The Federal Reserve is Helping Some of Us

Increases in the Federal Reserve Prime Rate have implications for homebuyers and for savers. It is far too easy to be complacent about cash. It is foolish to have too much credit card debt. Far too many individuals have far too much cash in their investment accounts, savings accounts, checking accounts and home safes. During the next couple of weeks, I hope to provide some suggestions for leveraging cash with wisdom. The goal is to protect your emergency fund and put cash to work. Today I want to outline the topic. Cash is expensive if you have to borrow to get it.

What is the Federal Reserve Doing?

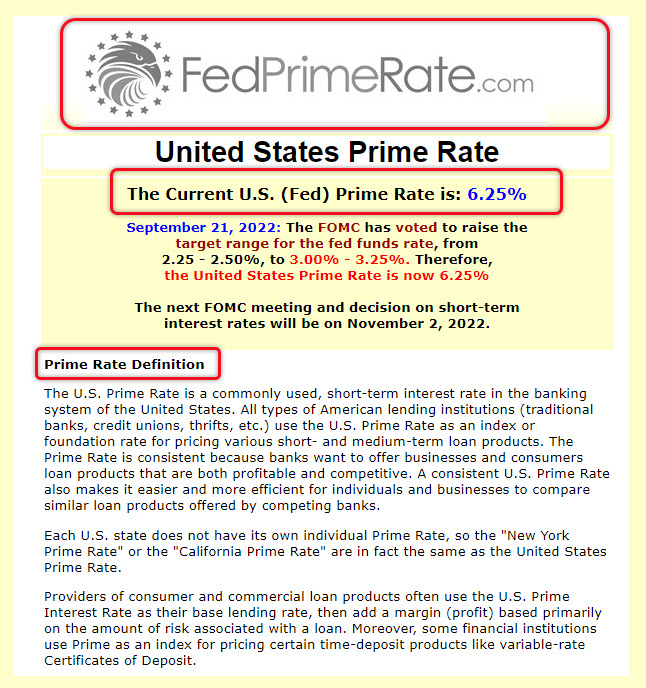

“Now that the Federal Reserve has been raising the United States prime rate, the current U.S. (Fed) Prime Rate is: 6.25%. As of September 21, 2022: The FOMC has voted to raise the target range for the fed funds rate, from 2.25 – 2.50%, to 3.00% – 3.25%. Therefore, the United States Prime Rate is now 6.25%. The next FOMC meeting and decision on short-term interest rates will be on November 2, 2022.” SOURCE: LINK to FedPrimeRate

What is the definition of the Prime Rate?

“The U.S. Prime Rate is a commonly used, short-term interest rate in the banking system of the United States. All types of American lending institutions (traditional banks, credit unions, thrifts, etc.) use the U.S. Prime Rate as an index or foundation rate for pricing various short- and medium-term loan products. The Prime Rate is consistent because banks want to offer businesses and consumers loan products that are both profitable and competitive. A consistent U.S. Prime Rate also makes it easier and more efficient for individuals and businesses to compare similar loan products offered by competing banks.” SOURCE: LINK to FedPrimeRate

Why Does This Matter?

“As of Saturday, October 29, 2022, the national average 30-year fixed mortgage APR is 7.15%. The average 15-year fixed mortgage APR is 6.43%, according to Bankrate’s latest survey of the nation’s largest mortgage lenders.” This makes home mortgages far more expensive. But this also makes the interest you can earn on your savings more appealing.

While some might think this is bad for stocks, and it can have an impact, most dividend-growth investors don’t use dividend growth as a short-term strategy. Therefore, the current dividend yield is not the main deciding factor. While I might make 3.15% on a one-month CD, and that is better than the rate I can earn on some of our stocks, the stocks have more value because they have a long-term view, not a short-term interest rate view. Link to BankRate.

What Should We Think About Regarding Cash?

Let me suggest a couple of things you want to do. First, you want to have a strategy for your cash. Then, you need to think about where you will put your cash, and how long you will need to have cash on hand. You also want to think about how much you can earn on your cash and pick options for each bucket of cash. There are multiple buckets including monthly expenses, quarterly expenses, semi-annual expenses, annual expenses, and emergency expenses.

The Cash Strategy That Thinks About Now and Tomorrow

Cash is needed for daily needs, weekly grocery shopping, monthly bills (charitable giving, mortgage or rent payments, utilities, cell service, SimpliSafe security monitoring, Medicare supplement insurance coverage), quarterly expenses (I pay our estimated Federal and State income taxes quarterly), semi-annual expenses (automobile liability insurance premiums), annual expenses (property taxes, umbrella insurance premiums, subscriptions for things like Seeking Alpha), and emergency one-time costs like replacing the exhaust motor assembly on our Ruud furnace this week and some dental work Cindie has scheduled.

There are other future cash needs for things like travel or replacing a vehicle when the 2020 Ford Escape starts showing signs of age. For those it is wise to think 2-5 years into the future. However, this does not have to be too complicated. Well, perhaps for some of my readers who live paycheck-to-paycheck and buy things with credit cards, this will be complicated. You should start with a budget and get rid of all short-term credit card debt, HELOC debt, and auto loans.

Our Situation is Cash Poor but Cash Flow Rich

Much of our ongoing normal expenses are covered by monthly Social Security income. Even more cash flows in from our dividend-growth stocks and ETFs. Still more cash arrives when I trade covered call options. In addition, Cindie has income from her part-time job as a baker at Beehive Homes in Oregon, Wi. The strategy for much of the cash is to cover all of the normal expenses for the entire year. The “leftover” cash can then be invested. As a result, we don’t need to have a huge emergency fund. Our fund currently stands at $10,000.

The emergency fund is the one that may require attention now that interest rates are rising. Rather than keeping emergency funds in a checking or savings account, it is better to think about some better interest rate solutions. That will be the subject of a future post.

More to Come – Stay Tuned

In some future posts I hope to talk about money market mutual funds, emergency funds, CD’s and CD attributes, CD ladders, and any questions that come my way from each post.

This is very helpful, Wayne! Thank you!

LikeLiked by 1 person