Supply and Demand

When demand exceeds supply, a few things can happen. The normal thing is that the price of something will rise. If everyone wants eggs and there are few eggs, the sellers can demand more per dozen. Another thing that can happen with investments is that the yield can drop. As more investors buy an investment, the price of the shares rises. As that happens, the dividend yield drops. This doesn’t mean the dividend is reduced, it only means that dividend in relation to the price per share is less. Another result is that the item can stop appearing on the shelf. When toilet paper was in high demand during the Covid “pandemic”, some shelves were bare.

One of my readers, who is also one of my remote Zoom students, was trying to buy a 1-month CD yesterday using instructions I had provided. She sent me an email that said the following.

“I still can’t find the 1- and 2-month CDs… I looked around on the list of available CDs last night and found Camden Bank for 3 months as the earliest maturity rate. Now when I searched again, it’s nowhere in my sight on the screen and instead there is one from Keybank with a 4-month maturation level. Do I just need to call Fidelity and ask them to send me a list?”

My First Response

My first thought was that I had not clearly explained how to find the shorter-term CDs. So I went to Fidelity to get some screen shots to send her. What I discovered shocked me. There were no CDs with maturities less than four months. Why is this? I believe it is either because the demand for these CDs has exceeded the supply and the shelves are currently empty. It might also be a change in Fidelity’s overall fixed income offerings. Either way, this changes the investment landscape. What are the alternatives?

Best Choice with FDIC Insurance

The best choice this morning is a 4-month CD from Keybank with a current yield of 4.85%. There is no expense ratio, and this CD is FDIC insured. However, if you live in NY, OH, OR, or WA, you cannot buy this CD. That is called a Blue Sky Provision. “Due to individual state securities regulations (Blue Sky laws), this security may not be purchased in the following states or territories.” – Fidelity Investments

The other downside to this approach is that you have to be willing to have your money tied up for four months. For most cash, that is probably acceptable. However, there are some other possibilities.

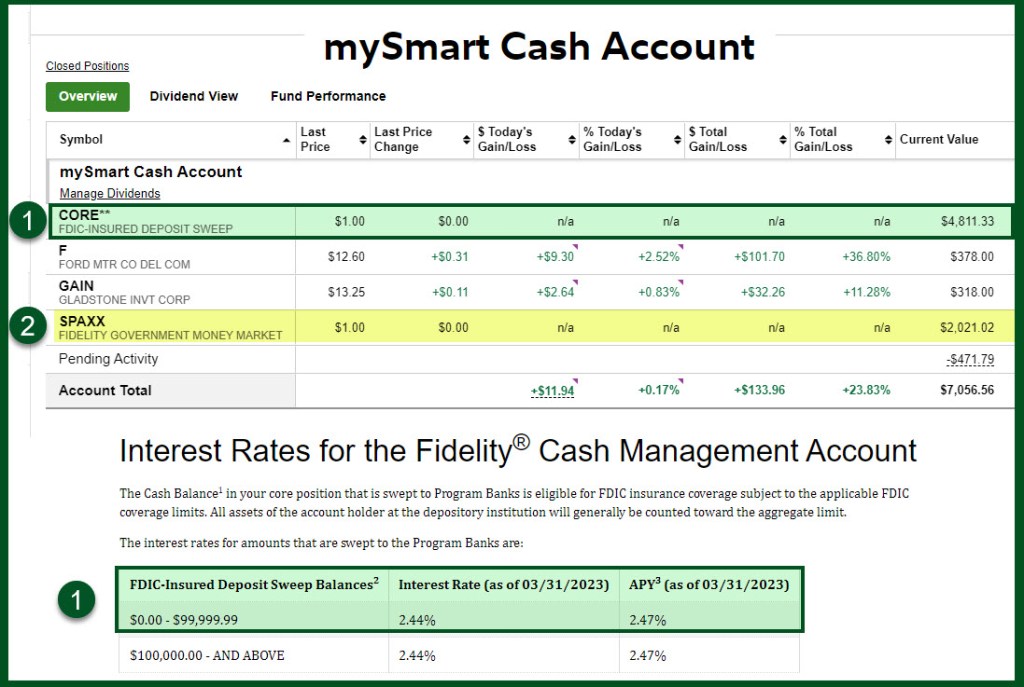

Our Fidelity Core Checking Account is FDIC Insured

Some of our cash at Fidelity rests in “FDIC INSURED DEPOSIT AT FIFTH THIRD BANK.” This bank is currently paying 2.44%. While that isn’t ideal, it is far better than our bank was and is paying us. In 2022 our bank gave us less than $1 for the entire year – which is an interest rate of 0.01%. What a joke that is. Actually, it is an insult to our intelligence.

Our mySmart checking account with Fidelity is infinitely better than our checking account with Wisconsin Bank and Trust. I have moved our checking activity to Fidelity and only keep $750 at the Wisconsin bank as an “emergency fund” so that I can go to the bank for cash from time-to-time. In the last twelve months, even though our average balance was over $7,000, WBT paid us less than one dollar in interest. That is ridiculous.

In March, because I moved our Social Security deposits to Fidelity, we made $16.63 in interest and $1.92 in a dividend from our 24 shares of GAIN in that account. So in 30 days I received what WBT would have given us in more than sixteen years. Furthermore, because our checking account balance is now $750, WBT paid us zero dollars in interest for March.

Money Market Funds

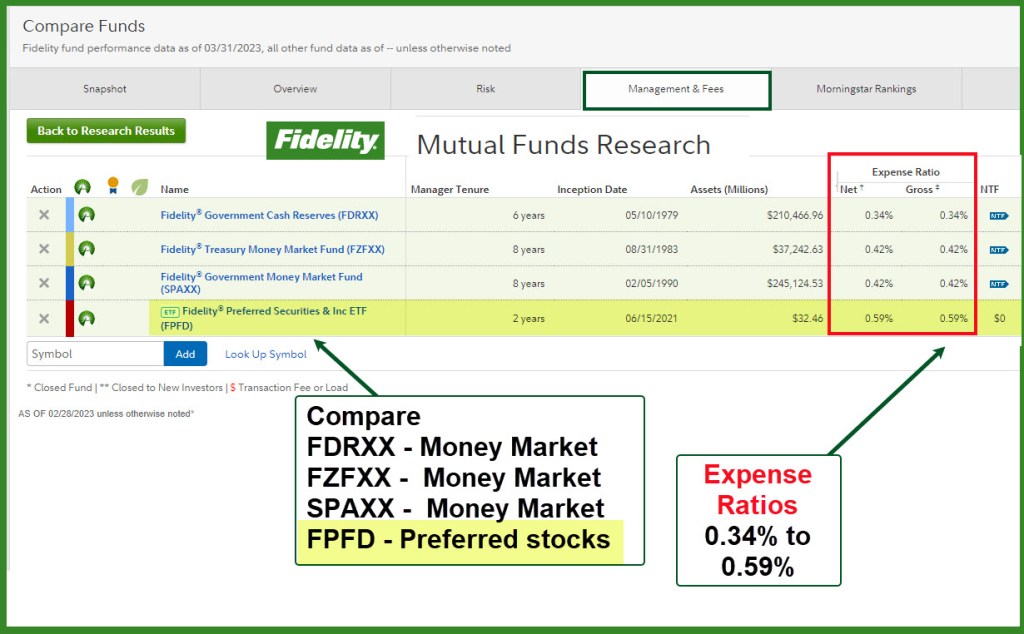

Money market funds are my go-to second alternative for our cash. There are some good money market funds at Fidelity, and I use three of them. The three are SPAXX, FDRXX, and FZFXX. All of them pay over 4.40% and all of them have an expense ratio between 0.34% and 0.42%. The net income, therefore, is just over 4.0%.

In our mySmart checking account I moved just over $2,000 to SPAXX as an “emergency fund.” It is highly likely that we won’t need that cash, so we may as well earn a higher interest rate. However, bear in mind that money market funds are not FDIC insured. Nevertheless, the actual risk of losing money (based on history) is very low. While there is some risk, it is nowhere near as risky as buying stocks.

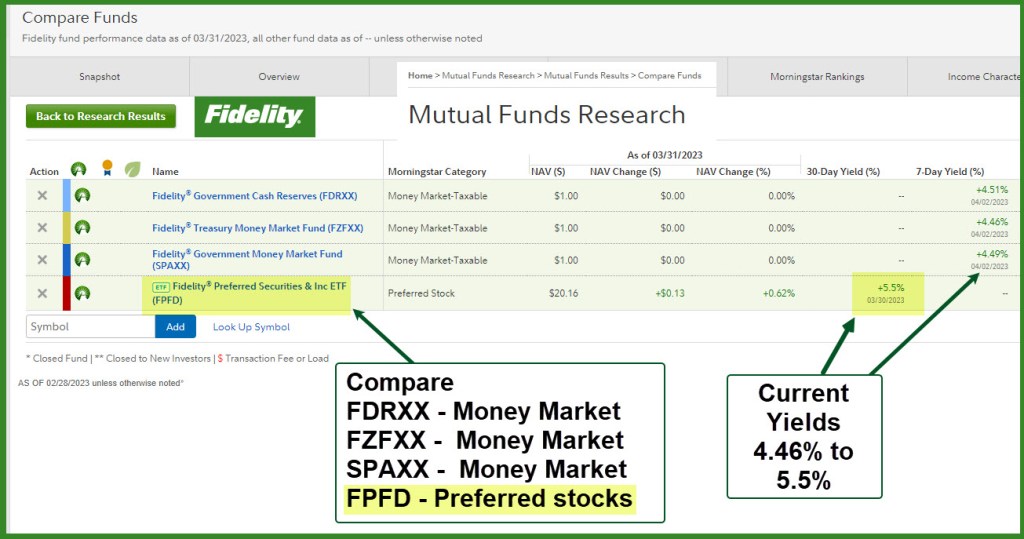

Preferred Stocks

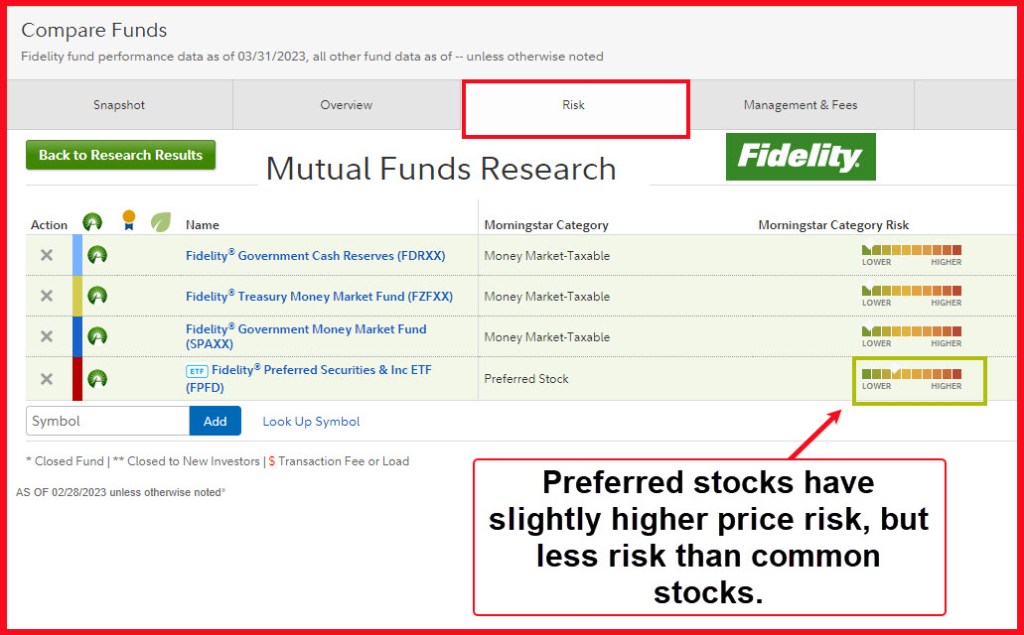

I won’t go into the details about preferred stocks, only to say that they are a bit safer than common stocks. They are not FDIC insured. They tend to have a higher yield than common stocks. One ETF that fits in this category is FPFD. The yield is 5.5% and the expense ratio is 0.59%. Therefore, you can get almost 5% on your money and get paid monthly like interest. However, this extra yield is probably not worth it. The risk is higher.

Another possibility is PFFV Global X Variable Rate Preferred ETF. This ETF has a yield of 6.56% and an expense ratio of 0.25%. However, please know that the value of this ETF has dropped over 12% in the last year, so this is not a safe investment. FPFD, in contrast has lost 7.71% in the last year. Both of them have a Seeking Alpha QUANT rating that is SELL.

Full Disclosure

Cindie and I own shares of FDRXX and SPAXX. Our grandchildren’s UTMA accounts hold shares of FZFXX and FDRXX.

Great information Wayne! We have enjoyed the last series of posts on Easy Income Strategy as we are working towards increasing our dividend totals. Since we switched over most of our savings into fidelity, we have bought CD’s on and off especially since the rates have been pretty good. I’m going to look into the Fidelity mySmart checking account, that sounds interesting. Is that now called Fidelity Cash Management? I can’t find anything called “MySmart”.

Thanks, Jackie

>

LikeLike

Hi Jackie, Yes, it looks like they rebranded the account, but the Fidelity Cash Management offering looks identical to what I am using. I opened the account a long time ago, but never really switched over to it until recently. I will be doing more of the Easy Income Strategy posts during the balance of the year, but they won’t be as frequent. Wayne

LikeLike

I see that Fidelity did replenish the CD’s for 1-month and 2-month, but with far fewer choices. I think the demand will continue to exceed the supply.

LikeLike