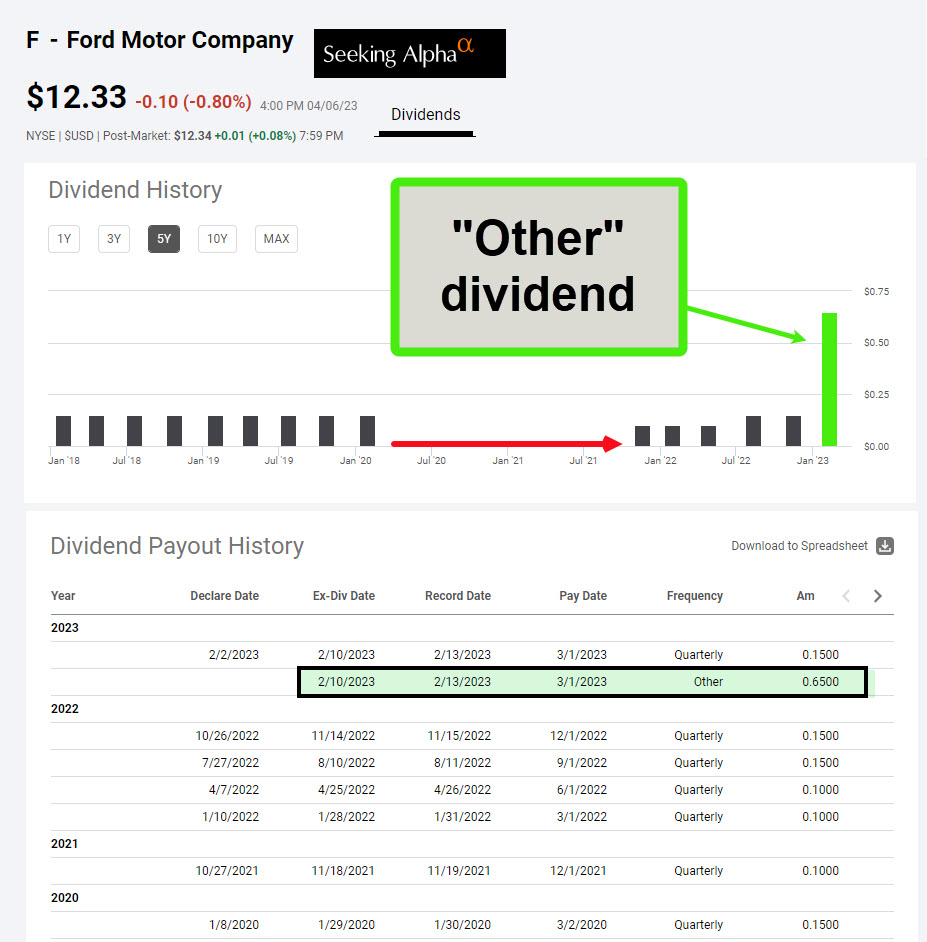

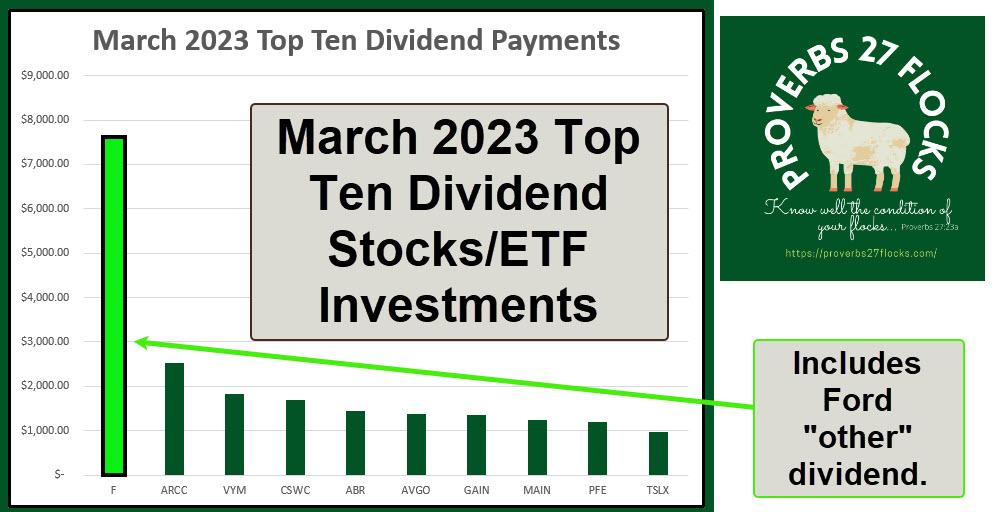

However, there is a word of caution about my results. Sometimes a company pays a special dividend, or a supplemental dividend, or a dividend classified as “other.” That is the case for March. The Ford Motor Company paid an extra $0.65 per share in March on top of the regular $0.15 quarterly dividend. That is not likely to be repeated this year. In fact, Ford just announced their next dividend is just the quarterly $0.15 per share.

To put this in perspective, I only expect to average $11,000-12,000 per month in 2023 dividends. Some months are less, and some months, like the four mentioned above, are far more.

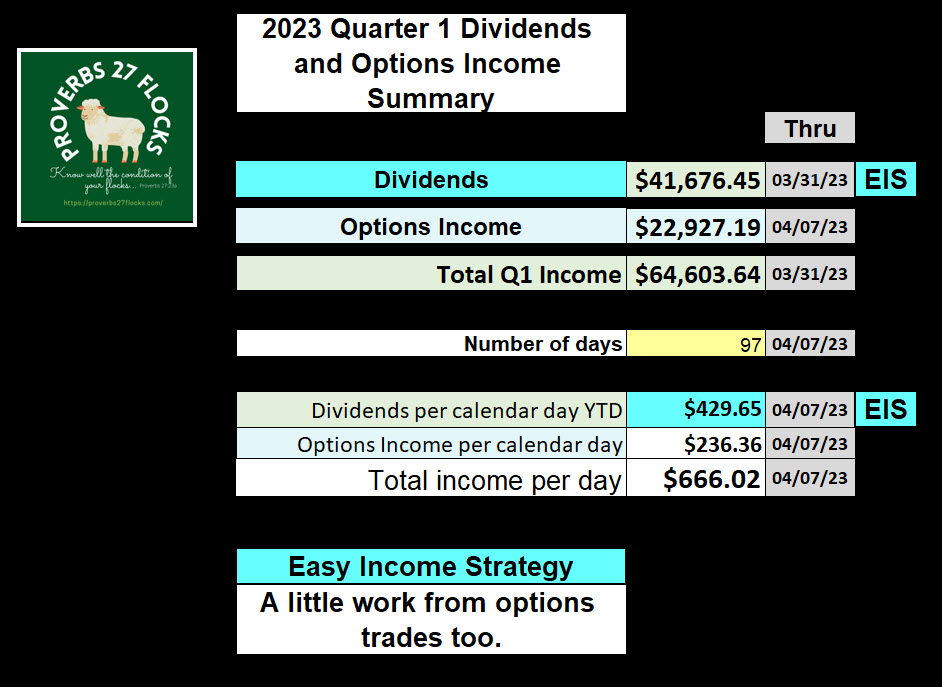

EIS Dividends and Options Q1 Summary

This table shows the results for both dividends, which is the “easy” part, and options trades, which requires more skill and just a tiny bit of work. Pay particular attention to the average income per day. The EIS income per day through April 7 is about $430. Some of this is taxable, some of it is tax-deferred, and some is tax-free. Because of Social Security, we can be very generous because we don’t need more pocket money.

March 2023 Dividends Top 10 Bar Chart

Sometimes it is best to look at the top ten. In this case, the total dividends from these are the main drivers of the success of the easy income strategy for the first quarter. Remember, however, that the Ford dividend included both a quarterly and a special one-time “other” dividend.

March 2023 Dividends Top 10 positions Table

For those who want to see the actual dollars for the top ten, here is the information in that format.

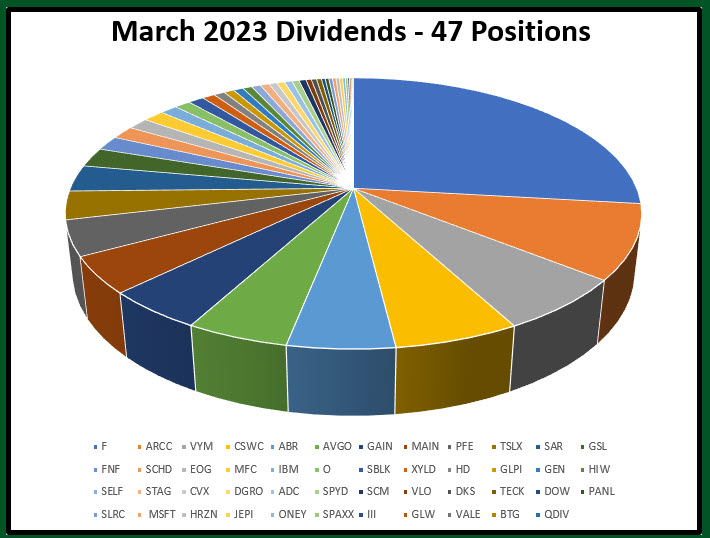

March 2023 Dividends 47 positions Pie Chart

In the end, any dividend-growth strategy should have a measure of meaningful diversification. This is best accomplished by most investors by focusing on dividend-growth ETFs like SCHD, DGRO, VYM, and comparable ETFs with low expenses and proven dividend growth. The downside to that strategy is that you probably won’t see dividends coming into your account as frequently as we have dividend income. One of the reasons I invest in BDCs, like GAIN and MAIN, is the predictable monthly income. Realty Income (O) is a REIT that also offers monthly dividend income.

The quantity of your positions is actually greater than the quantity of my different stock positions if you invest in low-cost ETFs and mutual funds. So it is not the quantity that matters. It is the quality.

What Should You Do?

Let me strongly suggest that you have a strategy. It does not have to be dividend growth, but I would say it should be anti-bond and anti-annuity. There are exceptions to this “rule”, as there are some who might benefit from tax-free bonds and others who might need an annuity for specific reasons. However, the vast majority of investors would do well to avoid or minimize putting money into annuities and bonds.

Full Disclosure

I have no plans to sell any of our investments.

Final Word

I think bonds are a poor long-term choice for most investors.

Wayne, there is no doubt your EIS results speak for themselves. Your willingness to share information and help others is a blessing. We are on a path that does follow your EIS with dividend paying stocks. We are seeing progress in our monthly dividends.

I trust you and your family will have blessed Easter weekend. Jesus is Alive!

LikeLiked by 1 person