A New Question and My Answer

In November I posted a blog answering a question from my oldest granddaughter. It had to do with investing in an automobile manufacturer. There is some interesting history associated with the car company that makes a car she likes: the VW Beetle. The car is wonderful, but is investing in Volkswagen also wonderful? She is the owner of a wonderful Volkswagen beetle, so it isn’t surprising that she was interested in this company. About a week ago she responded with the following in response to my original blog post. A link to the original article is below.

“OH, my goodness this was so interesting. I did already know that the beetle was Hitler’s one good idea, but I had no idea how meh Volkswagen is doing. The rates are neutral, it’s not a growth investment, and compared to Ford and Toyota it’s just not the brand to choose to invest in. Bummer.

What I’m wondering is why is Volkswagen struggling so much? If it appears to be a successful company at the moment.”

What Do Investors Want to See?

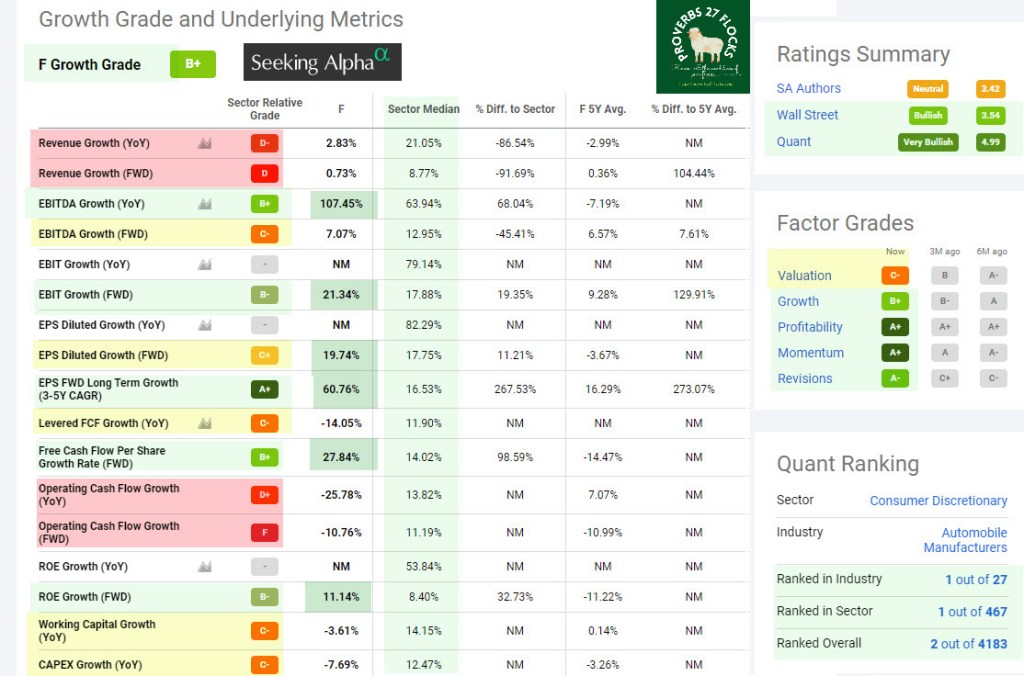

Most investors want to buy an investment today that will be worth more one, five or ten years from now. There are many ways to look at this. One is to see if the company is paying a growing dividend and that dividend is supported by growing earnings. VW pays an annual dividend and there isn’t a lot of history. Therefore, many dividend growth investors will skip VWAGY. But there is a large group of growth investors who don’t care about dividends. They buy stock in companies like Tesla, Google, and Amazon. Why do they like one company over another? Let’s explore VWAGY and compare it with Ford (F) and Tesla (TSLA).

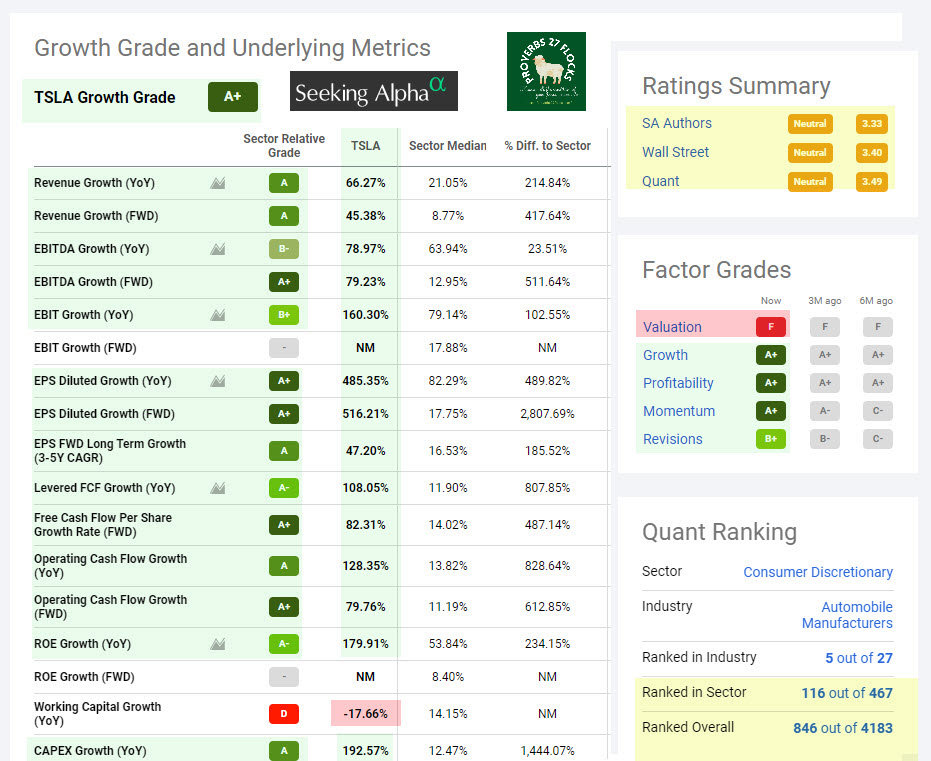

Revenue Growth

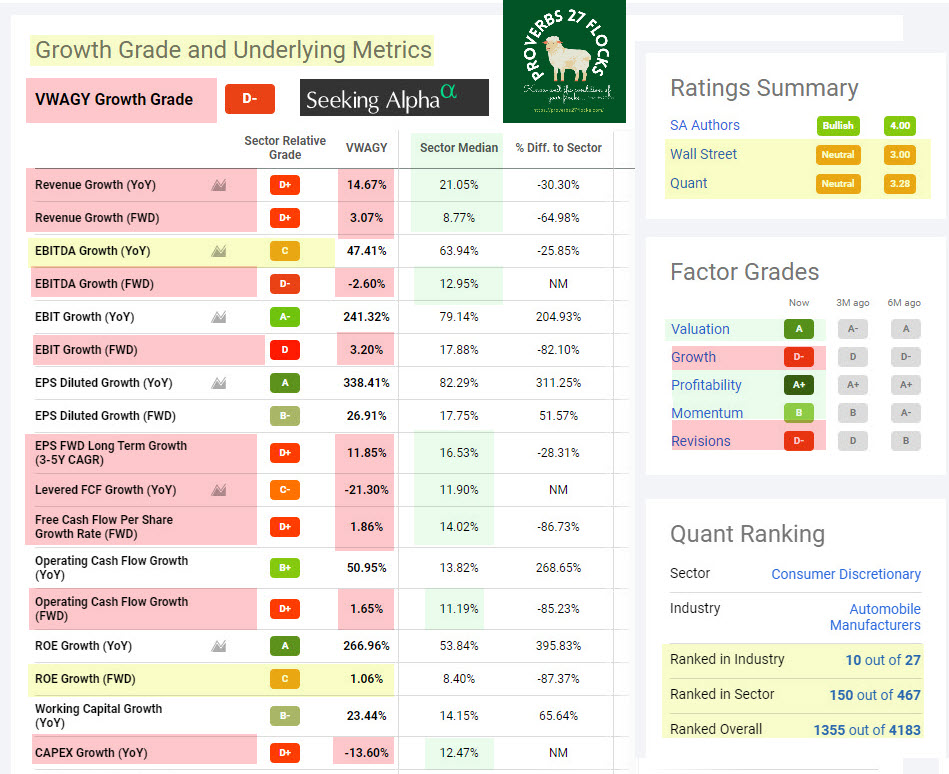

Revenue is money that is coming in from the company’s customers. Investors want to see customers spending more-and-more to buy the company’s products and services. There are at least two numbers to consider: YoY and FWD. YoY is a short way of saying “how does this year compare to last year?” That is “Year over Year.”

FWD is “forward” revenue. Forward revenue is expected future revenue based on things the company is saying. Seeking Alpha shows that VW’s YoY and FWD revenue growth both fall below the “Sector Median.” This is worse than it sounds. It is another way of saying that they are way behind the leaders in their sector (Consumer Discretionary) and are probably way behind in their industry (Automobile Manufacturers) as well. So, investors look at a tool like Seeking Alpha, and see that VW gets a grade of D+. That is a crummy grade.

EBITDA Growth

EBITDA is an abbreviation for Earnings Before Interest, Taxes, Depreciation, and Amortization. This is a fancy way that accountants look at earnings. They seem to think that it is best to remove the interest the company pays on debt, the taxes they pay, the depreciation on the company’s assets and amortization. Let’s not get bogged down with those things. Rather, because it is important, what is VW’s EBITDA picture? The FWD number is very discouraging. It is a minus 2.6%. That is awful.

Free Cash Flow is FCF

This is also a complicated piece of the puzzle. However, a simplistic way to understand why FCF is important is that “Free cash flow (FCF) represents the cash available for the company to repay creditors and pay out dividends and interest to investors.” (Investopedia) – In other words, do they have money they need to pay the bills? If customers are slow in paying for the product they bought, or their suppliers want to be paid more quickly, or both are happening, then this might spell trouble. “FCF accounts for changes in working capital. Therefore, it can provide important insights into the value of a company and the health of its fundamental trends.” (Investopedia)

VW’s Levered FCF Growth (YoY) is -21.30%. Negative is not good, and it is way below the median for this sector. The “Free Cash Flow Per Share Growth Rate (FWD) is an awful 1.86% compared to the sector median value of 14.02%.

CAPEX Growth

CAPEX is “Capital Expenditure.” That is another important piece of the puzzle. “Capital expenditures (CapEx) are funds used by a company to acquire, upgrade, and maintain physical assets such as property, plants, buildings, technology, or equipment. CapEx is often used to undertake new projects or investments by a company.” (INVESTOPEDIA) As buildings, equipment and technology get old, they usually need to be replaced. If a company is growing, they will be investing in the business. If they aren’t investing in their business, that can be a warning sign. Perhaps they cannot afford to invest, or they are uncertain what investments they should make. VW’s score on this is also very weak compared to their sector median.

What Do the Experts Think?

Seeking Alpha offers three sets of opinions: Their own authors, the opinions on Wall Street, and the proprietary Seeking Alpha QUANT rating. Both Wall Street and the QUANT ratings are “neutral.” That means “ho hum.” There is nothing exciting about VW from an investor’s perspective. The views about F and TSLA are much greener.

Violet’s Original Question

“What I’m wondering is why is Volkswagen struggling so much? If it appears to be a successful company at the moment.”

They have made some progress. However, investors perceive that Ford, Tesla, Daimler, General Motors, Toyota, and Nissan are better choices. That is probably why VW’s P/E ratio is 5.89. That is very low. TSLA’s P/E is a crazy 161.18 and Ford is at 13.18. The higher the P/E, the more the investors are voting for the growth of the investment. VW isn’t getting many votes because investors are concerned about their revenue growth, EBITDA growth, FCF growth, CAPEX growth, and their ability to compete globally against the other automobile manufacturers.

Original Blog Post: LINK

Investopedia Resources

Full Disclosure

Cindie and I own 5,530 shares of F as a long-term investment. I also buy cash covered puts for F shares and sell some covered call options. I don’t own shares of TSLA and might at some point in the future.