Build A Longer CD Ladder

In my last post on this topic of wise cash management, I provided the steps to do a 1-2-3-month CD ladder. For my own purposes, buying CDs with a longer time horizon doesn’t really make sense when the Federal Reserve is aggressively raising rates. However, some investors with cash they are saving for a longer-term project or large purchase might want to take a different approach.

Other Preset CD Ladders and a Caution

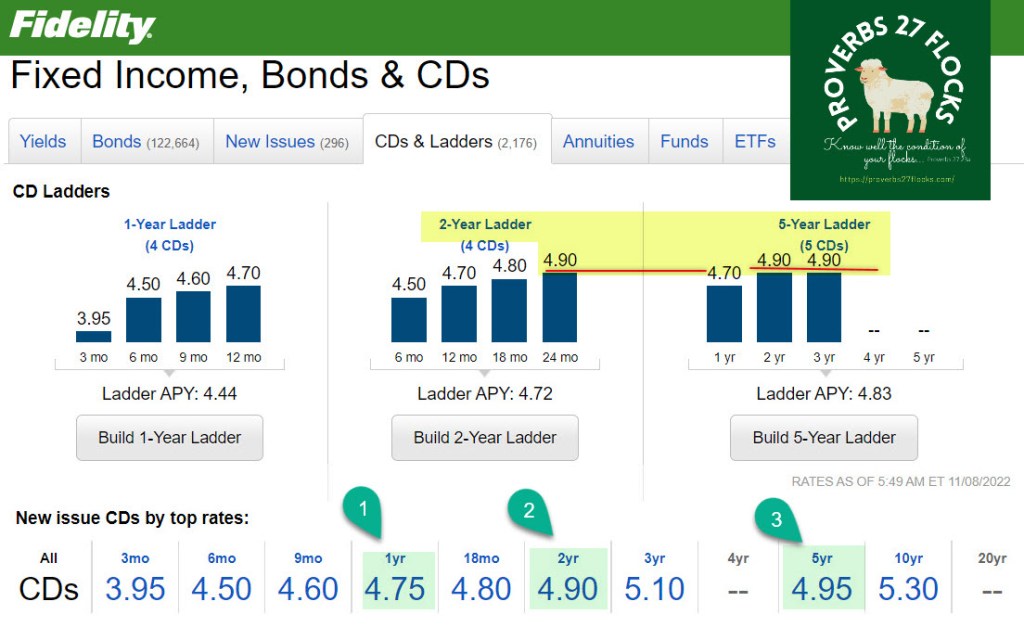

Fidelity offers three preset ladders. 1-Year Ladder (4 CDs or $4,000), 2-Year Ladder (4 CDs or $4,000), or 5-Year Ladder (5 CDs or $5,000). You can also build a “Custom CD Ladder.” It is generally unwise to buy a 2-year ladder unless you have a specific project that is two years out. I would suggest that a 5-year ladder is probably foolish for two primary reasons.

First of all, the additional interest you will earn from the longer-term CD to lock up the usefulness of your cash is insignificant. I would rather have cash earning 4.7% for twelve months than tie up the cash for two or three years for 4.90%. Secondly, the Federal reserve has been changing the rates upwards in 2022. There may be some slowing of that increase in the months ahead, but why tie up too much cash for too long?

On November 2, 2022, the Federal Reserve interest rate was changed to 3.75% to 4.25%. According to the Motley Fool, this is “the fourth consecutive rate hike of 0.75% and the sixth rate hike this year. These rate hikes are the fastest cycle in history, pushing borrowing costs to a 15-year high.” LINK

Enter an Order to Buy a Laddered CD

Now you may be ready to purchase a CD ladder. On October 26 I did some screen shots of the Fidelity CD rates. Rates have changed slightly since then, due to the November 2 rate increase. However, the concepts and the process are the same.

First of all, you want to click on News & Research and select the Fixed Income, Bonds & CDs link. Then select the tab for CDs & Ladders. You can then select a 1-Year Ladder, or if you have a longer horizon, perhaps a 2-Year Ladder.

Click Build 1-Year Ladder. Fidelity will ask you which account you want to use to buy the CD. In my case, it can be any of five different accounts. This includes brokerage, IRA, and ROTH IRA accounts. I would not recommend buying CDs in IRA accounts unless you have a specific reason for doing so. I bought come CDs in Cindie’s IRA because I want to have cash available for her required 2023 RMDs.

Fidelity will then ask you, “How much would you like to invest? Tell us the total amount you would like to invest in your ladder.” The minimum amount is $4,000.

Fidelity then wants to know “Do you want maturing positions to be deposited or re-invested?” I think the best answer is “Return maturing principal to my core account. Each CD will return its final coupon and principal into your core cash account when it matures.” This gives you your cash to use for your project or for a pending large expense.

Fidelity will select four CDs for the four rungs of your 1-Year Ladder. For simplicity’s sake, you can click CONTINUE. However, if you want to be more selective, you can make changes to the choices Fidelity presented. For example, you can select “View other available CDs” for any or all of the rungs. The four rungs are for three months, one for six months, one for nine months, and finally, one for twelve months.

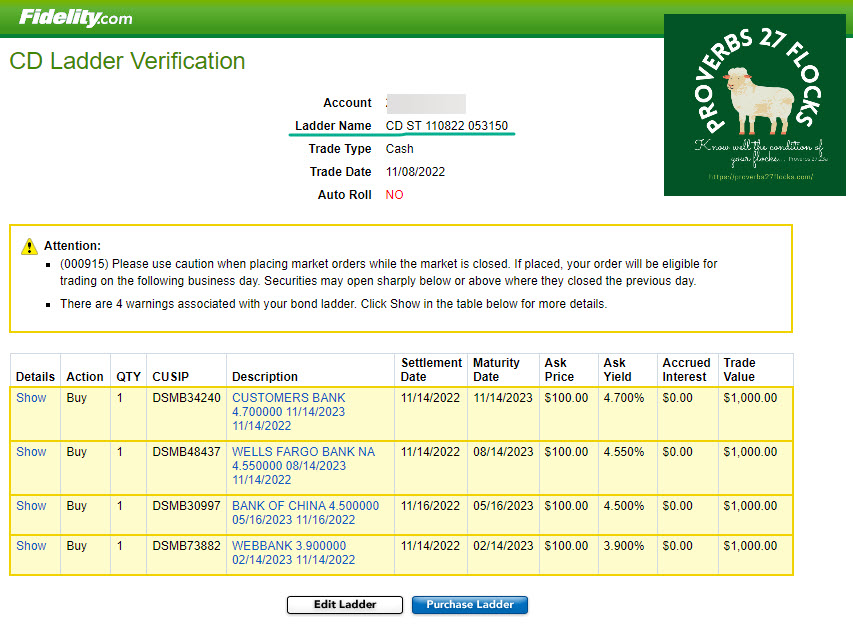

Like most order entry processes, Fidelity then asks you to do a CD Ladder Verification. Once you have done this, you can click “Purchase Ladder” or you can “Edit Ladder” if you want to make any additional changes. (I did not place the order.)

Here are Cindie’s current CDs. They are holding cash for her 2023 IRA RMDs.

Your CDs Might Not Be Purchased

Fidelity offers the following in the fine print at the bottom of the page. “If you leave the CD Ladder Verification page prior to clicking Purchase Ladder, your order will not be placed.” They also tell you:

By clicking Purchase Ladder, you understand that these orders do not cancel (or cancel and replace) any existing orders, and you are agreeing that the order information is correct and you are authorizing Fidelity to execute these orders on your behalf.

Please note that the dollar values in the Trade Value column are inclusive of accrued interest and estimated concessions and fees.

Due to the illiquid nature of the market, it is possible that bonds displayed on Fidelity.com may no longer be available. Similarly, due to the manual nature of providing quotations, errors can occur, and bonds may be displayed at a price that is clearly away from the current prevailing market price. Fidelity reserves the right to cancel transactions in cases where the displayed offering is no longer available, or the price displayed is clearly away from the current prevailing market price.

Sometimes CDs are Better Than Dividend Stocks

CDs are not a bad choice for your emergency fund. The yield might be better than what you can get from a stock and your cash, within limits, is FDIC insured. However, bear in mind that your CD will never increase in value. Stocks can and do grow in value in a bull market. If you buy a $1,000 CD and then check it a week later, it might say the CD is now worth $995. Don’t be alarmed. It is still worth $1,000 unless you decide to sell it early for $995. The price that appears is the current market price. It isn’t the actual value of the CD if you hold the CD to maturity. It is rare that you will have an emergency that requires $1,000 immediately. If you are nervous, keep some cash in the money market mutual fund or your core cash account.

Here are some cautions from Fidelity Regarding CDs:

“The secondary market may be limited. The pre-maturity sale price of CDs may be less than its original purchase price, particularly if interest rates are higher at the time of sale. There may be certain features or provisions of the CD that may also influence its market price. If you want to buy or sell a CD on the secondary market, Fidelity Brokerage Services LLC (“FBS”) will charge you a markup or markdown.”

“Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Your ability to sell a CD on the secondary market is subject to market conditions. If your CD has a step rate, the interest rate of your CD may be higher or lower than prevailing market rates. The initial rate on a step rate CD is not the yield to maturity. If your CD has a call provision, which many step rate CDs do, please be aware the decision to call the CD is at the issuer’s sole discretion. Also, if the issuer calls the CD, you may be confronted with a less favorable interest rate at which to reinvest your funds. Fidelity makes no judgment as to the creditworthiness of the issuing institution.”

Don’t ask a Fidelity representative to buy CDs for you. That is silly and expensive. “Minimum markup or markdown of $19.95 applies if traded with a Fidelity representative. For U.S. Treasury purchases traded with a Fidelity representative, a flat charge of $19.95 per trade applies. A $250 maximum applies to all trades, reduced to a $50 maximum for bonds maturing in one year or less.”

Thanks for these posts. Helpful!

Jeremy

>

LikeLiked by 1 person