Is Your Cash Working as Hard as You Work?

There is nothing about cash that is appealing to me as an investor. Cash is just like gasoline in the tank of our Ford Escape. I fill the tank but not because I like the fuel. I like what the fuel can do. It can get me where I need to go.

I view cash in the same way. Fuel and cash are different in one regard. I can make my cash work for me at all times, while the regular gas does nothing until I start the engine. Recently, with the increase in interest rates, I have started to reevaluate how our cash is deployed. Until recently, cash was almost the same as fuel sitting in a tank. Now it can grow while in storage.

Is your cash working? I have some suggestions to make it work.

Our Cash Positions

In reality we have only three main piles of cash. One is in our Ally Savings account. That is the emergency fund. Another pile varies from day-to-day. That pile is in our bank checking account. It is replenished with our Social Security income via direct deposit and by direct deposit of Cindie’s parttime wages.

The third pile is stored in eight Fidelity Investments Accounts. Two of those are ROTH IRAs, two are traditional IRAs, and the remaining for are different types of brokerage accounts. About 1.4% of our total Fidelity assets are in cash. This can vary widely, as dividends come in that increase the cash holdings. These dividends get deposited in the core accounts used for holding uninvested cash.

Half of our Fidelity accounts use a mutual fund with the ticker symbol SPAXX. This is the Fidelity Government Money Market fund. It is the “core” position. The other four accounts have cash in a position called “CORE.” Core, as it turns out, is not a good place for cash unless I plan to invest the cash soon. Even then, Core is a questionable tank for cash. Today I will talk about the choices and why I am changing from using the default “CORE” to money market mutual funds.

Fidelity’s CORE Holding Bucket

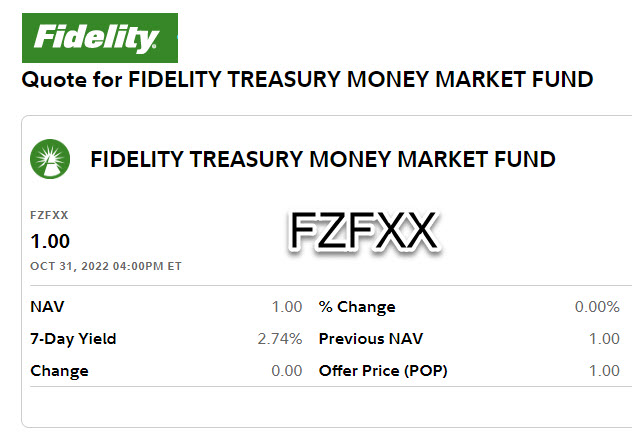

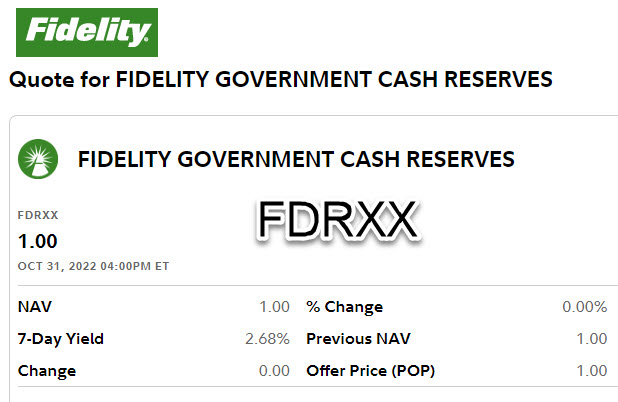

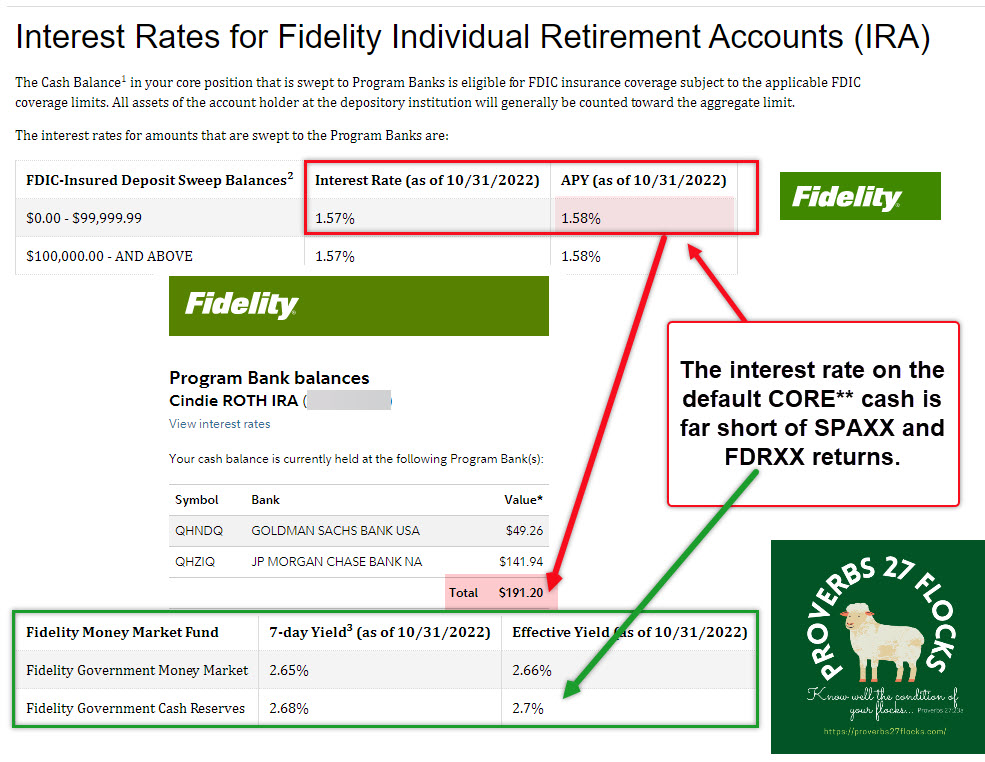

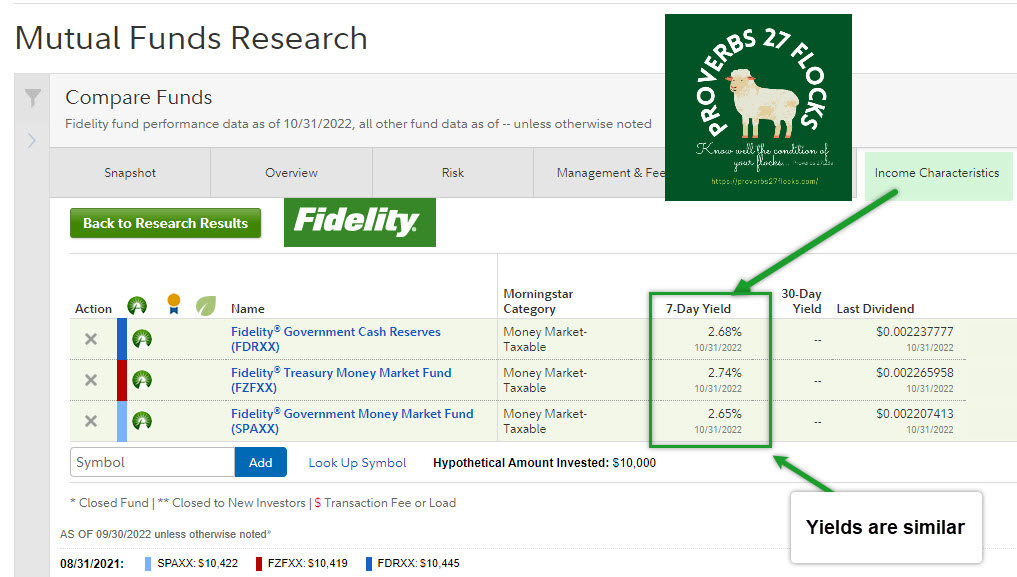

Your core position holds the cash in your account. You can choose your core position from at least four options, but not every option is available for every account. I have found that I have four choices. They are CORE FDIC-INSURED DEPOSIT SWEEP (the default), SPAXX, FDRXX, and FZFXX. The last three are money market mutual funds. SPAXX is the Fidelity Government Money Market Fund, FDRXX is the Fidelity Government Cash Reserves, and FZFXX is the Fidelity Treasury Money Market Fund. The main benefit of CORE is that it is stored at banks with FDIC insurance.

Fidelity picks banks for the CORE FDIC-insured cash holdings. In one of accounts the two banks are GOLDMAN SACHS BANK USA and JP MORGAN CHASE BANK NA. Big banks are generally safe banks. As a result, many investors think the “CORE” FDIC insured account is a good idea. I suppose if you had $250,000 in cash, that might make some sense. What you gain from the “insurance” you lose in interest.

FDIC “Insurance” Coverage

The FDIC covers checking accounts, Negotiable Order of Withdrawal (NOW) accounts, savings accounts, Money Market Deposit Accounts (MMDAs), time deposits such as certificates of deposit (CDs), Cashier’s checks, money orders, and other official items issued by a bank. The FDIC does not cover stock investments, bond investments, mutual funds (like SPAXX, FDRXX, and FZFXX), crypto assets, life insurance policies, annuities, municipal securities, safe deposit boxes or their contents, and U.S. Treasury bills, bonds, or notes. The last one, US Treasury stuff, “are backed by the full faith and credit of the U.S. government.” The standard insurance amount is $250,000 per depositor, per insured bank, for each account ownership category. So Fidelity puts funds in multiple banks to give you more “insurance.” However, I would suggest that having more than $100,000 in FDIC insured account probably is not wise.

Many Banks Are CD Devils (with FDIC Insurance)

I have a Chase VISA card that we use for Amazon Prime purchases. I like that card, so I went looking at the Chase Bank CD rates. I was very disappointed. I have found that most banks do the same thing as Chase. They take your money and don’t give you much in return.

Even the bank where we have our checking account, Wisconsin Bank and Trust, is a CD devil. Their 3-month CD interest rate is 0.01%, and their 12-month CD earns a paltry 1.60%. At least Chase offers 2.28% on their 12-month CD. Chase’s 3-month CD earns a dismal 0.02%. These investments are FDIC insured, but that is expensive insurance. In a future post I will talk about a place where you can get much better interest rates on 1-month, 2-month, and 3-month CDs. Today our focus is on the mutual funds.

Comparing CORE, FDRXX, FZFXX, and SPAXX for Income

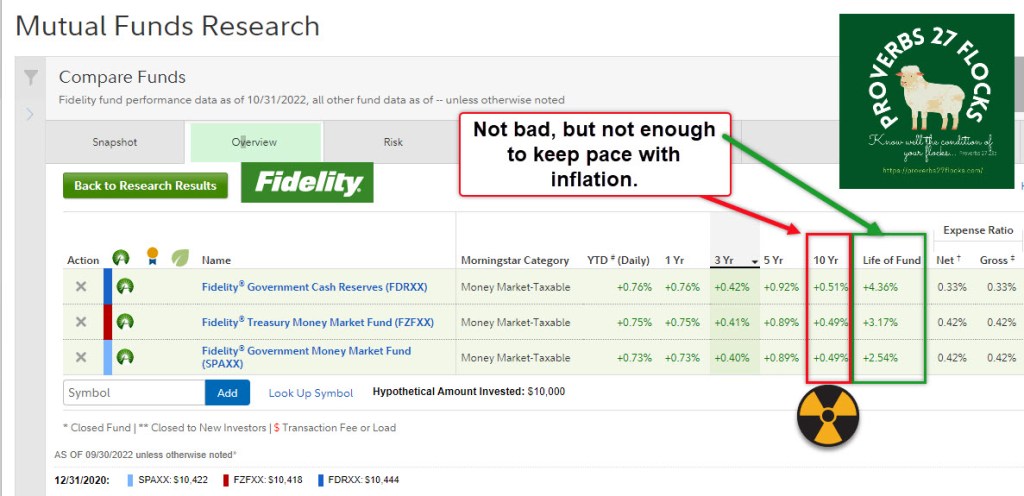

A prudent investor always asks, “What is the expense ratio?” for these three funds that ratio is 0.33%, 0.42%, and 0.42%. The seven-day yield on these is 2.68%, 2.74%, and 2.65%. Therefore, the net yield for FDRXX is 2.35%. For FZFXX it is 2.32%. For SPAXX the yield is 2.23%. There is no expense ratio for the default CORE (FDIC-INSURED DEPOSIT SWEEP) so it earns 1.58% at present. Said another way, the three mutual funds pay you more than the CORE does. You sacrifice FDIC insurance if you choose to move your core cash to the money market mutual funds. I think it is worth going with SPAXX, FDRXX, or FZFXX given how little cash I hold. It should be noted that Weiss Ratings gives all three a C+ rating. That is more than adequate for cash.

The Government Funds are taxable, but the NAV (Net Asset Value) is a constant $1.00 per share. That means for every “share” of SPAXX, the share is worth $1.00 per share. I have never seen it go lower than that or higher than $1.00 per share.

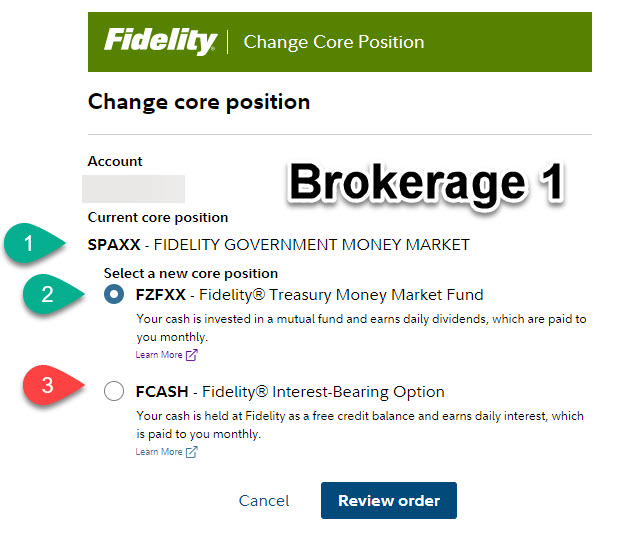

Making the Change from CORE to SPAXX or FDRXX or FZFXX

You might find that some of your accounts cannot buy some of these. For example, one of our accounts does not have a selection to change the CORE account from CORE to any other fund. My traditional IRA can only switch from CORE to SPAXX or FDRXX. It looks like FZFXX is not available. I may call Fidelity to ask why that is so. However, I plan to move the cash from CORE to SPAXX in the near future. Before I do, I want to think about buying some 1-month CDs instead.

Cash in the UTMA Accounts

Our six grandchildren have UTMA accounts. I am the custodian of those accounts. Currently cash sits in FCASH (the core account) and FDRXX. I submitted a change for their core accounts from FCASH to FZFXX. The reason is simple. FCASH currently pays 1.57%, while FZFXX pays 2.74%. Although they have very little cash, even their little bit should earn more interest. FZFXX cash is invested in a mutual fund and earns daily dividends, which are paid monthly.

FZFXX NOTE: “You could lose money by investing in the fund. Although the fund seeks to preserve the value of your investment at $1.00 per share, it cannot guarantee it will do so. An investment in the fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. Fidelity Investments and its affiliates, the fund’s sponsor, have no legal obligation to provide financial support to the fund, and you should not expect that the sponsor will provide financial support to the fund at any time.” – Fidelity Investments

Full Disclosure

Cindie and I have a little more than $10,000 in an Ally online bank savings account that is currently earning 2.35%. The interest rate has been increasing monthly over the last several months. At the beginning of 2022 the interest rate was 0.50%. However, I am now considering alternatives. 2.35% is OK for a savings account, but there are other FDIC insured options with a better return. We may move this money to Fidelity and buy 1-month CD’s that are currently paying more than 3.0%.

LINK: FIDELITY FCASH

Hi Wayne.. is there a penalty to take money out of fdrxx or spaxx.

LikeLiked by 1 person

There is no penalty for withdrawing cash from a money market fund that is in a brokerage account. However, if it is in a ROTH IRA or traditional IRA, the same rules apply for all withdrawals. If the ROTH has been open long enough, there are no restrictions or income taxes. Any money withdrawn from a traditional IRA is, of course, subject to income taxes. However, there is no penalty as such.

LikeLike