Looking Up or Looking Down?

In life, there are many ways to look at the current situation. Much of this has to do with a person’s worldview. There are those who count their blessings, and others who focus on what they don’t have. Some compare themselves to those they consider more fortunate, hoping to get what they have. Others look at the needs of others to see how they can help. Some people are looking up, and others are looking down. If I look down in a city, I see very little: a dirty sidewalk or street. But if I look up, I see buildings that rise because of the work of sensible builders.

When it comes to investing, looking at a single day, month, or year can be a harmful perspective. Because the market has been in a funk, I want to show you some images that help me.

Look at Twenty Years

Perhaps you have only been investing for a couple of years. During times like these it is prudent to remember that investing is a marathon, not a 50-yard dash. The following images might help you think long-term.

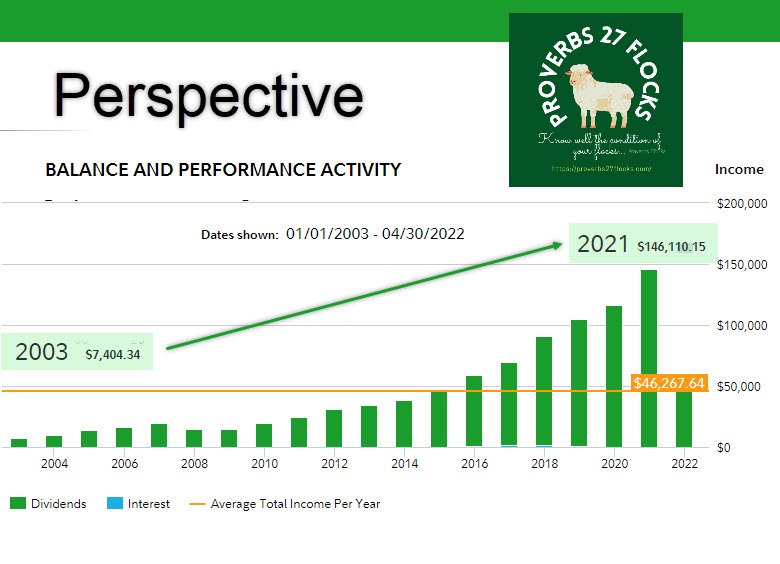

Dividend Income and Account Balances

A long-term investor builds a strategy and then has tactics that align with that strategy. My strategy is to buy quality ETFs and stocks that pay a rational dividend based on realistic earnings expectations. This certainly includes dividend growth and a rational dividend payout ratio. This strategy accomplishes two things: more income to help fight inflation, portfolio growth, and greater diversification.

Bonds versus Stocks

Many investors, if not most investors, make decisions based on fear. They don’t like risk. Sadly, the one risk they avoid (extreme volatility during bear markets) is actually a bigger long-term risk. The safe investments, including cash, CD’s, savings accounts, and bonds are not really protection if you factor the negative drains caused by inflation. Here is the allocation of assets in my ROTH IRA.

ROTH Two-Year Balance History

If you look at the April 2020 to April 2022 balances in my ROTH IRA, you will see that there are bumps in the road. But during the downward ticks, I kept my perspective.

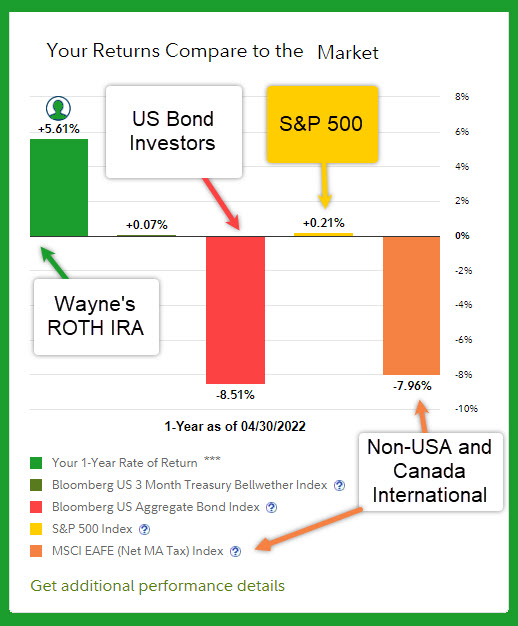

ROTH IRA One-Year Returns

The image above shows that my ROTH is still up over 5% in the last twelve months. Of course, this could change tomorrow or next month. The purpose of this image is to compare my ROTH IRA returns with US Treasury’s, the bond index, the S&P 500 (top-heavy with just a few big companies), and the MSCI EAFE index (international investment mix that excludes the USA and Canada.) How do the bond investors feel about the last twelve months? When interest rates rise, bonds are no longer as attractive because bonds do not have FDIC insurance.

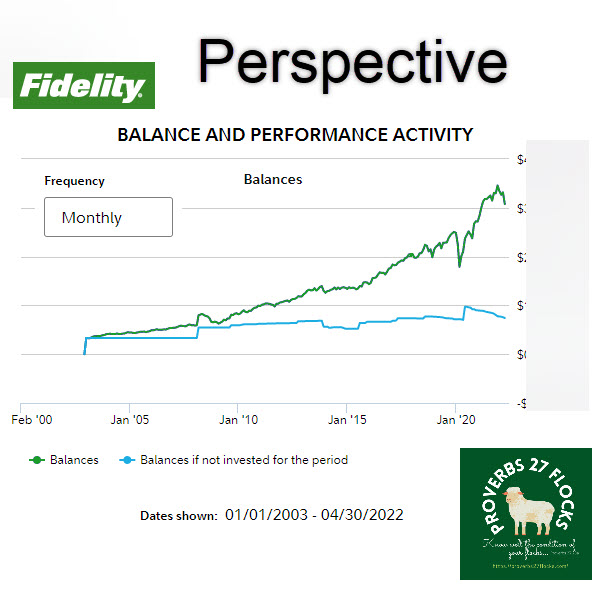

Twenty Years for All Accounts

Finally, there are two pieces for the long-term investor consider if we want to have a right perspective. The first answers the question, “does my dividend growth strategy work?” Does my strategy to choose quality investments that pay growing dividends provide more income? What happened to dividends in 2019 when Covid-19 caused fear and panic in the stock markets? They continued to climb.

Secondly, did I sacrifice portfolio growth on the altar of dividends? The following image would suggest otherwise. Bear in mind that the real returns of any market include both dividends and the growing or declining value of the investment. One thing I know for certain, even when the market is going down, I will continue to receive more dividend income than we need for living. That means, given our perspective, we can give more to those who have needs.