A Bank Provides Safety and Convenience

A bank is a financial business licensed to accept checking and savings deposits and make loans. However, many banks also provide other services including debit and credit cards, individual retirement accounts (IRAs), certificates of deposit (CDs), and safe deposit boxes. It is an easy place to get cash, although most people probably use ATMs for that purpose.

One piece of the safety net is FDIC insurance. “The Federal Deposit Insurance Corporation (FDIC) is an independent federal agency insuring deposits in U.S. banks and thrifts in the event of bank failures. The FDIC was created in 1933 to maintain public confidence and encourage stability in the financial system through the promotion of sound banking practices. As of 2020, the FDIC insures deposits up to $250,000 per depositor as long as the institution is a member firm. It is critical for consumers to confirm if their institution is FDIC insured.” – Investopedia

Why is a Bank a Thief?

It is prudent to have a savings account. However, banks do not provide sufficient interest for the money you give them. Remember, they are the borrower of your money. You are the lender. Lenders can decide what is a fair rate. If you don’t behave like a lender, the bank will treat you poorly.

I think a checking account and a savings account make sense. Although cash is rarely needed for most transactions in the 21st century, there are times when I go to Wisconsin Bank and Trust (WBT) to get cash for my wife or for gifts for our grandchildren. But most of the time I don’t think of our bank in a positive light. As interest rates have risen, the value of WBT’s services has been greatly diminished.

There was a time when our WBT checking account was paying a nice 3-4% on the checking account balance. However, that is a faint memory. Furthermore, the rates WBT offers for savings and CD deposits is laughable. As a result, our emergency funds were moved to an online bank a long time ago. Ally Bank currently pays 3.40% on our savings. These savings are for our emergency fund. WBT pays 0.01% on the cash in checking and essentially the same rate for comparable funds in their CD’s as well.

Beware of the Fees

If you open what WBT calls a “Signature Series Checking” account, the best you can expect is 0.25% interest. If you give them $100,000, the best you will get is $250 per year. You are the lender, and they are the borrower. They should be giving you at least $4,000 per year at 4.0% interest. But it gets worse. If you don’t keep at least $50,000 in the account, they will charge you, the lender, $9 per month or $108 per year to have their checking account. How do I know this? I read the very fine print on their website.

WBT Fine Print for Personal Account Fees

“Signature Series Checking Annual Percentage Yields (APY) are accurate as of 02/13/2023. APY tiers apply to the following balances: 0.00% APY on balances of $0.00 to $49,999.99. 0.15% APY on balances of $50,000.00 up to $149,999.99. 0.25% APY on balances of $150,000.00 up to $249,999.99. 0.25% APY on balances of $250,000.00 and above. Rates and terms may change after the account is opened. Keep minimum average daily balance of $50,000 or $100,000 in total relationship balance for the cycle month to avoid $9 monthly maintenance fee. Signature Series Checking is a Consumer Checking account. $50,000 minimum balance required to obtain APY.” – Source: Wisconsin Bank and Trust

Recommendations

In the last couple of weeks I have had conversations with friends about the poor results they are getting from storing their excess cash at their bank. Even if you are saving for a long-term purchase like a car or a home purchase, you should not settle for less than three percent on any of you money.

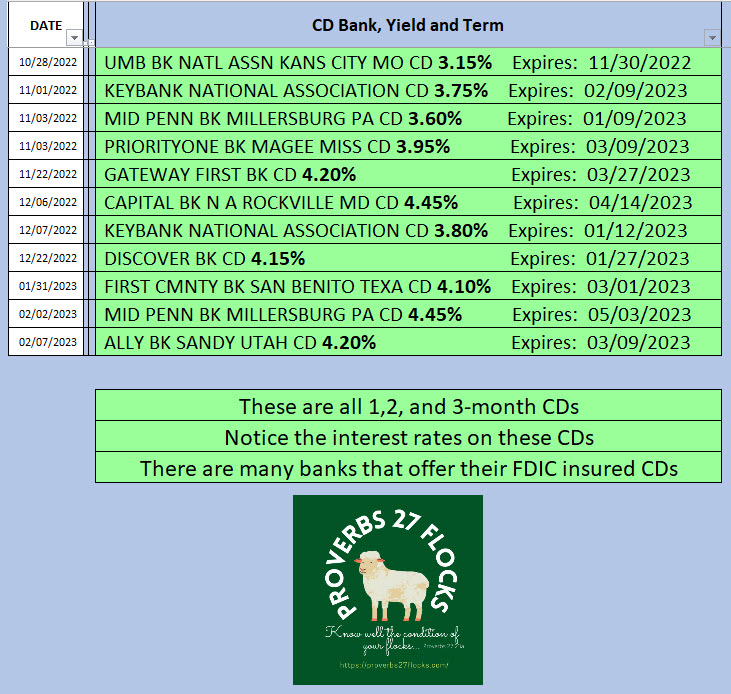

It is best for most prudent savers to move their money to either an online bank and/or to a place like Fidelity Investments. I have been buying CD’s for Cindie with some of her cash. Here is an example of the CD’s she has.

We will be keeping our WBT checking account. However, I have already moved our Social Security Direct Deposit to our Fidelity cash account. That account comes with checks. It is very easy to do electronic funds transfers between Fidelity and WBT. The good news is that the money that was earning 0.01% will now earn at least 3%.

Links

We did the same with our emergency cash.

LikeLiked by 1 person