Reinvesting Dividends to Increase Your Shares and Income

If you invest in stocks or ETFs that don’t pay a dividend, you don’t have to worry about reinvesting dividends. However, you probably face increasing risks and many other choices as you approach your retirement age. If you fund your retirement with Social Security, it is likely Social Security will not provide enough monthly income to cover your monthly expenses. If that is the case, you may have to sell portions of your investments to get the cash you need.

Unfortunately, you cannot predict what the market will do one week from today, much less one year before you take your retirement plunge. When you decide you need cash you may be looking at a market that is down 30 percent or more. You may have quality investments, but during a bear market just about every asset is punished due to the mass exodus from equities.

Retirement Income Strategies

There is a business in the area where we live that provides services to clients that are nearing or are in retirement. The business is known as “Retirement Income Strategies.” In a video on their website, Kristian Finfrock says, “Our main focus is really helping people understand the shift from accumulating assets to the preservation and distribution of assets.” They then help their clients turn their assets “into a stream of income, hopefully a stream of income that they will never outlive.” They help individuals create retirement strategies using investments and insurance products.

Let me suggest what I think is a better approach. First of all, insurance like annuities, is not the best choice for most prudent investors. Rather than face the decision (and work) of moving from investments that don’t pay you quarterly or monthly, start buying those investments now. In addition, if you have investments that are not paying dividends, consider moving gradually from those investments to ones that are not only paying dividends, but are paying increasing dividends. You can create your own stream of income and you don’t have to pay an advisor, no matter how good they are, anything to do this. Furthermore, good investments are a better choice for most individuals and couples than any annuity I have ever seen.

What Are the Benefits of Reinvesting Dividends?

Reinvesting your dividends gives you quarterly (or monthly) opportunities to buy more shares and build wealth over time. You could take the cash, of course, and when you reach retirement, you will probably need the cash to replace what your employer is currently paying you for your time and expertise. The “secret” is to keep doing this quarter-after-quarter, year-after-year. If, for example, you own shares of the Vanguard High Dividend Yield ETF (VYM), you would have received $0.6622 for each share on March 24, 2022. Then, on June 24 you would have received $0.8479. For the third quarter, the payout on September 22 would have been $0.7672. I expect another dividend in late December.

On each of those dividend payment dates, the price per share of VYM was different. On March 24 the shares were trading at around $112.48. $103.31 would have been the price to buy a share on June 24th. In September the price was around $99.65. The wise investor knows prices go down and up. However, you don’t know in March what the price will be in September. What really matters is this: each time you buy shares, you add shares that are likely to give you more dividends in the following quarter. Then you buy even more shares at a lower price, if the price per share drops. I love it when that happens. This is a powerful engine for income growth.

This approach is called “dollar cost averaging.” You want to avoid trying to time the market and avoid trying to guess when the price will be more favorable. Your total cost is less likely to be influenced by market timing.

Dollar Cost Averaging

According to Investopedia, “Dollar-cost averaging is the practice of systematically investing equal amounts of money at regular intervals, regardless of the price of a security. By buying regularly in up and down markets, investors buy more shares at lower prices and fewer shares at higher prices.”

In addition, this approach helps prevent poorly timed lump sum investments at a price that might not be best. So, for example, if I receive $5,000 in dividends in the fourth quarter, I divide that money into a couple of different ETF purchases. But I might not buy all of the shares as soon as the dividends arrive. I might wait a week and then buy some. Then, a week later, buy some more, and so on until the $5,000 has been invested in more shares. I want to do this before the next quarterly dividend is declared. The reason is simple: I want the new shares to receive the next dividend so that I can buy even more shares of the investments I hold.

A Dollar Cost Averaging Example

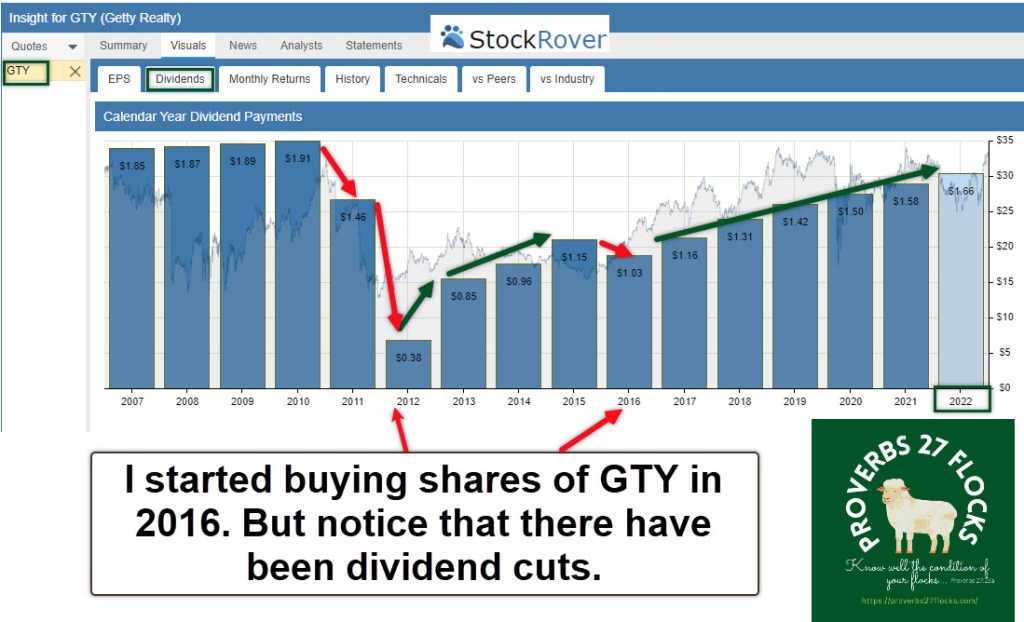

By way of example, I like shares of a REIT called GTY. GTY is Getty Realty Corp. I have 700 shares of GTY in my traditional IRA. It pays quarterly dividends. But I did not buy all 700 shares at one time. Rather, I bought 100 shares, and then added another 100, and then another, until I reached the number of shares I wanted to hold. So now my 700 shares are paying me $1,204 in dividends each year. I can now use that money in retirement. I don’t have to reinvest the dividends unless I want to do so.

Furthermore, I don’t need to change my investing strategy just because I entered retirement. I may reinvest the dividends, or I might just take the cash.

Summary

The beauty of dividend reinvestment is that you don’t have to try to time the market. Dividends flow into your account at least quarterly for most stocks and stock ETF investments that pay a dividend. You can buy more shares of the same investment or buy shares of a different investment. This grows your income in an easy way.

What Might You Do?

Do you know what your income is from your current investments? It isn’t hard to see this on the monthly Fidelity statement or in the positions page on their website. If you go to your positions, just click on “Dividend View.” If one of your positions does not pay a dividend you will see two dashes (–) in the column that shows the “Est. Annual Income.” There will be a total for each account you own and a total for all of your accounts.

To illustrate how powerful my approach is, my estimated annual income in my traditional IRA will be $91,988.52 in the next twelve months. That will more than cover my RMD for 2023 and it will provide some amazing opportunities for my wife and I to give money away.

A Reminder from King Solomon

Having more and having great treasure will not satisfy or bring joy. You cannot take it with you. Don’t waste this life chasing treasures that don’t last and that will never meet your deepest needs. Always chose better over trouble.

“Better is a little with the fear of the Lord than great treasure and trouble with it.” Proverbs 15:16 ESV

LINK for Retirement Income Strategies

I would typically look at price per share and not focus much on the dividend growth. This series has helped me see the need for a larger view than simply the price per share.

LikeLiked by 1 person