A Word of Caution

When I share a “top ten” list of stocks that we own, or a “top three” list of ETFs, it is important to realize that I might not recommend the same investments for you. There are a couple of reasons for this. First of all, stocks make up a very large percentage of our portfolio. As a result, I am more diversified by virtue of the stocks I have selected. In addition, a beginning investor should focus more on an approach that includes large-cap, mid-cap, and small-cap stocks using a low-cost ETF or mutual fund that provides exposure to these different areas of the market. This is important because new investors have far less wiggle room for mistakes. It is also important because new investors really should have a simple approach until they learn more about investing. Before I share our top three, you should know some basics first.

What You Should Always Know

Regardless of the funds or ETFs you buy, always be aware of at least four things about the fund: 1) The total number of stocks included in the fund. More isn’t necessarily better, but from 100-400 is probably a good range. 2) What the top ten investments are and what percentage of the total fund is the value of the top ten. If the top ten make up 40-50% of the total fund assets, be prepared for some ups-and-downs, especially if the top ten include the FAANG companies (Facebook, Apple, Amazon, Netflix, and Google). This became very obvious when Facebook dropped dramatically this week. 3) The expense ratio matters. If the expense ratio is greater than 0.30%, be thoughtful and hesitate. Perhaps there are similar ETFs that have a lower cost with comparable returns. 4) What is the dividend, and is it growing?

Retirement Portfolio Income and Growth

You don’t and shouldn’t have to sacrifice growth to get income. Sometimes you can get some good ideas by reading what others have said. One good example is this Seeking Alpha article by the “Financially Free Investor.” LINK

Real Estate Investments and ETFs

Sometimes a fund is a poor substitute for individual investments. For example, I believe it is hard to find a good ETF or mutual fund that covers the real estate sector of the economy. Rather than buy a REIT ETF, consider buying some of the better REITs. This is a helpful article by Jussi Askola. LINK

What About Our Top Three ETFs?

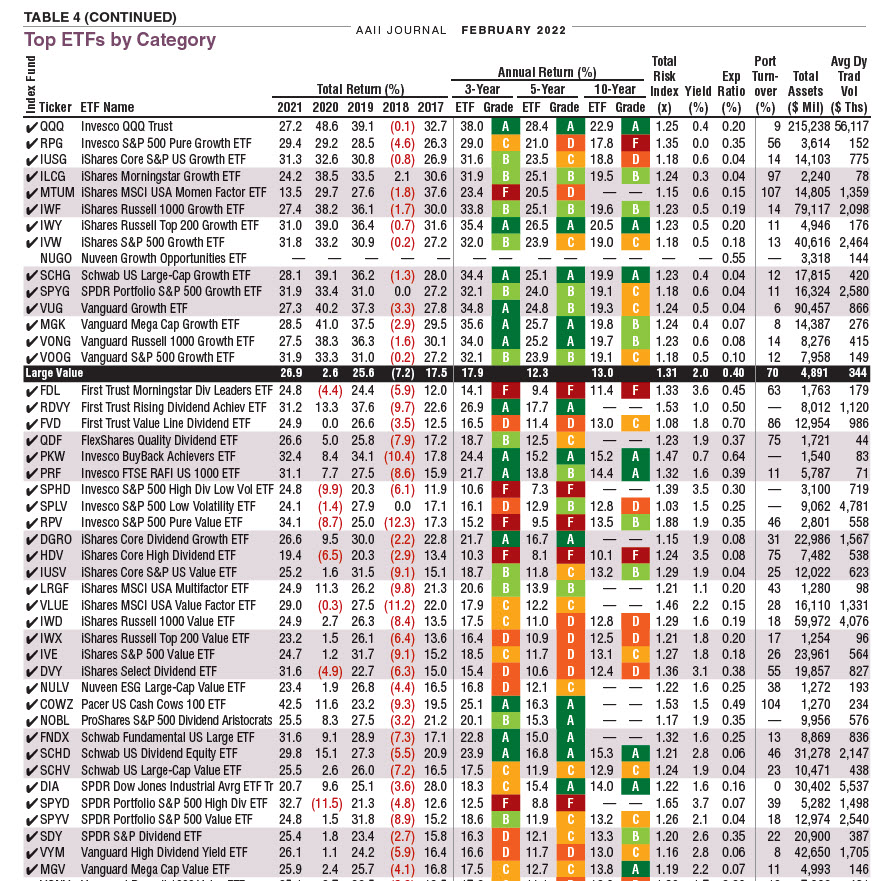

Number one of our top three is VYM (Vanguard High Dividend Yield ETF) with 415 companies, a 0.06% expense ratio, growing dividends, and a decent dividend yield. Vanguard offers more quality low-cost ETFs than any other company, in my opinion. When in doubt, it is rarely wrong to pick Vanguard. Almost 50% of the money we have invested in ETFs is in Vanguard’s VYM. In fact, VYM is also our largest investment in our entire portfolio. The 5-year dividend growth rate is an acceptable 7.01%. But the next one is better in that regard.

Number two of our top three is SCHD (Schwab U.S. Dividend Equity ETF). SCHD is about 11% of our total ETF investment universe. Like VYM, the expense ratio is 0.6%, but SCHD holds only 105 investments and the top ten make up almost 41% of the total. However, the higher risk is worth the potential for higher rewards. Furthermore, the 5-year dividend growth rate for SCHD is 12.32%. If you want a 12% raise every year, don’t work for McDonald’s. Buy SCHD instead.

Number three of the top three is DGRO (iShares Core Dividend Growth ETF). As you can see, I like Vanguard, Schwab, and iShares ETFs. DGRO is about 5% of our total ETF investment mix. The expense ration is 0.08% and the yield is 1.99%. That is better than a CD or savings account in a long-term portfolio. DGRO, like VYM, has 422 holdings, so it is more diversified. The 5-year dividend growth rate is 10.30%, so it can help you stay ahead of rampant inflation. One plus of DGRO is that the top ten investments make up 25% of the total invested dollars.

Other Dividend ETFs

Other ETFs to consider include SPYD, DVY, NOBL, VIG, and HDV. In addition, we own shares of some preferred stock and bond ETFs. Examples include PFF, PFFD, VCIT, and VCLT. Another category worthy of consideration includes QYLD and XYLD. These pay monthly dividends and focus on options trading to get some decent income for your retirement investment portfolio.

AAII Journal

Here is a more difficult way to weed through ETFs. I like AAII, but information overload is the name of the game.

Full Disclosure

Cindie and I have about $500K invested in ETFs. We own 2,325 shares of VYM as our largest holding. We have far more invested in company stocks, especially in the technology, financial, healthcare, real estate, and business development portions of the economy. We also own international investments, but I don’t think international ETFs are worth considering. If you want international exposure, buy shares in some good international companies instead. Avoid China, however, as the risks are just too great.