Some Insurance is a Necessary “Evil”

Recently a friend asked me for my thoughts about life insurance for his wife before he retires from his job. He wants to make certain that he decides what he should do based on wisdom that shows love for his wife. He then asked if the topic might be a good blog post. Yes, it is. I reviewed my past posts and did not find one that addressed his question.

The answer to his question, I believe, is primarily a subtraction calculation. That is, annual income minus annual living expenses should be a number much greater than zero. If we know what our expenses and income are, we can make an informed decision about life insurance. Of course, if the subtraction calculation shows that there is only $1,000 of income above annual expenses, then a prudent person will realize that inflation can be a long-term cancer on a small excess.

There are some forms of insurance that make sense for those who live in the USA. Some types, of course, are required by law or to satisfy a mortgage lender in order to purchase a home. Other types of insurance are sensible, and some are just plain silly. Cindie and I have automobile insurance, homeowner’s insurance, and umbrella insurance.

Although we have had life insurance in the past, we no longer see a need for that type of insurance. However, anyone who has dependents who would struggle to meet obligations or who would lack proper food and shelter if the provider died, should strongly consider some life insurance coverage. There are many different flavors of life insurance, but only one really is appropriate for most family situations. That type is term life insurance. Term life insurance assumes your financial needs will decrease and your financial resources will increase. Therefore, when the policy reaches the end of the term, it is no longer needed.

A Biblical Perspective

Because I am a Christian, I seek ultimate guidance for life decisions in the Bible. At the highest level, I am to love God and love others. Automobile liability insurance coverage is a way to try to love and protect those who might be injured and suffer loss as a result of a collision with one of our vehicles. The same is true of homeowner’s liability insurance. I am showing concern for others by having insurance. I might not have sufficient resources to cover the costs, so the umbrella policy takes it to a higher level.

When our children were little, and I was the primary source of income for the family, it was wise to have life insurance because our total investments were very small. Most of the time life insurance coverage was provided as a benefit by my employers, but I was able to and did purchase additional coverage for a small monthly premium. This was the loving thing to do to provide for the members of my household. As Paul told his young protégé, Timothy, “But if anyone does not provide for his relatives, and especially for members of his household, he has denied the faith and is worse than an unbeliever.” 1 Timothy 5:8

Life Insurance is a Contract

The insurance company creates the insurance policy and has an obligation to the owner’s beneficiaries if the policy owner dies. “A life insurance policy guarantees the insurer pays a sum of money to named beneficiaries when the insured dies in exchange for the premiums paid by the policyholder during their lifetime.” – Investopedia

Like many things in life, life insurance can be complicated and confusing. Most know that they can purchase term life insurance, but even term insurance can get complicated. There are decreasing term policies, convertible term, and renewal term polices. Other types of life insurance include whole life, universal life, indexed universal life, variable universal life, and various types of annuities. I cannot recommend any life insurance choices without knowing the needs and resources of those who are asking for guidance. However, as a general rule, the best type of life insurance is term life.

Life Insurance May Be Unnecessary

A life insurance policy to protect my wife is no longer needed. This is really just a matter of considering the income resources we have and determine if they can cover our cost-of-living expenses. At this stage in our lives, with no debt and no mortgage payments, the most costly pieces of normal life are property taxes, transportation costs and insurance, utilities, Medicare supplemental insurance, groceries, and home maintenance. Our average annual costs for these items are less than $35,000 per year.

If someone is receiving Social Security, a pension, and income from investments, they can determine what their estimated annual income will be. For example, my wife’s mother had a pension, Social Security, and investments. As her memory failed, she asked me to take over the work to pay her bills and manage her finances. I gave her monthly updates so that she would not worry about her needs. Thankfully, she did not need a life insurance policy, as her income was sufficient to cover all of her living expenses.

Cindie, of course, will not receive my Social Security if I die before she does. However, she will have her own Social Security and her expenses will probably be around $35,000 per year. So it is reasonable to assume that she will need at least $20,000 per year above her Social Security income to live, without factoring increasing costs from inflation.

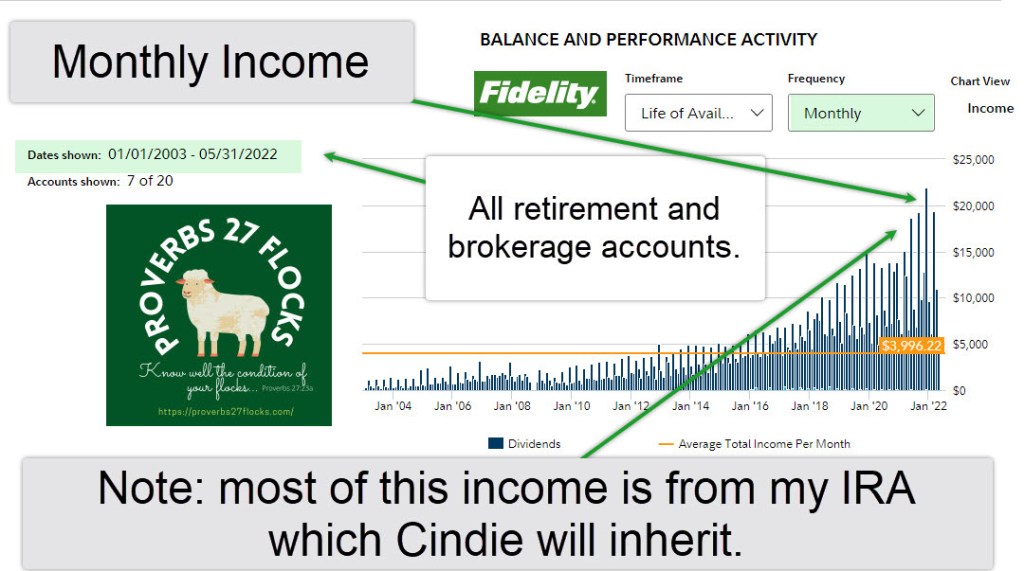

Because our investments, primarily those in my ROTH and Traditional IRA accounts pay dividends, and those dividends are growing each year, there is no need for me to purchase a life insurance policy. Cindie will have more than sufficient income to cover her needs, generous charitable giving, increasing costs due to health care, and a good buffer to keep inflation from creating a mess.

Summary: Someday you will be Verstorben.

It is true that someday I will be, as the German language says, verstorben. That is, I will be deceased. I have a will and Cindie is the beneficiary of all of the assets in my name. We also have a trust with Cindie as the primary trustee and others as secondaries to help Cindie if and when she needs help. I’ve done my love Cindie work, and I would encourage you to do your love your family as well.

Before you agree to sign an insurance policy contract, remember to think about loving your family. Loving your family means providing for them as best as you can with the resources God has given you. If you have the resources, then save yourself the cost of the insurance premium and give someone a gift instead. There are widows and orphans who certainly could use the help. That, by the way, is true religion.

James 1:27 “Religion that is pure and undefiled before God the Father is this: to visit orphans and widows in their affliction, and to keep oneself unstained from the world.”

All scripture passages are from the English Standard Version except as otherwise noted.