Our Children’s Investing Education

When I was the father of early teenaged children, what I knew about investing could have been summarized in two paragraphs. Actually, the correct analysis would have been two words: “Very little.” As a result, I was not prepared to teach our son and daughter this helpful piece of managing personal finances. Furthermore, when they were teenagers, there were no ETFs and mutual funds were expensive and a mystery. Things have changed in the last three decades.

Our Grandchildren and their UTMA Accounts

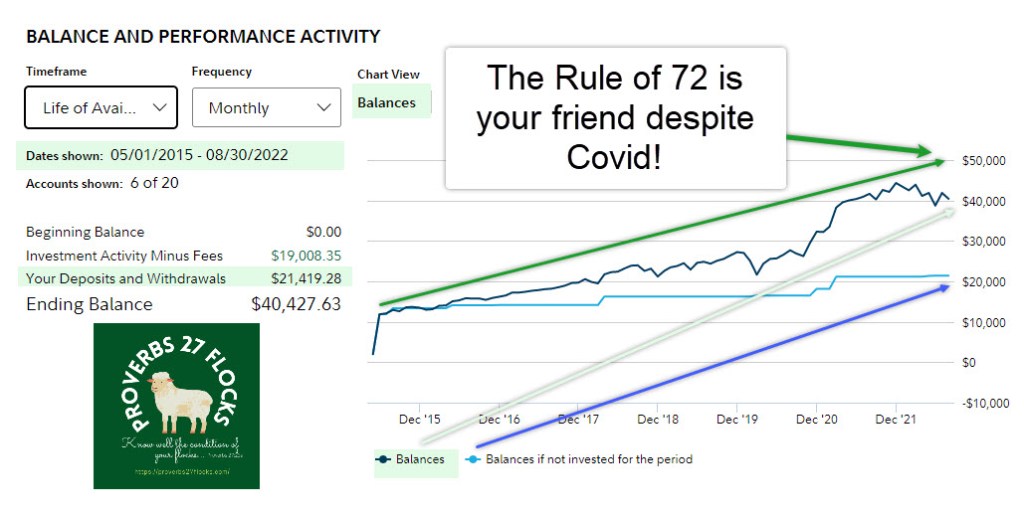

We have been blessed with six grandchildren. Cindie and I opened UTMA accounts for all six more than seven years ago. A recent performance snapshot shows their average 5-year growth on their investments has been over 12%. They don’t own bonds or hold much cash. They do own ETFs that I carefully selected and that I have generally held for the long-term. Before you sing my praises, realize that the S&P 500 has done a bit better than the UTMA accounts, but not by much.

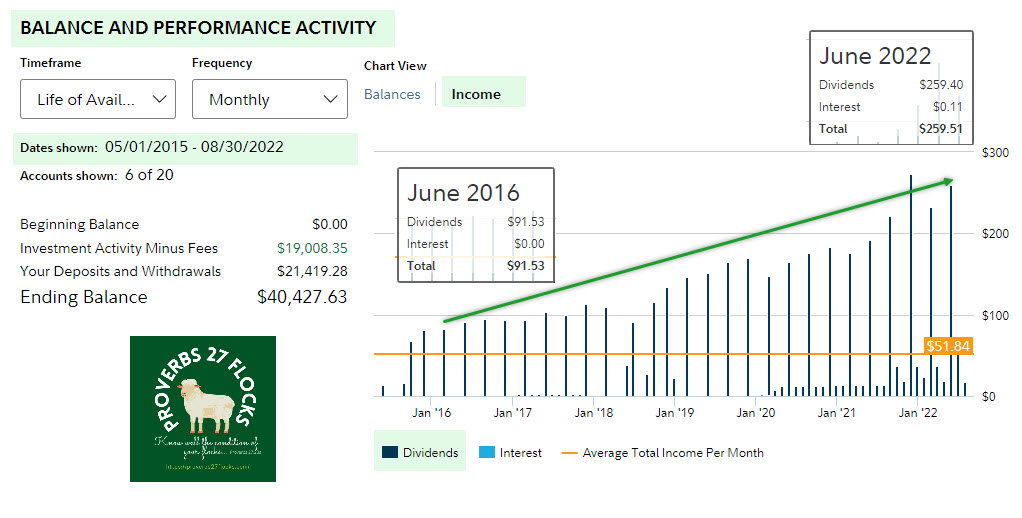

However, there is another important factor that is overlooked by many investors. A bird in the hand is often worth two in the bush. I am talking about dividends. As you can see in the illustration above, the six accounts earned a total of $91.53 in dividends in June 2016. That has increased to $259.51 six years later. While it is true that some of this increase is due to adding more cash and buying more investments, much of the income growth is patiently waiting for dividend growth. You might be able to sell an investment for a profit down the road, but you have to sell to get a profit (or a loss). If you invest in dividend growth stocks, you can get more of your money today.

Investing in Our Grandchildren is More than Money

Cindie and I want our grandchildren to learn. We pray for them as they begin a new school year. It is exciting to see our eldest granddaughter starting college this year. Four of the six grandchildren are now teenagers. I am working to help them learn how to invest, so when they ask questions, I am delighted. When a child hits the teen years, Fidelity has an account especially designed for teens. It is the Fidelity Youth Account. We helped the four teen grandchildren open Fidelity Youth Accounts by giving each of them some cash to start their investing journey making their own decisions based on, I hope, the training I have provided. Of course, their parents are also teaching them, so they have several coaches on their side.

Recently I received another question from one of the three granddaughters. I received Mia’s permission to share her question and to talk about the advice I gave her.

Mia’s Question On August 21

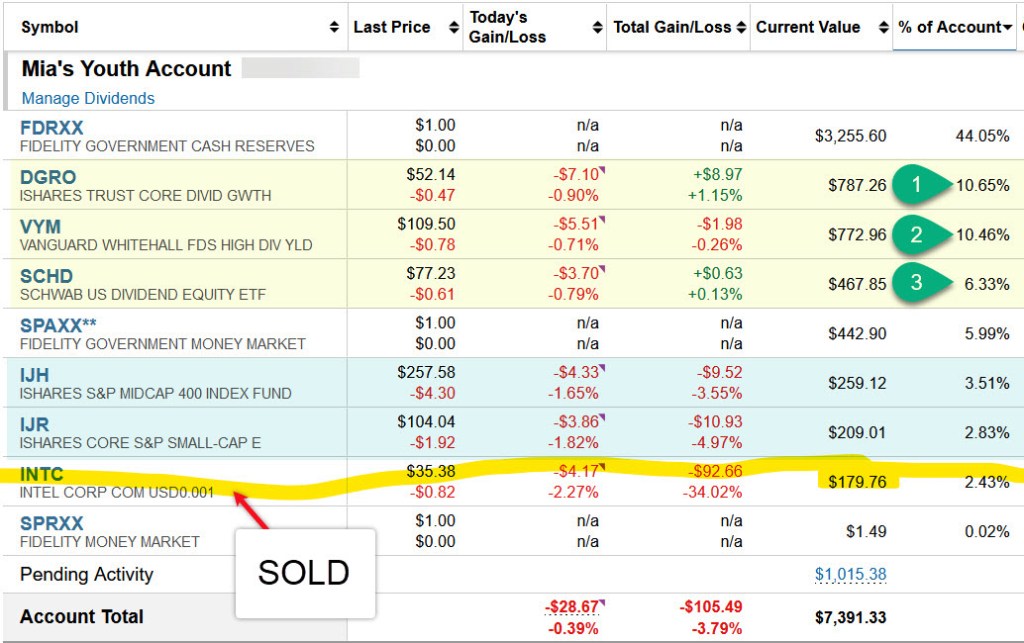

“Hi Papa, I decided to sell my shares of INTC, and I was wondering if you had any advice on ETFs I should buy with the money? Here’s a screenshot of what I already have. By the way, the FDRXX at the top is just part of my car savings. Love you!”

There are at least four things that I like about Mia’s question. 1) She realized that INTC might not have been a very good investment choice for her Fidelity Youth Account. She was wise to sell, even if she had to take a loss. 2) She sees the value in diversification using ETFs. 3) She is saving for a larger purchase so that she won’t have to take a used car loan. 4) She seeks wisdom and advice from me, making me very proud of her willingness to learn.

My Response

Dear Mia, I’m glad you asked. Here is how I look at what you shared with me.

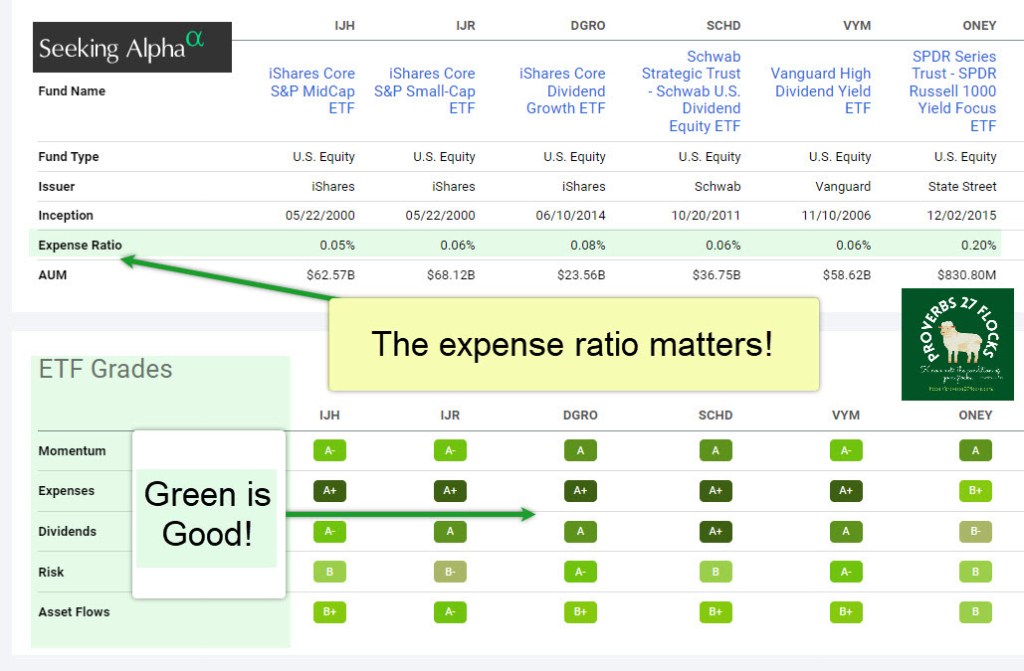

1) You already have some excellent ETFs. You already own some DGRO, VYM and SCHD that are your largest holdings. You certainly could buy more of all three.

2) I think IJH and IJR are worth buying. You have around 3% of your funds in each of them. Buying more is another good strategy.

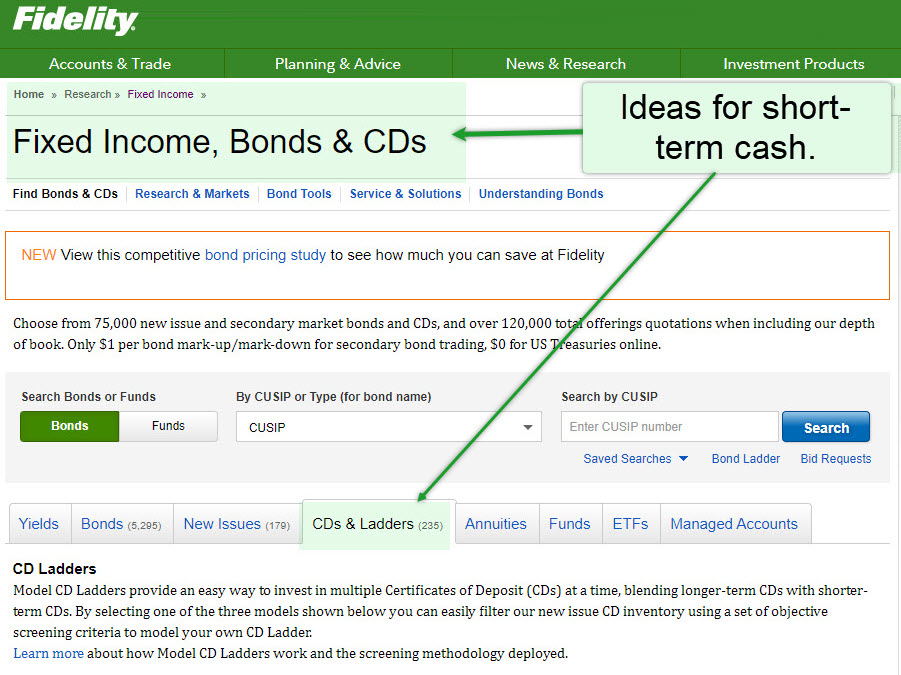

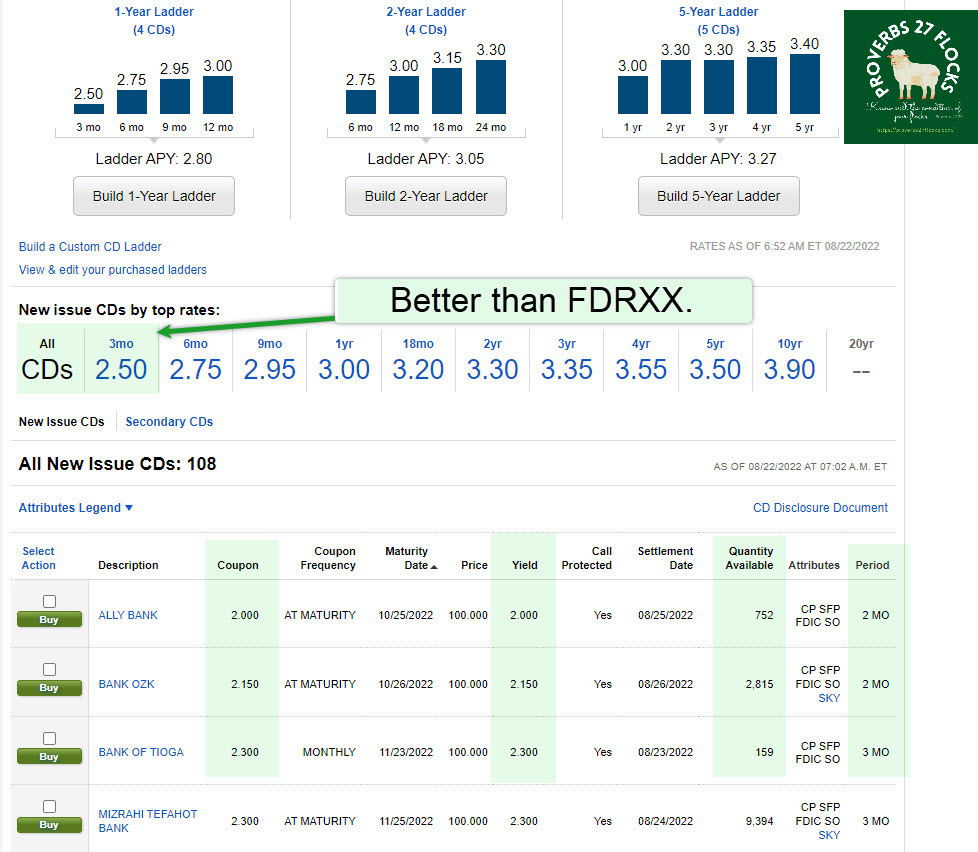

3) I would take some or all of the FDRXX and buy short-term CDs that will get you better interest without any expense fees. I can show you how to do that if you are interested. Your mom or dad could probably help you with that as well.

If you don’t plan to buy a car in 3 months, buy some 3-month CDs By the way, good job!

4) I have been starting to buy shares of an ETF called ONEY. It is also a good choice to add to your account. However, adding another ETF probably isn’t necessary given what you already have.

The following screenshots are important. Let me know if you have any questions.

Love, Papa

Learning Through Pictures

You have a good mix of investments and your top three are shown in yellow. Think about buying more IJH and/or IJR.

By the way, your question is a good one! May I use the first image below for a blog post? I would remove your account number so that no one would see that. (She said yes!)

If you don’t need the cash in the next three months, buy some CDs.

Here is how I compare the ETFs. I look at expenses, ratings, dividend growth and performance.

Mia’s Response on August 23

“Thank you for the advice! I think I’ll buy some IJR. I also did move my car funds from FDRXX to CDs, with the help of my mom. And yes, you can use that screenshot for your blog. Thanks again, love you!!”

Full Disclosure

We love all of our children, their spouses, and our grandchildren. Love is an action verb, not an emotion.

Great post, Wayne!

It’s beautiful to see your love for your family.

Have a great day, Jeremy

>

LikeLiked by 1 person

A wonderful way to share knowledge and have your grandkids get to know you as well. I think my grandkids will all say I taught them how to fish. Time in the boat. Priceless.

LikeLiked by 1 person