Finding Dividend Growth Stocks

In Part 9 I suggested some ETFs to consider for dividend growth. Most of my readers are best sticking with low-cost ETFs or index mutual funds with low expense ratios. You should have exposure to large-cap, mid-cap, and small-cap stocks in multiple business sectors. When you have less than $100,000 in assets, you probably don’t want to get too focused on just a few stocks. However, there are some good reasons for venturing into some stocks as a part of your overall portfolio once you reach $100K in assets. There are a couple of reasons I might suggest for the more serious investor who really wants to see the potential for better than average income growth. Three reasons are: returns, dividend growth, and the ability to trade options.

Stocks Versus ETFs – Who Wins with Overall Returns?

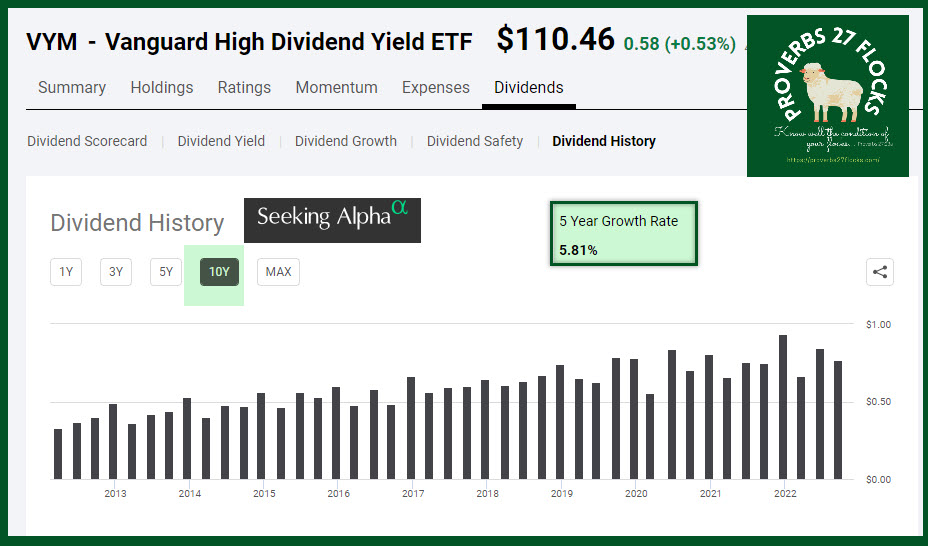

While an ETF is far more diversified than a single equity like Chevron, 3M, Pfizer, Coca-Cola, or Ford, diversification can also drag down returns during bull markets. VYM, for example, has weathered the bear market well. I just checked the YTD results and VYM is only down -1.94%. However, my shares of ABBV (AbbVie Inc.), are up 22.57% YTD. Of course, there is more risk in owning one health care stock than there is in owning VYM which holds 445 positions. Furthermore, VYM has PFE, ABBV, MRK, JNJ, and LLY (health care stocks) in the top ten. So I get more health care companies for the same $10,000 investment than I would get from buying $10,000 worth of ABBV.

On top of that, VYM puts you in several different sectors including: Financials (20.33%), Health Care (16.26%), Consumer Defensive (13.70%), Energy (11.22%), Industrials (10.42%, and Technology (7.44%). So clearly, having multi-sector exposure can reduce overall long-term risk.

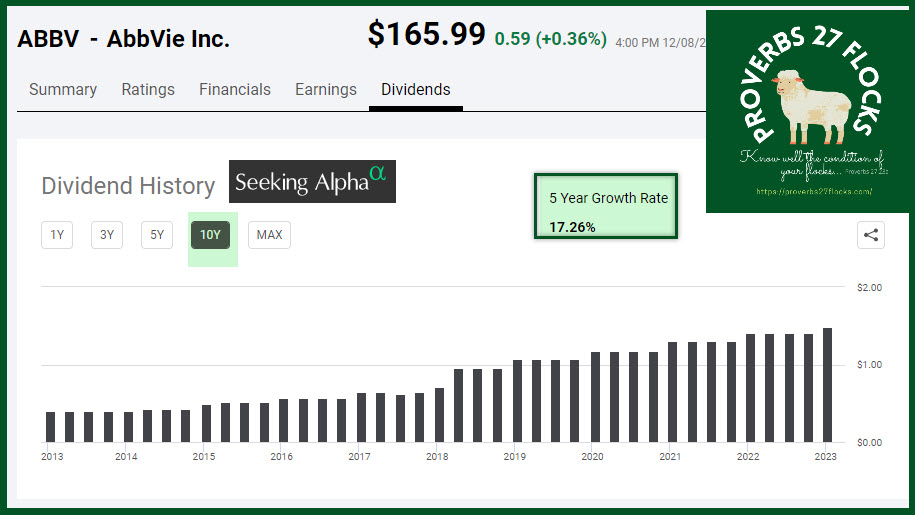

However, VYM’s 10-year returns are 121%. That isn’t bad until you realize ABBV’s 10-year returns are 403%. The novice investor would just look at the growth returns and put their entire $100K portfolio in ABBV, hoping for another ten years of spectacular returns. That is the way of folly.

The point, however, is that diversification does not always help total returns. In a pool of 445 positions, you have some positions like ABBV that have done very well, and you have investments like CVX (Chevron) in the top ten that have ten-year returns of 60.95%. When you own ETFs and mutual funds, most of the time you are buying some mix of investments that reduces potential risk, but also reduces potential upside.

Stocks Versus ETFs – Who Wins with Dividend Growth and Yield?

ABBV has a yield of 3.58% while VYM yields 2.93%. Why the difference? Because VYM has a blend of various stocks with various dividend yields. To make the contrast even more vivid, ABBV has 5-year dividend growth that far exceeds that of VYM as the two following images illustrate. However, the novice investor must be cautioned once again. It is far more realistic to expect that ABBV, during times of financial hardship might suspend or hold their dividend steady. The future is uncertain due to government regulation, competition, and various lawsuits that could damage a single company in a way that is very undesirable.

Bear in mind that there is no good reason to compare VYM with ABBV other than to illustrate the point. It isn’t comparing apples with apples. It might be better to compare VYM with SCHD and then look at ABBV. SCHD has a better yield of 3.37%, a ten-year growth rate of 167%, and a 5-year dividend growth rate of 13.74%. That is one of the reasons I hold VYM, SCHD, and 500 shares of ABBV.

What Are Some Easy Ways to Find Good Stocks?

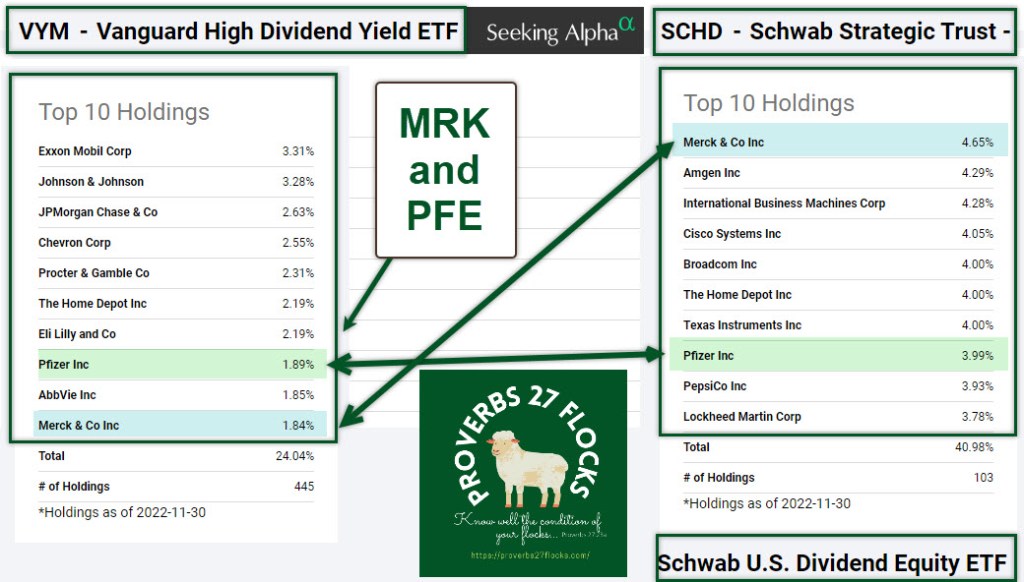

This doesn’t have to be hard. One way is to use Seeking Alpha and look at VYM and SCHD. Both have dividend growth. Both have a top ten list. Here, by way of example, are the two side-by-side.

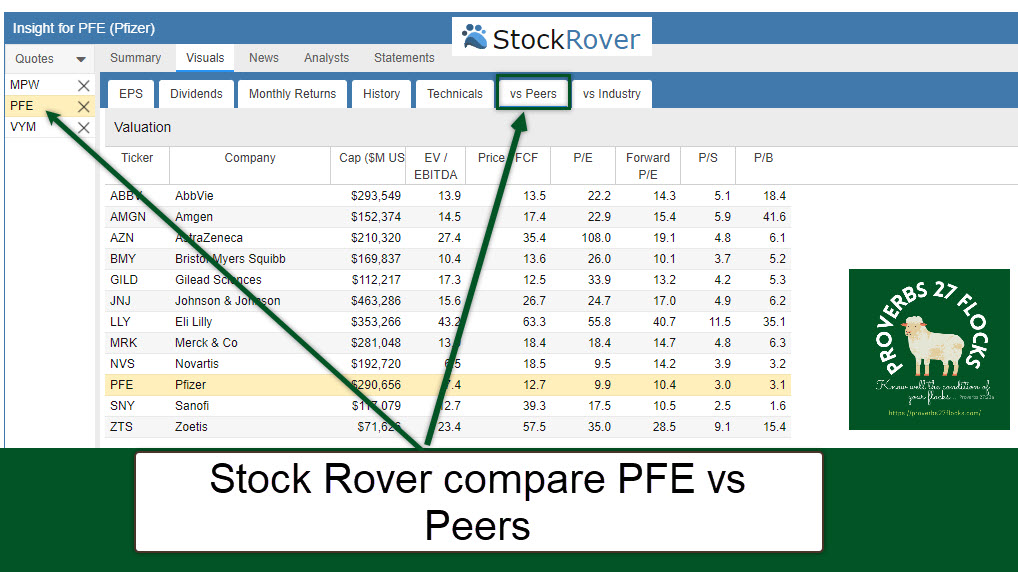

I look for similarities and differences. One thing that stands out is that both have shares of MRK and PFE in the top ten. Using the peers feature in Seeking Alpha or Stock Rover, I get a list of possible competitors.

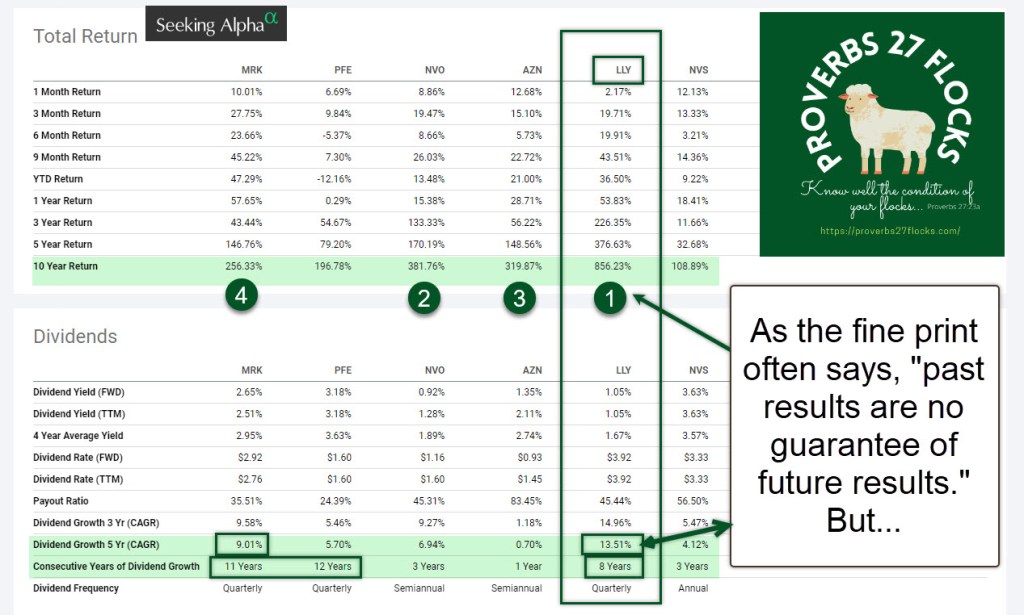

In Seeking Alpha, when I look at peers for MRK the default stocks are: PFE, NVO, AZN, LLY, and NVS. It then is very easy to make a comparison of the dividends, the dividend yield, the dividend growth and the number of years of growth for these six, and the 10 Year Return. Once again, a word of caution. Just because LLY has some great historical numbers, there are other factors to consider.

For example, LLY has a PE (FWD) of 47.55. MRK has a PE (FWD) of 14.91. ABBV has a PE (FWD) of 11.94. The comparisons could go on. Apparently, in this market, investors are willing to pay more for LLY’s future earnings growth potential than they are to expect great growth going forward for Merck or Abbvie.

Look at Other Sectors Too

You could do the same with the other top ten in SCHD. I could look at IBM, AVGO (Broadcom), CSCO (Cisco), HD (Home Depot), and PEP (Pepsi) and their peers. The reason is simple. These companies are in different sectors. If I want to pick five-dividend growth stocks, I don’t want five in the health care sector. I’d rather have some in the technology sector, financials, and consumer goods.

In fact, I own 300 shares of AVGO. AVGO just announced something that makes me smile: Broadcom raises quarterly dividend by 12.2% to $4.60/share. I have 300 shares of AVGO, so I will be receiving $1,380 in dividends on December 30. Last quarter I received $1,230. Buy and hold is working all the way to the bank. (Broadcom (NASDAQ:AVGO) declares $4.60/share quarterly dividend, 12.2% increase from prior dividend of $4.10.) Note: AVGO’s ten year returns are more than 1,600%. I wish I had purchased AVGO in 2012.

Trading Options on ETFs or Stocks?

Another reason to consider stocks in addition to ETFs is the opportunity to sell covered call options on your shares for additional income. While it is possible to trade options on some ETFs, it is nowhere near as profitable as trading options on a stock like ABBV. Furthermore, although I can trade options on VYM, I don’t want to do that. I don’t want to risk having my shares called away.

Other Resources

You could read what Justin Law says. He is the author of The Dividend Kings. “Maximize your income with the world’s highest-quality dividend investments.” Here is a link to his December 4 Seeking Alpha article: LINK for Dividend Champion, Contender, And Challenger Highlights: Week Of December 4. When racing horses you want champions, not nags (a nag is an old, worn-out horse). When picking investments, pick champions.

If you Google “Dividend Growth Investing” you can find lots of interesting ideas. Within 30 seconds I found a link to a site called “Dividend Data.” Here is a link: DIVIDEND DATA

Summary

If you don’t have a lot of money, which is often the case for beginning investors, stick to ETFs. If you have a growing pile of investment dollars, you may want to start by buying 5-10 shares of a company stock, after you have done your research.

You can get a better return when investing in individual stocks. You can also experience a more traumatic loss if you decide to sell during a bear market.

What Might You Do?

One way to see where I have confidence is to look at my top ten investments. VYM is number one. However, AVGO is certainly in my top ten. My AVGO shares are currently worth about $159,000. I would not have that kind of money in a single company’s stock if I thought it was high risk junk. I think it is a champion.

A Reminder from King Solomon

When Solomon talks about his investments, he talks plural. He doesn’t just own sheep, he also owns cattle. And in both cases he has multiple groups of animals, probably in different pastures with different shepherds. That is diversification.

“Know well the condition of your flocks, and give attention to your herds, for riches do not last forever; and does a crown endure to all generations?” Proverbs 27:23-24 ESV

Wayne, Thanks for sharing your thoughts. Why do you prefer ETFs to mutual funds if you don’t plan to be an active trader?

Sent from my iPhone

>

LikeLiked by 1 person

There are a couple of reasons. When you buy a mutual fund you have to pay an unknown price. You place the order when the market is open, and you get the price of the fund after the market closes. Lets say you place the order at 10AM and the price at that time is still the previous day’s price. Let’s also assume that was $50. You see that the market is going down, so you place your order, anticipating a price below $50. However, some news makes the stock market charge up and the mutual fund, after close, has shares valued at $51.50. That is an unnecessary risk. I can place a buy limit order for an ETF and wait for the price to come to me. Let’s say the ETF I am interested in closed at $50 yesterday, and I see the market is going down at 10AM. I can enter a buy order for $49.50 (or whatever price I choose) and wait to see if someone will sell me there shares at that price. This is often the way I get a better deal on my shares.

Also, you cannot control how a mutual fund manager might behave when it comes to selling positions. If you have the mutual fund in a taxable account, you can wind up with a surprise of big capital gains that you were not anticipating. This can make your tax situation for that year ugly.

So, even though I don’t buy-and-sell the ETFs, I want more control over what is happening. ETFs rarely pay capital gains.

Does that help?

LikeLike

Thanks for your prompt and helpful reply😊 I understand the advantage of being able to place a limit order and knowing the price when you make the trade rather than having to wait for the close of the market. But if you only buy index funds are you exposed to the manager incurring surprise gains and loses?

LikeLiked by 1 person

If I understand what you are asking, and you only buy index funds, then you probably aren’t going to have surprises. Nevertheless, you still have the potential to buy something at a price higher than what you would have liked during a volatile market. Of course, there is also the potential that you might get more shares than you expected because of a steep drop on the day you place your order. I like to compare this to buying just about anything else. There are very few products where you go to a store, or online, and just give the business $500 and let them determine how many widgets or whatever based on their employee costs, an increase in utility rates, or other things outside of your control. If you want 100 widgets, and you think $500 will buy them, you don’t want to get 97 widgets. Again, for index funds the risk is much smaller, but the pricing model makes an ETF with a similar index and expense ratio a better choice for me.

All things being equal, I’d rather buy ETF SPY than any of the mutual funds that track the S&P 500. It used to be that fund companies over-charged for their index funds. Thankfully, the competition of ETFs made their solutions less popular, forcing them to lower their costs.

LikeLike

Both the article and the conversation in the comment section were helpful to me! I’m probably still in the ETF-only timeframe, but looking ahead!

LikeLiked by 1 person