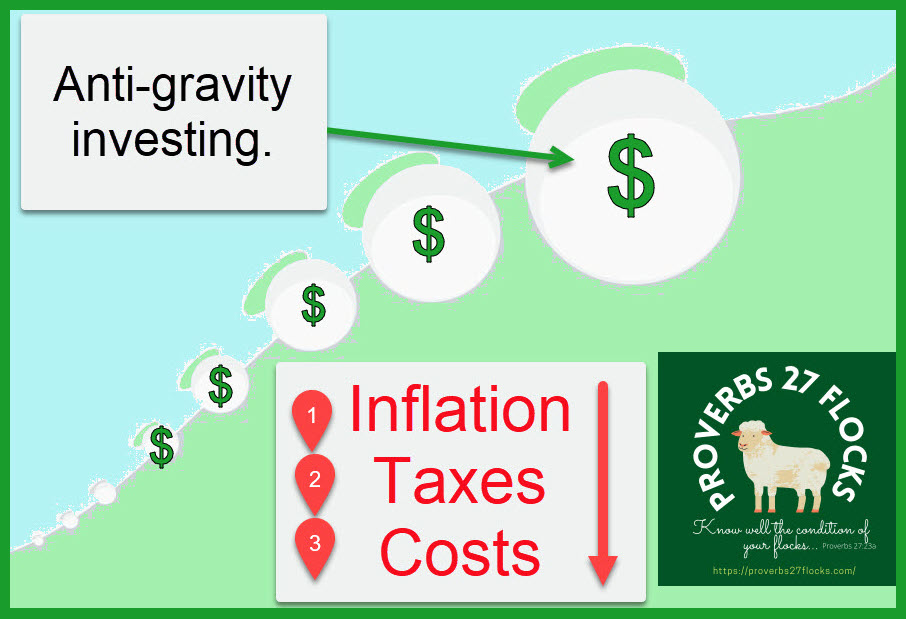

Anti-Gravity Investing

Gravity pulls things down. Some of the gravity investors face include bear markets, poor investment returns, inflation, high investment fees, high management costs, and everyone’s favorite: taxes. I build our investment portfolio to counteract government, economy, and other forms of investment gravity. The key is found in returns. What are returns? Which ones are useful for paying the bills?

Returns Matter in all of Life

The word “return” or “returns” has some interesting meanings. If you borrow a book from the library, the expectation is that you will return it. When you earn income, it is highly likely that the IRS will want you to file an income tax return. Returns are also what you should expect when you lend money. You expect to get your loan amount back with interest. Investors are also interested in positive returns. When we go away from home for a vacation, the expectation is that we will return. Even God expects returns. He says the things he has said won’t return empty. God always gets the returns he plans and purposes.

“For as the rain and the snow come down from heaven and do not return there but water the earth, making it bring forth and sprout, giving seed to the sower and bread to the eater, so shall my word be that goes out from my mouth; it shall not return to me empty, but it shall accomplish that which I purpose, and shall succeed in the thing for which I sent it.” Isaiah 55:10-11

What are Investing Returns?

Investopedia says, “A return, also known as a financial return, in its simplest terms, is the money made or lost on an investment over some period of time. A return can be expressed nominally as the change in dollar value of an investment over time. Alternatively, a return can be expressed as a percentage derived from the ratio of profit to investment. Returns can also be presented as net results (after fees, taxes, and inflation) or gross returns that do not account for anything but the price change.” Let me break that down in some simple illustrations.

The Fine Print

If you have looked at an investment, especially ETFs and mutual funds, you probably have seen wording that says, “Past Performance Is No Guarantee of Future Results.” That is a polite way of saying, “don’t count on the same returns” or “you might actually lose money.” “We might not be able to deliver comparable results, and we might also fail miserably.” As a general rule, it is best to ignore returns from the past couple of years when doing your analysis. You should focus on ten-year returns, or longer. The Securities and Exchange Commission (SEC) requires asset management firms to warn potential investors that: “the returns an asset made in the past don’t mean that future returns will be the same.”

Does Your Advisor Earn Their Keep?

A question you should evaluate at least yearly is, “does my investment advisor earn his/her keep?” In other words, if you subtract what you are paying for help, advice, trades, annual or quarterly fees and for the expense ratios on the funds they buy for you, are you at least beating the S&P 500 index? If not, you might want to think long and hard about the cost of the advice. Your returns may suffer if you don’t do at least a little bit of homework.

Whence Cometh the Returns?

Do you know if your returns are from buying and selling investments? Are your returns from dividend income on your existing investments and dividend reinvestment? Are you watching your flock to make certain the wolves (expenses) aren’t thinning the herd? Does your advisor have a strategy fueled by a goal you have provided? If you don’t know what your advisor is doing and why they are doing it, you probably haven’t asked enough questions.

You Can’t Spend Gains Until They Are Received

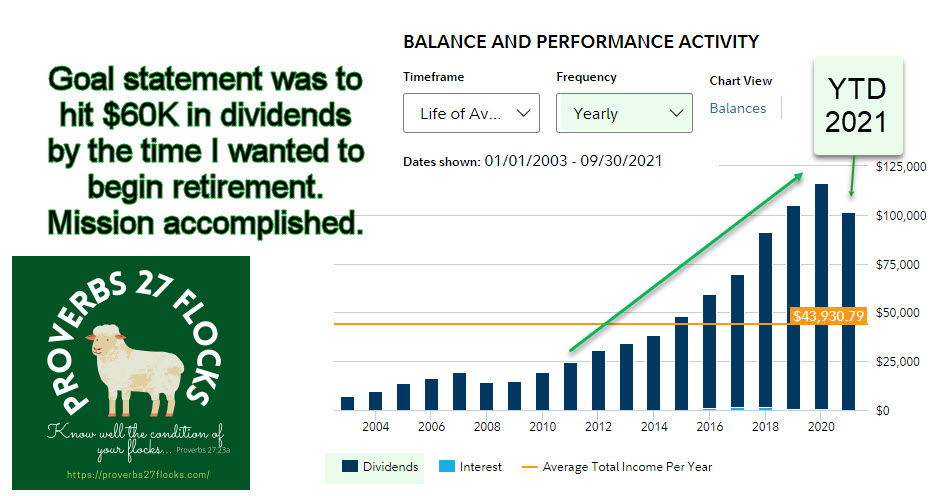

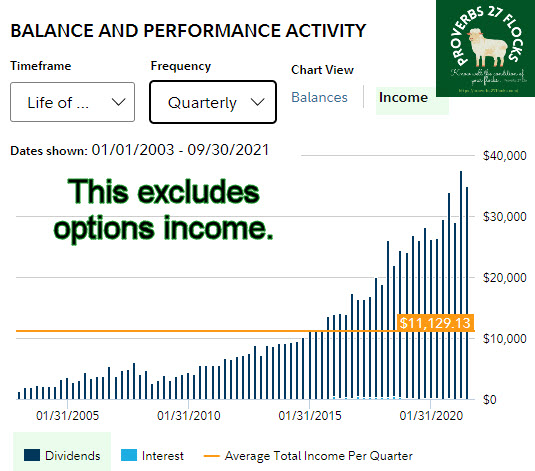

One thing that keeps some investors on the sidelines or in the slow lane, is the fear that their assets will dramatically decline in value. That is a legitimate concern. You cannot, however, spend stock prices. You have to sell the investment to have buying power. The following graphs illustrate (2003-2021) a good approach for an investor willing to have a dividend growth focus. I did not have to panic sell our investments when Covid-19 hit our investments. Having a reasonably certain income stream from dividends helped me ignore the panic and stay focused.

As you can see, our dividend income in 2019 was greater than the preceding year’s income, and the 2020 income was greater than the 2019 even though 2020 was a difficult Covid-19 year. ABBV, for example, dropped dramatically in value in 2019 and 2020. I did not sell. At the beginning of 2020 ABBV boosted their dividend. They did it again in 2021. The stock price bounces around, but the income is increasing.

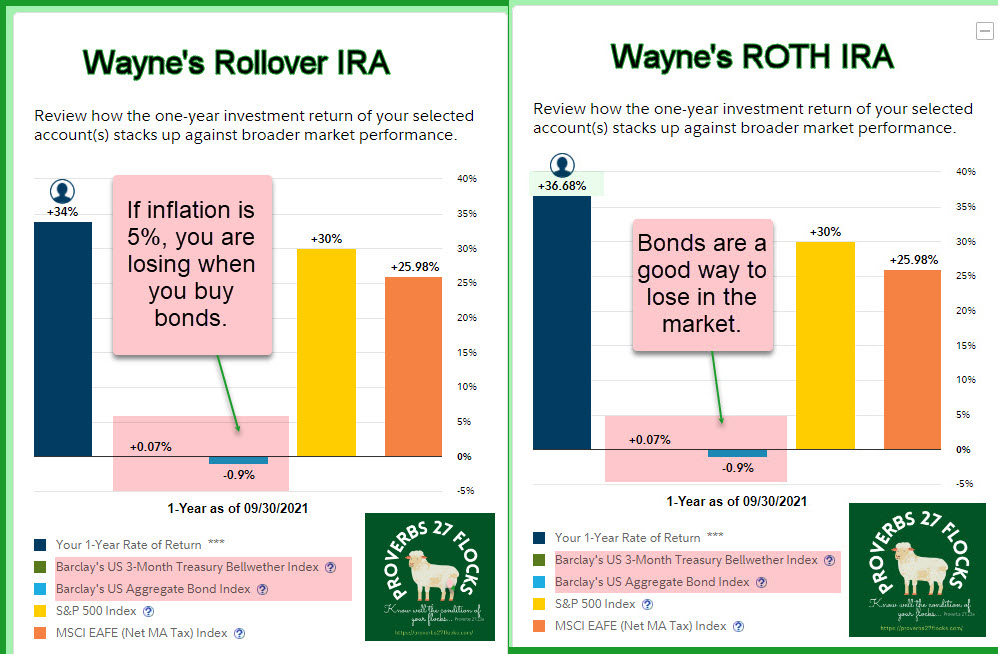

One Way to Measure Returns at Fidelity

There are several ways you can get a good idea of your returns if you have your retirement account(s) at Fidelity Investments. One quick way is a graph that shows you your 1-year returns compared to some other common indices. If you don’t at least match the S&P 500 with similar returns, then you might want to rethink your approach. This starts with a goal statement and then a strategy that can be used to reach your goal. At the very least, your advisor should provide that basic service with input from you. If you don’t provide direction and guidance, don’t expect great results.

Learn From Your Mistakes

If you don’t learn before investing, at least learn from your investing. If you don’t, you are like a dog that returns to his vomit and eats it again. “Like a dog that returns to his vomit is a fool who repeats his folly.” Proverbs 26:11

Full Disclosure

Cindie and I own 700 shares of ABBV as a long-term investment.

All scripture passages are from the English Standard Version except as otherwise noted.