Build Your Own Short CD Ladder

In the previous post I suggested using some money market mutual funds for cash that may be need in the short-term or that may be needed in an emergency. Those funds are not FDIC insured. So while it may make sense to change your core cash position to FDRXX, FZFXX, or SPAXX, there are other approaches that work as well. CDs, as most know, have FDIC coverage. What some may not realize is that you don’t have to tie up your money for a year, or two years, or even for six months. Fidelity Investments usually has a broad selection of CDs anyone can buy. This includes CDs with shorter terms like one month, two months, and three months.

If you have $3,000 in idle cash, it may make sense to buy a one-month CD with $1,000, a two-month CD with the next $1,000, and a three-month CD with the final $1,000. If you take that approach, you are creating a CD ladder. There is more than one way to create a short CD ladder. For my purposes, “short” means “short term” or less than six months. For today’s post I will give you the steps to do a 1-2-3-month CD ladder.

Fidelity Investments Steps to Buy CD’s

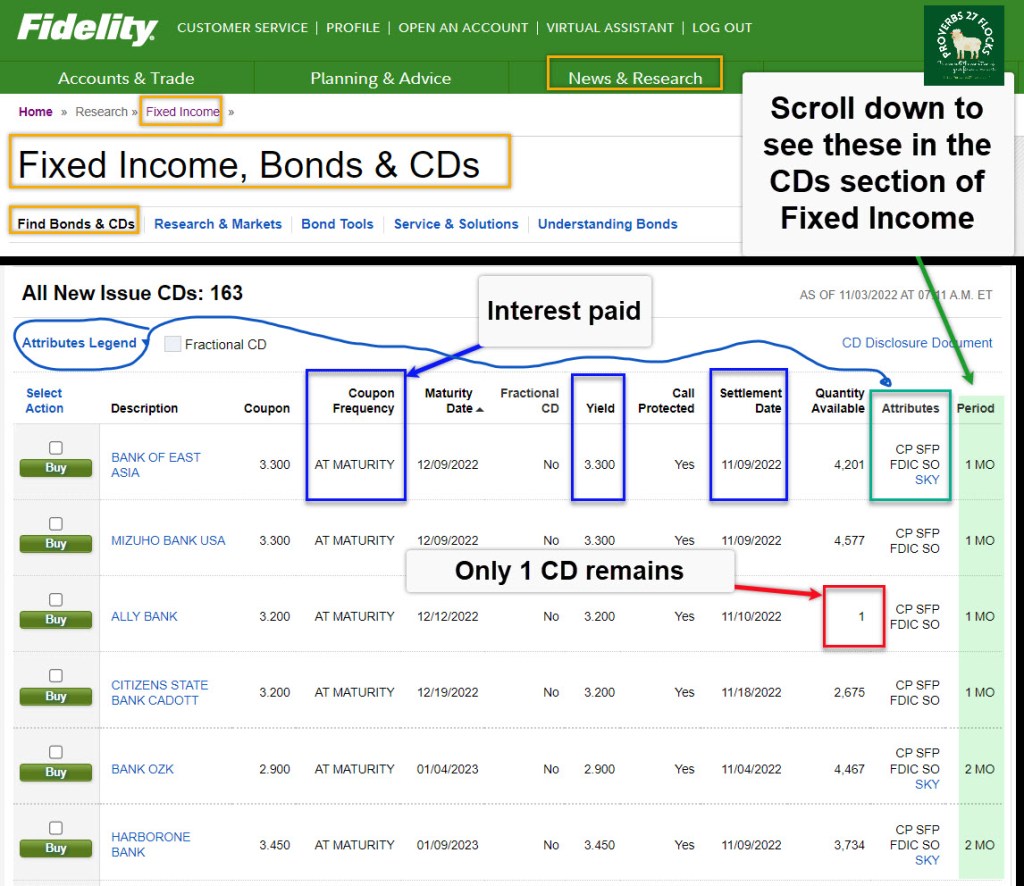

A long time ago the only way I could buy a CD was to go to the bank and fill out paperwork. That is no longer necessary. Everything can be done online. The easiest way to buy a CD is to click on the “News and Research” link in the top of the Fidelity main screen and then select “Fixed Income, Bonds & CDs.” Then look at the tabs that are presented and click on “CDs & Ladders.” At first it might appear that you can only pick 3-month, 6-month, 9-month and one-year CDs, along with some with even longer timeframes. However, if you scroll down, you will see there are many CDs that say 1MO, 2MO, and 3MO.

Look at the CD Attributes

One of the columns in the table of CDs says “Attributes.” There are three attributes of interest to me. The ones you will see are IE, RI, CP, FDIC, SKY, SO, and SFP. I always like to see CP (Call Protection) and FDIC. CP means the issuing bank cannot call the CD early. If you bought it for a month, they won’t give you your $1,000 back before the month is over. This means you will receive the promised interest. You have protection.

The other protection you have is FDIC insured. This is the norm, and I cannot recall seeing any CDs that are not FDIC insured. It never hurts to confirm. Finally, if an issue says “SKY” it may mean you cannot buy the CD if you are in one of the Blue Sky States. You can click on “SKY” if it appears to find out if the CD is prohibited in your state. For example, a CD from the Bank of East Asia is not available in MT, OH, and TX. This illustration shows another example with four states.

Most CDs have the following attributes: CP (Call Protection), FDIC (FDIC Insured), SO (Survivor Option), and SFP (Sinking Fund Protection.)

Enter an Order to Buy a CD

Now you are ready to purchase a CD.

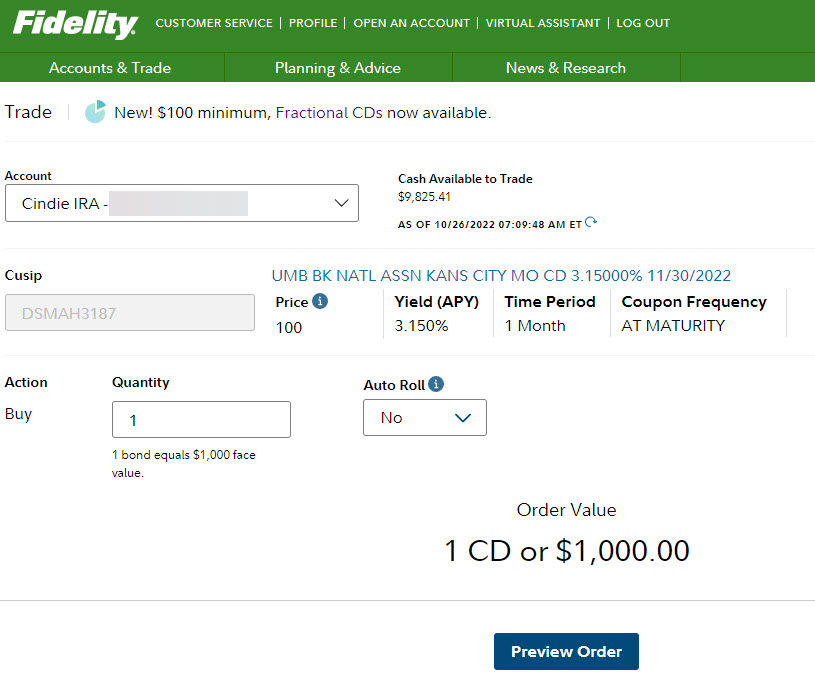

Click BUY on the CD you want to buy. Remember that one CD costs $1,000, so you must have $1,000 in your account’s core cash position. This can be any of the money market funds. It doesn’t matter. Cash is cash as far as Fidelity is concerned. Also note how many CDs are available. If it says “1” then there is only one remaining CD for that issue from that bank.

You will need to pick the account for the buy, the number of CDs (1 is $1,000, 2 is $2,000, etc.) and whether or not you want to “Auto Roll.” I always say “No” for auto roll because I want to pick the CD that I want to purchase, or I may want the cash for some need. Once you made your selections, click “Preview Order.”

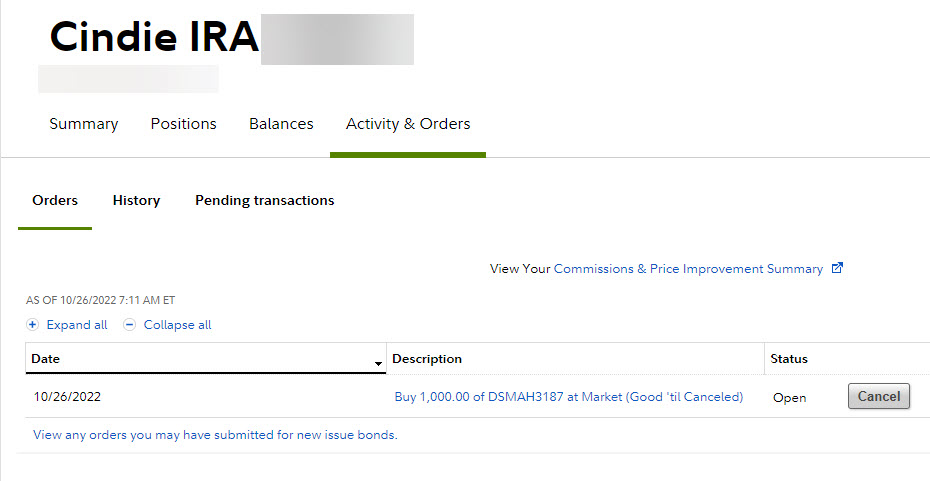

The Preview Order screen gives you additional information about the CD. The actual date the CD will be purchased depends on the “Settlement Date.” I might enter the order on October 26, but I won’t own it until October 31. If I click “Place Order” the order will be in my orders bucket. I can click on “Manage Orders” if I want to see it or delete it.

Orders Pending Screen

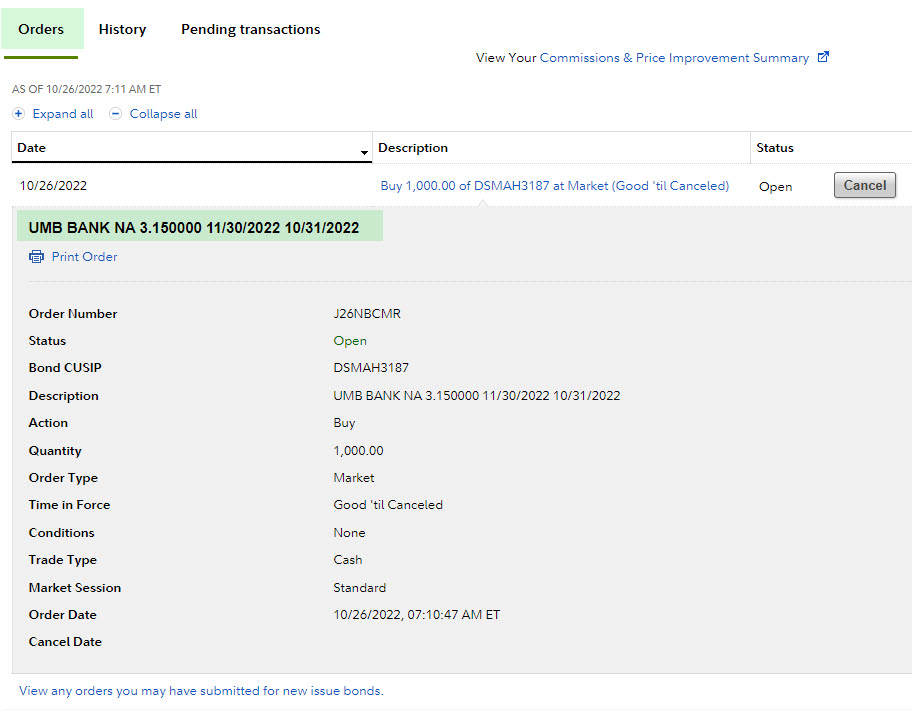

When you go to “Manage Orders” you will see something like the following. If you click on any individual order, you can see more details about that specific order.

Creating the Do-It-Yourself CD Ladder

The nice thing about doing it yourself, is you can pick a variety of CD’s. For example, I could buy two 1-month CD’s, one 2-month CD, and three 3-month CDs if I want to. If I did that, I would need $6,000 in total to buy the CDs (two plus one plus three is six.)

Sometimes CDs are Better Than Dividend Stocks

You can always get monthly income from some CDs. The yield might be better than what you can get from a stock. However, bear in mind that your CD will never increase in value. Stocks can and do grow in value in a bull market. If you buy a $1,000 CD and then check it a week later, it might say the CD is now worth $995. Don’t be alarmed. It is still worth $1,000 unless you decide to sell it early for $995. The price that appears is the current market price. It isn’t the actual value of the CD if you hold the CD to maturity. It is rare that you will have an emergency that requires $1,000 immediately. If you are nervous, keep some cash in the money market mutual fund or your core cash account.

Other CD Ladders

Fidelity offers three preset ladders. 1-Year Ladder (4 CDs or $4,000), 2-Year Ladder (4 CDs or $4,000), or 5-Year Ladder (5 CDs or $5,000). You can also build a “Custom CD Ladder.” Next time I will give you some thoughts about those ladders. One caution: Avoid buying 2-Year and 5-Year Ladders. I will explain why next time.