Unconsciously Overweight Ten Companies?

In January 2022 I talked about some of the dangers of index investing. I started by saying, “This week has been a glaring reminder that many ETFs and mutual funds have similar behaviors. If a fund manager tracks the S&P 500, the Dow Jones Industrial Average, or the NASDAQ, then their fund is likely to perform like the index they track.”

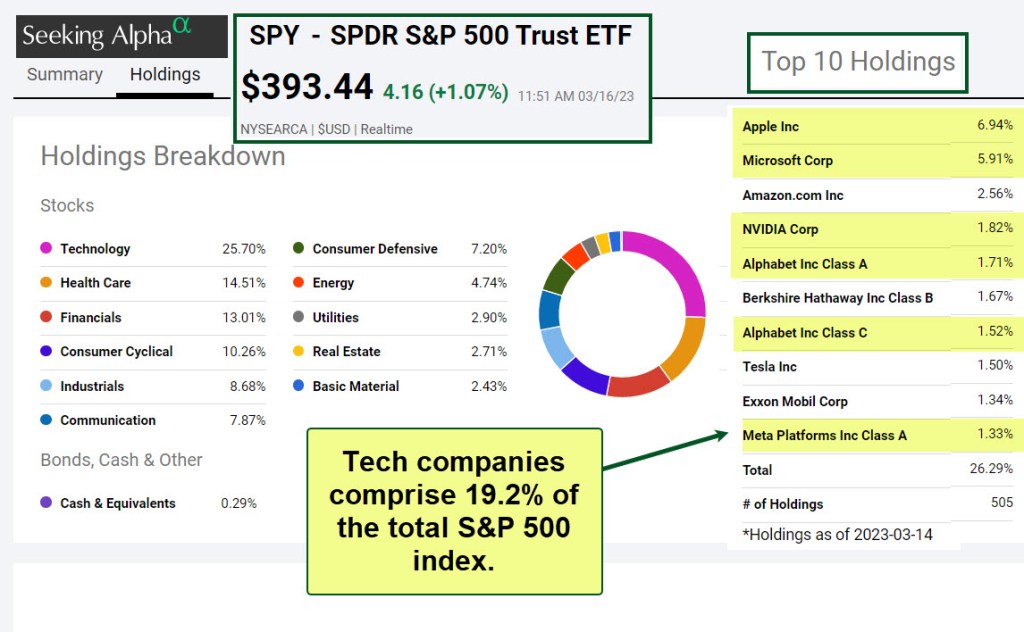

Wise investors always look at the top ten investments of every fund they select for their portfolio. If you neglect this step, it is likely you have some undesirable overlap and unhealthy concentration in the following stocks: Apple Inc, Microsoft Corp, Amazon.com Inc, NVIDIA Corp, Alphabet Inc Class A (Google), Berkshire Hathaway Inc Class B, Alphabet Inc Class C, Tesla Inc, Exxon Mobil Corp, and Meta Platforms Inc Class A (Facebook).

Two Meaningful Percentages

Two things should stand out to you when you see this list. The first is that six of the ten are in some way heavily focused on the world of technology. In fact, of the S&P 500 stocks, the six are at least 19.2% of the total top five hundred companies. That increases risk and may increase rewards.

The second thing you should see is that ten companies are only two percent of the total number of companies in the 500. Pause and think about that. You are saying, when you choose many index funds, to prefer a large percentage of your retirement savings in a select few companies.

Understanding Some Terms

One of my newer students asked some good questions this week. Recently, as she was reading John Bogle’s book, The Little Book of Common-Sense Investing. She sent me this question via email: “I wasn’t going to ask until I finished reading it, but something keeps sticking at me: what is the difference between an index fund, a mutual fund, and an ETF? They all seem like they are a basket of stocks that invest in the top businesses in the country. My only obvious observation is that mutual funds charge over 10x more in expense ratios than good ETFs. I looked into the Vanguard Index Fund (forgot the symbol, but it was one that closely resembled Bogle’s extolling in the book)…should I invest in an “index” fund over an ETF?”

My thanks to her for not being afraid to ask good questions! Here are my answers…

Question One: What is the difference between an index fund, a mutual fund, and an ETF?

First of all, either a mutual fund or an ETF can be and usually is an index fund. In fact, most mutual funds and ETFs are tied to an index. Some examples help (3 ETFs and three mutual funds) illustrate the wide variety of indices:

VYM – This ETF seeks to track the performance of the FTSE High Dividend Yield Index.

SCHD – This ETF seeks to track the performance of the Dow Jones U.S. Dividend 100 Index.

SPY – This ETF seeks to track the performance of the S&P 500 Index, by using full replication technique.

VHEHX – This mutual fund benchmarks the performance of its portfolio against the Barclays U.S. Corporate High Yield Bond Index and the High-Yield Corporate Composite Index.

VFSTX – This mutual fund benchmarks the performance of its portfolio against the Barclays U.S. 1-5 Year Credit Bond Index.

FBALX – This “balanced” mutual fund is a mix of stocks and bonds. Therefore, it seeks to benchmark the performance of its portfolio against the S&P 500 Index and the Fidelity Balanced Hybrid Composite Index comprising of 60% of the S&P 500 Index and 40% of the Bloomberg U.S. Aggregate Bond Index. I used to own shares of this mutual fund in the days when I didn’t understand bonds.

Question Two: Should I invest in an “index” fund over an ETF?

When you invest in an ETF, you are (usually) tracking an index. When you invest in a mutual fund, you are (usually) tracking an index. That is true 99% of the time. So my answer was, “I recommend you stick with ETFs.” Of course, the next questions should be “which ETFs should I buy?” and “why ETFs instead of mutual funds?”

Why ETFs instead of Mutual Funds?

A major difference between an ETF and a mutual fund is that you cannot know what a mutual fund is worth until the market closes each trading day. Let’s say there is a mutual fund that is very similar to an ETF. That is often true. Let’s further assume both are trading for $52 per share when you check prices at 10 AM. The reality is that the mutual fund is not trading at 10 AM. You can enter an order to buy 100 shares of the ETF for $50, after you notice that the share price is dropping. You also enter a similar order to buy 100 shares of the mutual fund, but you cannot specify the price you are willing to pay. The only price you see is yesterday’s price.

With an ETF you can pick a price you want to pay for the shares any time during the day. You can enter a buy limit order to offer to pay $50 per share rather than just accept whatever price is true at the market close.

Now let’s assume the price drops to $50 for the ETF and you get your 100 shares. Suddenly, some good news comes out before the market closes, and the price of the ETF shares rises to $52 for both the ETF and, at the market close, the mutual fund. You will pay $52 for your mutual fund shares.

Do you want to pay $5,000 for the ETF shares or $5,200 for the mutual fund shares if both are essentially tracking the same index? If you think paying an extra $200 is a good idea, then buy the mutual fund shares.

The same is also true when it comes time to sell your shares. With an ETF you can pick the sell price. With a mutual fund you only get the price at the market price at close.

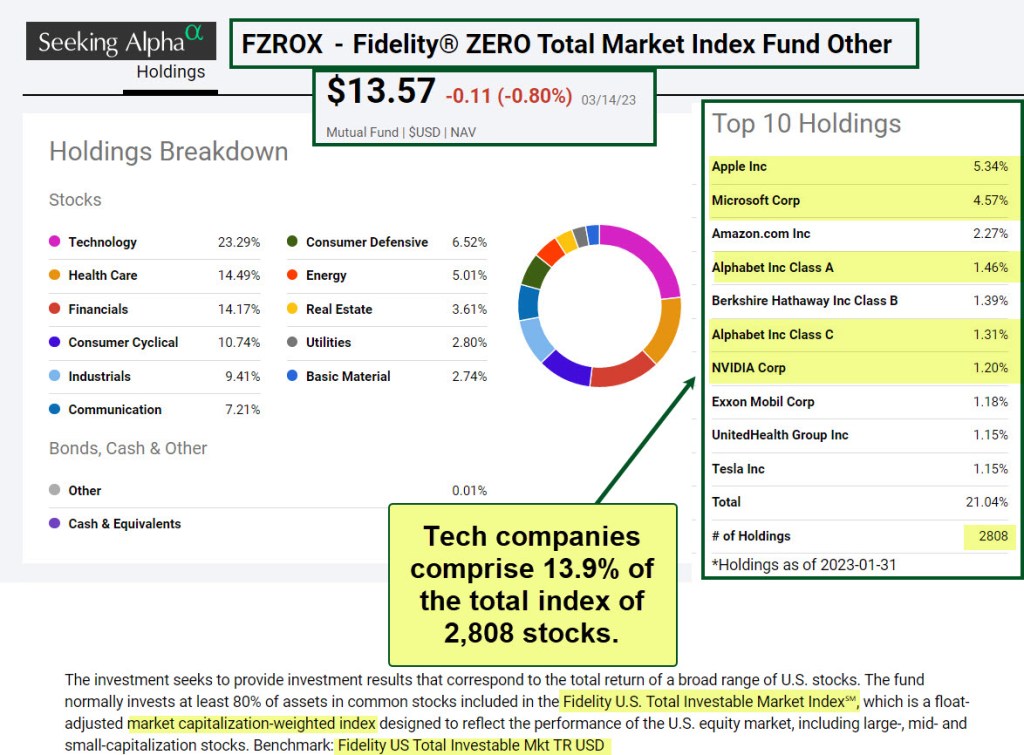

What about a Mutual Fund with Zero Expenses?

That may seem attractive on the surface. For example, the Fidelity ZERO Total Market Index Fund (FZROX) seems like a wonderful mutual fund. However, look at the top ten investments in the following illustration from Seeking Alpha.

You should notice that there are over 2,800 investments in FZROX so that seems like wonderful diversification. It includes large cap, mid-cap, and small-cap stocks. That is also desirable. But notice that five of the 2,800 stocks make up almost 14% of your total investment savings. Ouch!

Which ETFs Should I Buy?

The answer to that question has to be in response to your strategy. If you don’t have a strategy, then I don’t know how you can pick any investment. My strategy is dividend growth, so I look for ETFs that meet that criteria.

Full Disclosure

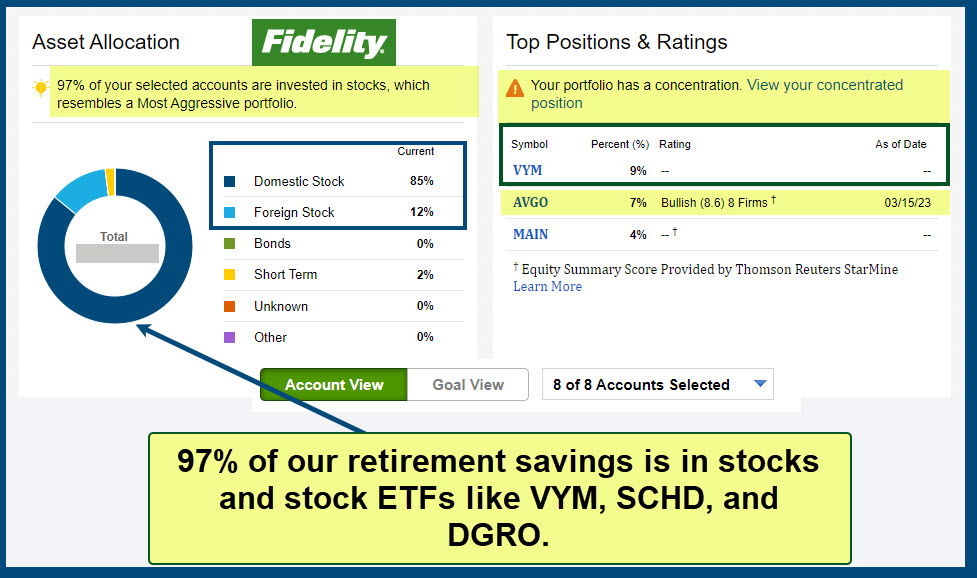

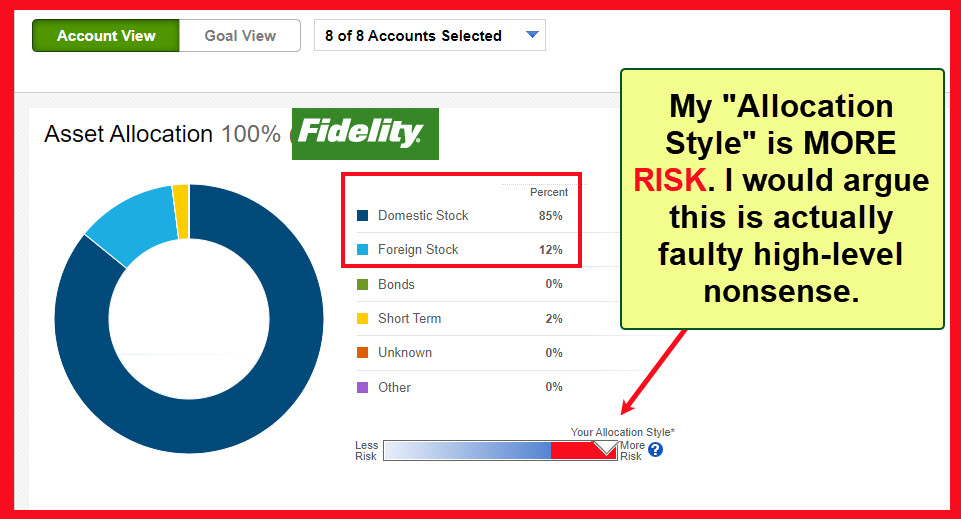

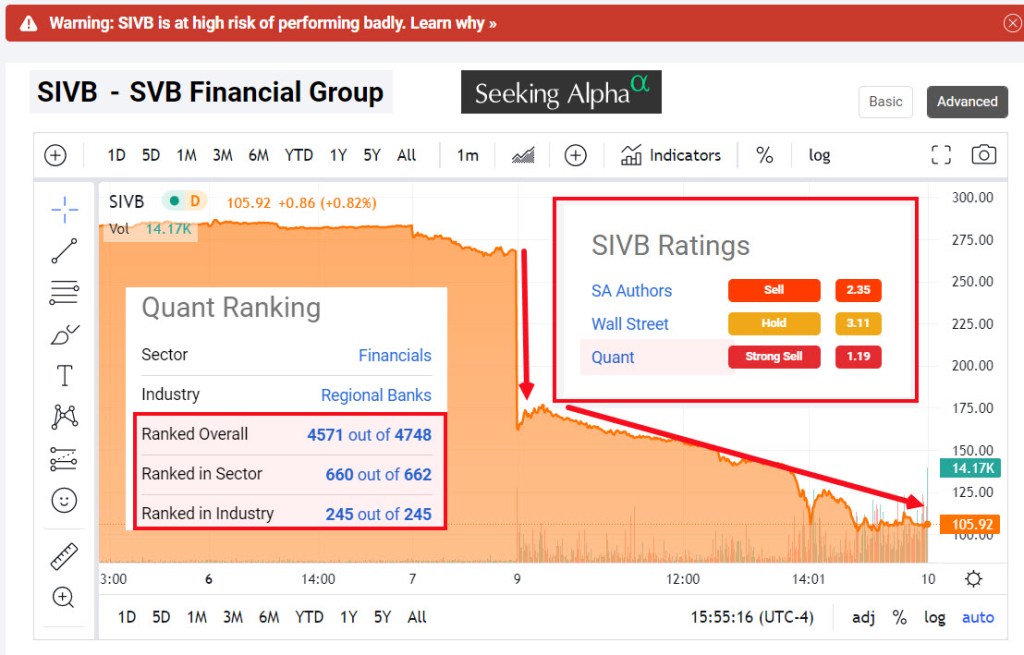

The following images help you understand how I invest. VYM is our largest dividend growth investment. It is an ETF that follows the FTSE High Dividend Yield Index. Our largest stock holding is AVGO. We are 97% stocks and stock ETFs. Fidelity’s automated rating says I am a “more risk” investor. Ask the managers of Silicon Valley Bank if bonds were a “safe” investment for their bank. They regret the safety they chose.