Is Popular Widely-Held Thinking Wise?

Every time I state my thinking about investing or specific investments, I run the risk of giving bad advice. Most investment advisors would call my investment approach “overly aggressive” at best, and “basically crazy and reckless” at worst. The popular model says the older you are, the more cautious and conservative your investment mix should be. Most models say that a person my age should have an asset allocation of 50% stocks and 50% “safe” money in US bonds, international bonds, and short-term treasuries.

I steer our investment ship differently than that. Our accounts have an allocation of stocks that is usually about 98% stocks with the balance in cash and CDs. If you listen to most advisors, they will want you to behave like most retirement target date funds. That just means you add more-and-more bonds and hold fewer-and-fewer stocks as you get older-and-older. This is deemed more “safe.”

This advice is true until it isn’t. The two demons that upset the model are inflation and a rather healthy bear market. This, combined with dramatically increasing interest rates, supply chain woes, federal policies and rampant government spending made the “safe” investments rather risky.

My Normal Advice

I generally give advice that I follow myself. I eat my own cooking when it comes to investing. Therefore, when I suggest that dividend-growth investing is a good path for the long-term investor, and that bond allocations should be kept to a minimum, I follow my own recipe. While I cannot predict the future, I do believe a slow-and-steady growth plan is the best way to invest for the long-term.

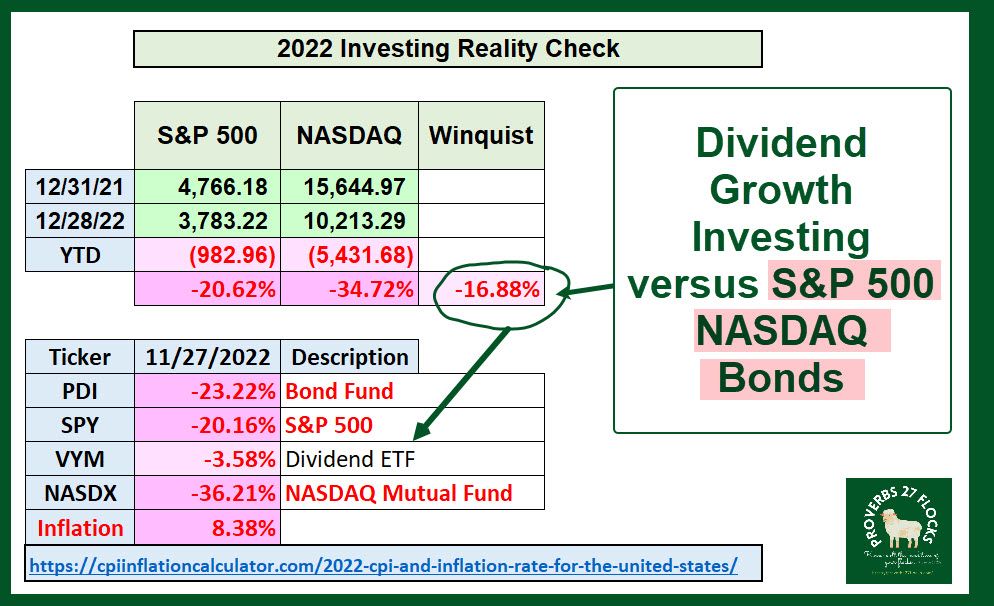

Comparing the Winquist 2022 YTD Returns with…

2022 is almost over. There could be a significant sell-off today or tomorrow, but the investing year ends when the market closes on Friday afternoon. I don’t believe it is too soon to take a look at the results for 2022. Here are our results compared with the S&P 500, the NASDAQ and some specific investments. I will keep my comments to a minimum.

If I had invested in bonds, our YTD returns would have been far worse than -16.88%. PDI, a bond ETF, is down 23.22% and ETF BND (shown later) is down 14.31%. But those who chose growth investing are really feeling the pain. Growth investing is fun until it isn’t.

Notice, however, that my favorite ETF (VYM) is only down 3.58% YTD. There is a reason for this. Dividend-growth investors buy investments for dividends that grow. So they are less inclined to panic when everyone else is petrified. I pity the investors who loaded up on the top ten investments in the NASDAQ and the S&P 500. All the while inflation kept gnawing away at the buying power of the dollar.

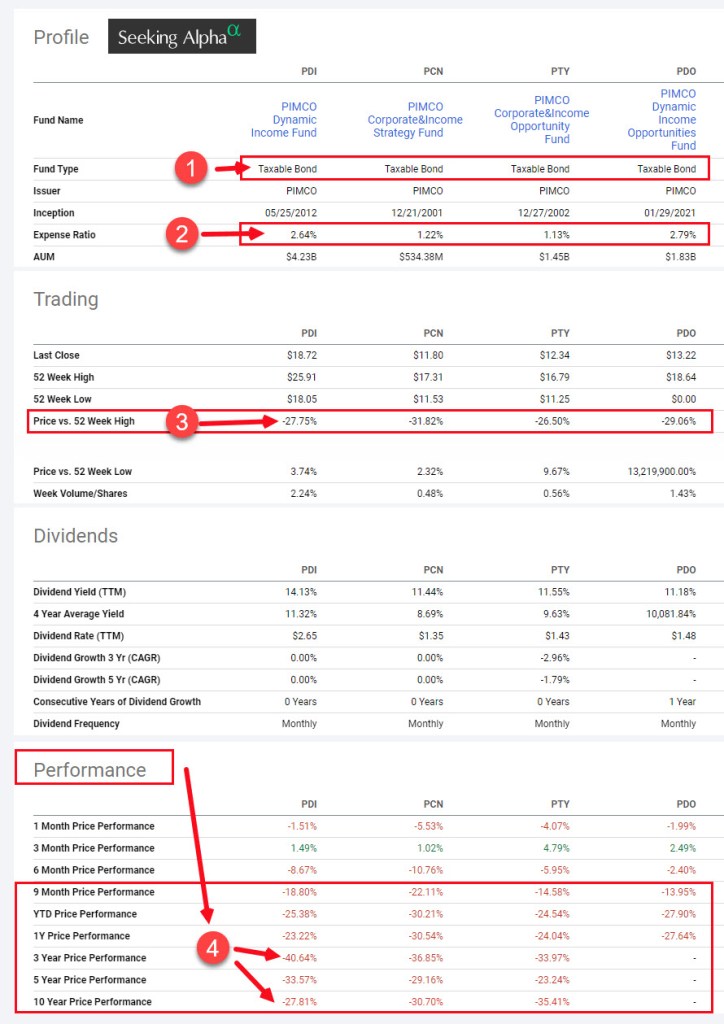

Bond Funds

Here are the results of two popular bond funds: PDI and BND. The protection of bonds is a mirage. The returns were horrible unless you compare them to the NASDAQ. Take a look at the third image, especially the ten-year returns. Then ask yourself, “how safe are bonds?” Of course, bond holders did receive income, but that income was obliterated by inflation. PIMCO’s returns stink – so hold your nose.

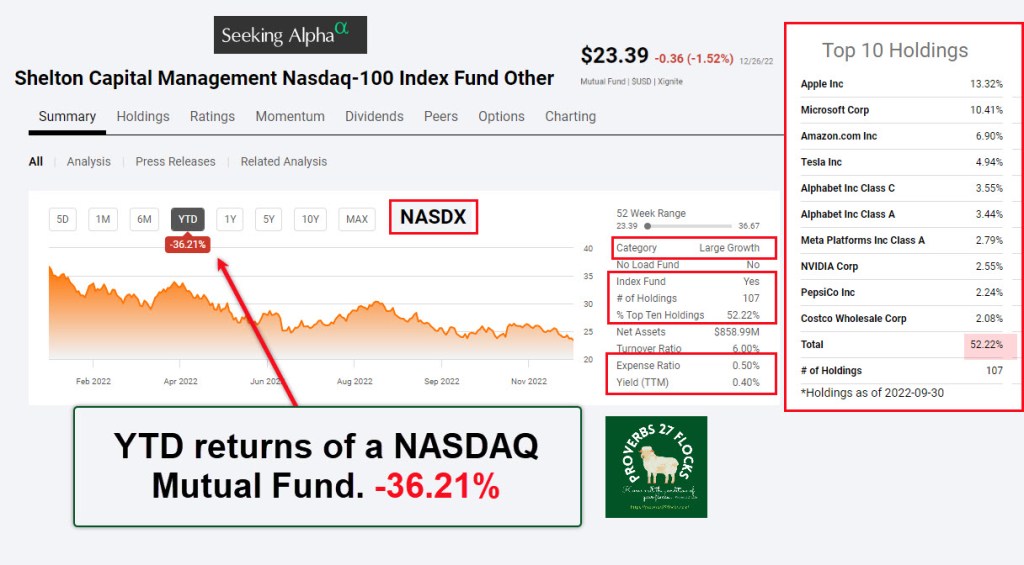

The NASDAQ

To say it was a bad year is not an understatement. I guess the only consolation is that “it could have been worse.”

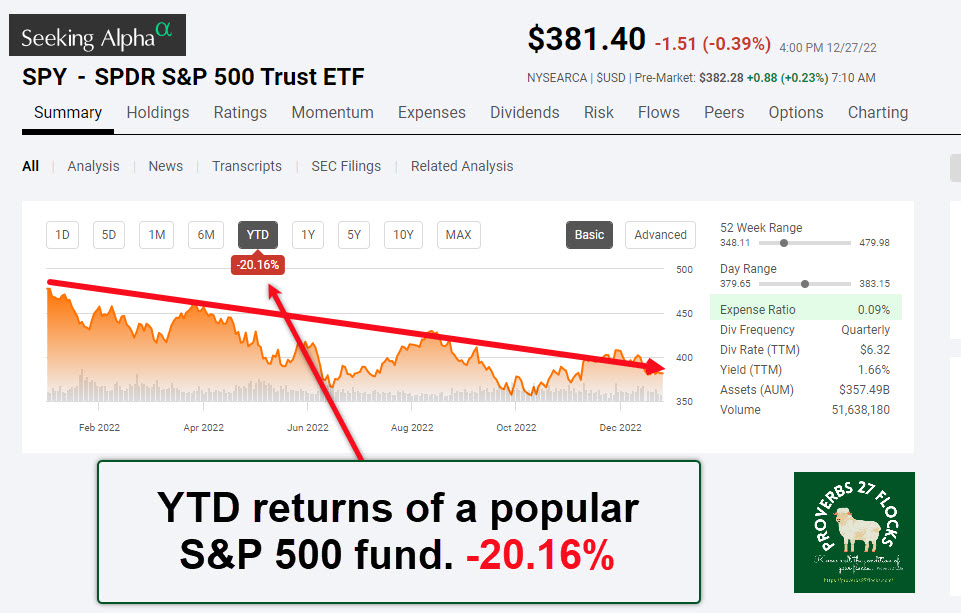

The SPY S&P 500 ETF

This is the backbone of many investor’s portfolios. In good years, this can be good. I’m not opposed to having an allocation in the S&P 500 via an ETF or index mutual fund. However, I really don’t like the top-heavy nature of that index because it is cap-weighted.

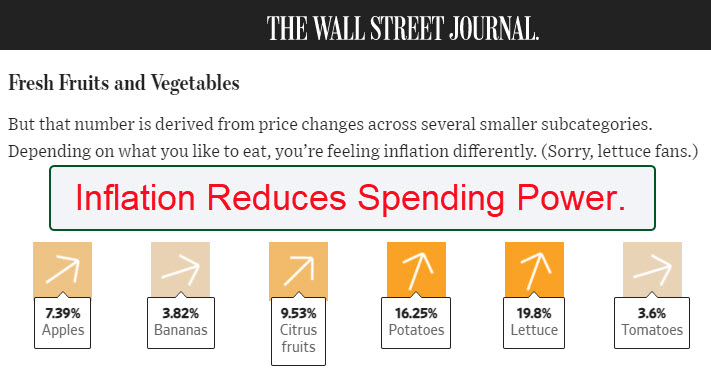

Inflation in the Grocery Aisles

My wife is glad that I buy the groceries. I know what eggs cost last year, what bacon cost last year, and what butter cost last year. In fact, I am fairly confident that our grocery costs have gone up by at least 20% in the last twelve months. Restaurant meals have also become more costly, as has gasoline, our electric bill, and most of the things we buy on Amazon. If you think inflation will go away, all I can say is “I hope you are right.” Sadly, I don’t think it will or can based on the bigger economic issues created by a federal government determined to spend us into prosperity.

As a result, I don’t want to hold investments that are going to be fighting a losing battle against inflation. Therefore, I will continue to recommend that investors think more carefully about their stock and ETF investments and steer them away from bonds or at least continue to caution them about the serious risks associated with bonds.

Summary Recommendation

Don’t follow my advice unless you understand the things I recommend. Although VYM has been a winner in 2022 in relative terms, it may not shoot up as fast as Apple, Microsoft, Amazon or Tesla in 2023. I prefer to be the tortoise in this regard. I want slow-and-steady growth, with rational income growth all along the investing journey.

At the very least, ask your investment advisor to show why you should be following their advice. Will they share the results of their own personal investing success? Are they eating the cooking they are serving to you? Did your investment advisor give you returns that beat the S&P 500? If not, why not? You are paying them for their expertise, so you should expect expert returns.

Thank you for sharing openly so much of what you have learned Wayne.

LikeLiked by 1 person